The Fed Can Now Declare Victory Over Inflation

Membership required

Membership is now required to use this feature. To learn more:

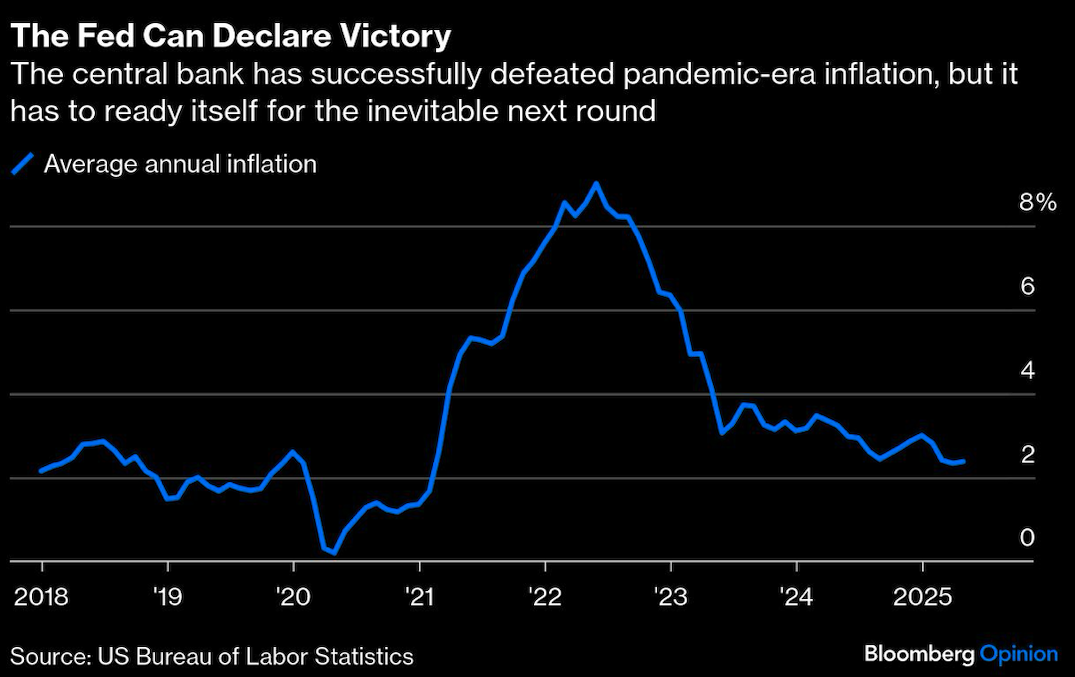

View Membership BenefitsWhen it comes to inflation, America has reached a “Mission Accomplished” moment. Rule No. 1 of inflation reports is never to read too much into one report, but there have now been several months of fairly low inflation, so it seems safe to call it: The Fed did its job. Pandemic inflation is over.

Note that I do not say, “Inflation is over.” Between tariffs and lower immigration, higher inflation is likely. But even if the next inflation report shows a big uptick, this week’s is an important marker. It bolsters the Fed’s credibility, showing that it is capable of fulfilling its mandate — and it gives the Fed more policy options if inflation returns.

Inflation has stabilized at a higher yet still tolerable level. Every inflation report this year has been fairly moderate — averaging just above a 2% annual rate.

In my book, five months makes a meaningful trend. Meanwhile, despite a federal funds rate of between 4.25% and 4.5%, the labor market is in fairly good shape and GDP is healthy. There are a few spots of weakness, but unemployment appears to be hovering at about 4% — which is probably its natural rate. From the Fed’s perspective, this is a good economy.

The question in the short run is this: Does that mean it should cut rates? The argument in favor is that the Fed’s job of containing pandemic-era inflation is (according to me) officially completed. It is time to normalize rates.

The argument against, which is stronger, is that the definition of “normal” may have changed. After all, current rates don’t appear to be having a dampening impact on the economy. Why cut rates when inflation is low and the economy is booming? It does seem that r* — the neutral rate of interest, at which rates are neither expansionary nor contractionary — is not far off from where rates are right now. At the very least, r* is quite a bit higher than it was in 2019, and higher than what the Fed forecasts it is. Cutting rates much further could risk reaccelerating inflation, which would be dangerous amid the tariff pressures already straining the economy.

So why declare victory at all? And if declaring victory, why remain cautious on rates?

Granted, it may feel premature, if not foolhardy, to declare “mission accomplished” on inflation. It’s not just the rise in tariffs and the fall in immigration; there are a lot of structural factors in the economy pointing to more inflation: more debt, an aging work force, slower productivity growth, and a world that trades less and is less reliant on the dollar. Still, declaring victory now will make it easier for the Fed to make policy in the future.

First, the days of an inflation rate below 2% may be behind us. If so, the Fed will need to internalize this truth in its communications and policies — or risk becoming too contractionary for too long in the future. When it undertakes its next framework review, it may need to increase its target rate from 2%. It can credibly do so now that inflation has been licked.

Second, the Fed needs to accept it is working with a higher r*. No one really knows what r* really is, of course, but the Fed’s view is certainly an important signal — telling markets how much they can expect the bank to increase rates if inflation comes back. Alternatively, it will signal to them how much they can expect the Fed to cut rates if the US finds itself in the dreaded stagflation scenario and the Fed must choose between boosting the labor market and reducing inflation.

The next Fed chair, whoever it may be, will have a hard job. And the most powerful tool at his or her disposal will be the Fed’s credibility. So while the Fed’s overall mission may not actually be accomplished — it is a never-ending mission — it should take this opportunity to declare victory over this round of inflation, and ready itself for the next one.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All