As early signs emerge that tariffs will drive up prices, the Federal Reserve faces a crucial question: Will tariff-induced inflation be short-lived, as the level of prices adjusts to the higher tariffs, or will it persist, as a series of feedback loops lead to further price increases?

One feedback loop that the Fed is always on guard for is longer-run inflation expectations becoming “unanchored” — that is, the rate is not expected to remain stable. If businesses and consumers expect higher inflation over the next several years, they may adjust their behavior now in setting prices, negotiating wages and making purchasing decisions. This would help make persistently higher inflation a reality, requiring the Fed to do more to reduce inflation to its target of 2% by keeping interest rates higher or even raising them.

The good news for the Fed is that, even with tariffs boosting expectations of inflation this year, surveys and market-based measures generally expect the boost to be temporary. The bad news is that there is one outlier — and it is the longest-running, most studied measure of inflation expectations.

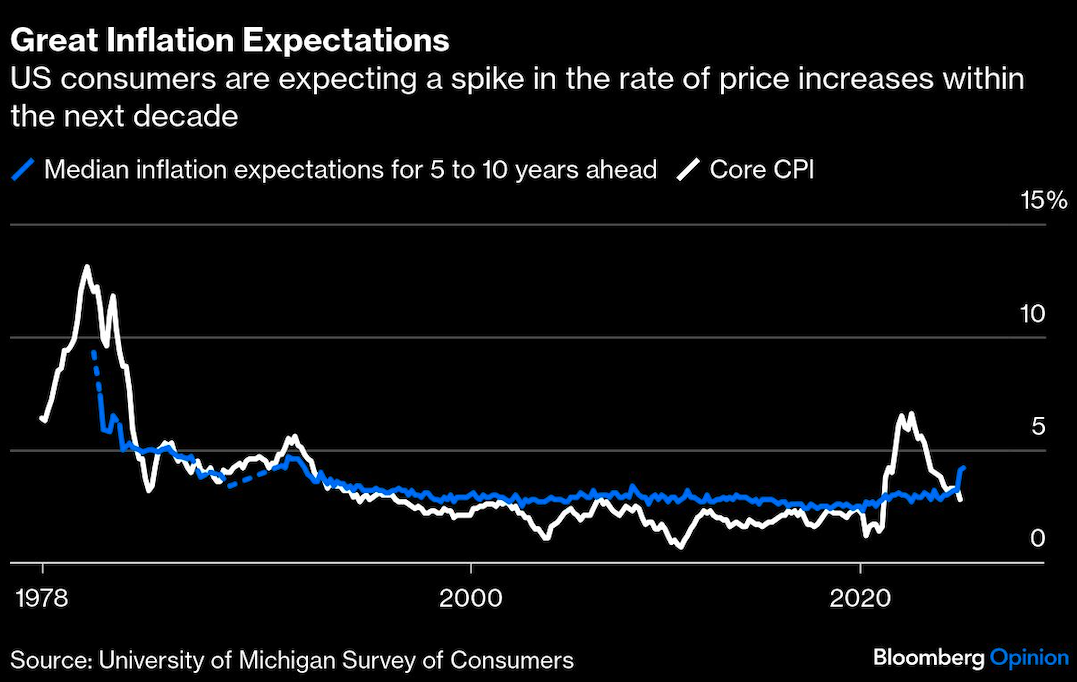

According to the University of Michigan’s Surveys of Consumers, which began in 1946 and became monthly in 1978, the median expected average change in prices in the next five to 10 years (the blue line) was 4.2% in May. That was 1.2 percentage points higher than at the end of last year, despite actual inflation slowing (the black line). The increase in longer-run expectations this year is even larger than the increase during the pandemic, when inflation surged.

After decades of low and relatively stable readings, this measure of longer-run inflation expectations has become “unanchored.” That said, there are reasons for the Fed to temper its concern, at least for now.

Most important, it’s the announcements of higher tariffs, rather than actual price increases, which appear to be driving the jump in expectations. About two-thirds of respondents to the survey spontaneously mentioned tariffs. Overall, the news that they had heard about economic conditions was dominated by news about government policy. In the past, increases in inflation expectations, such as during the pandemic, occurred when people reported hearing more news about rising prices. That’s not the case now.

Additionally, it’s not surprising that consumers struggle to translate unprecedented tariff increases of 25%, 30%, or even 145% into reasonable forecasts of price inflation, or that they may not realize that tariffs typically cause a one-time boost to inflation. Uncertainty among even professional forecasters is high, and tariff policies are constantly changing, so early expectations from consumers may shift again as they begin to experience the price changes. Asking about expectations in surveys is a useful exercise, but the current environment is pushing it past its realistic limits.

The increase in extreme responses in the survey suggests that the quality of the estimates is suffering. Twenty percent of respondents currently expect inflation to average 15% or more over the next five to 10 years. That’s even higher than in 1980, when actual CPI inflation was in double digits.

In recent years, the Michigan survey has become more susceptible to being an outlier. Last spring, to contain costs, it moved from a telephone survey to an internet survey. At that time, the share of those expecting long-run inflation of more than 15% more than doubled, to 10%. Then, when the news about tariffs drew attention early this year, the share doubled again.

It is also more susceptible to being an outlier than other surveys of inflation expectations. According to a survey by the Federal Reserve Bank of New York, the median five-year-ahead inflation rate remains unchanged this year, despite a slight increase in year-ahead inflation. It's also an internet survey, but it’s a monthly panel, and research suggests that participants learn about inflation data after they join the study and revise their expectations downward in subsequent interviews. The effect is largest in times of high uncertainty about inflation.

Of course, even outliers can provide insights into views and behavior. The Michigan survey includes some questions about buying conditions. If people expected inflation to be in double digits over the next several years, then they might be expected to buy now, before prices rise. And there has been an increase in the share of people who say it’s a good time to buy big household durable goods. But it is far less than the peak in the late 1970s and early 1980s. Consumers have extreme views on inflation now, but they are not yet changing their behavior.

There are reasons to be skeptical of the inflation expectations reported in the Michigan survey. But that doesn’t necessarily mean the Fed should be more confident about other measures.

The clearest message from the Michigan survey is not for the Fed. It’s for the White House. In recent years, the survey has picked up sharply pessimistic opinions about inflation. Now it’s picking up sharply pessimistic opinions about tariffs. So while expectations of inflation may have become unmoored, Americans’ dislike of inflation — and tariffs— is firmly anchored.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.