KKR & Co.’s recent deal for a struggling UK real estate firm was initially remarkable for landing in the midst of the American tariff turmoil. Now facing a domestic counterbid, this US-led buyout has become an emotive symbol of the London stock market’s capitulation to private equity and foreign takeovers. The odds may be stacked against the English interloper. But the situation has the feeling of an Agincourt moment for the UK market.

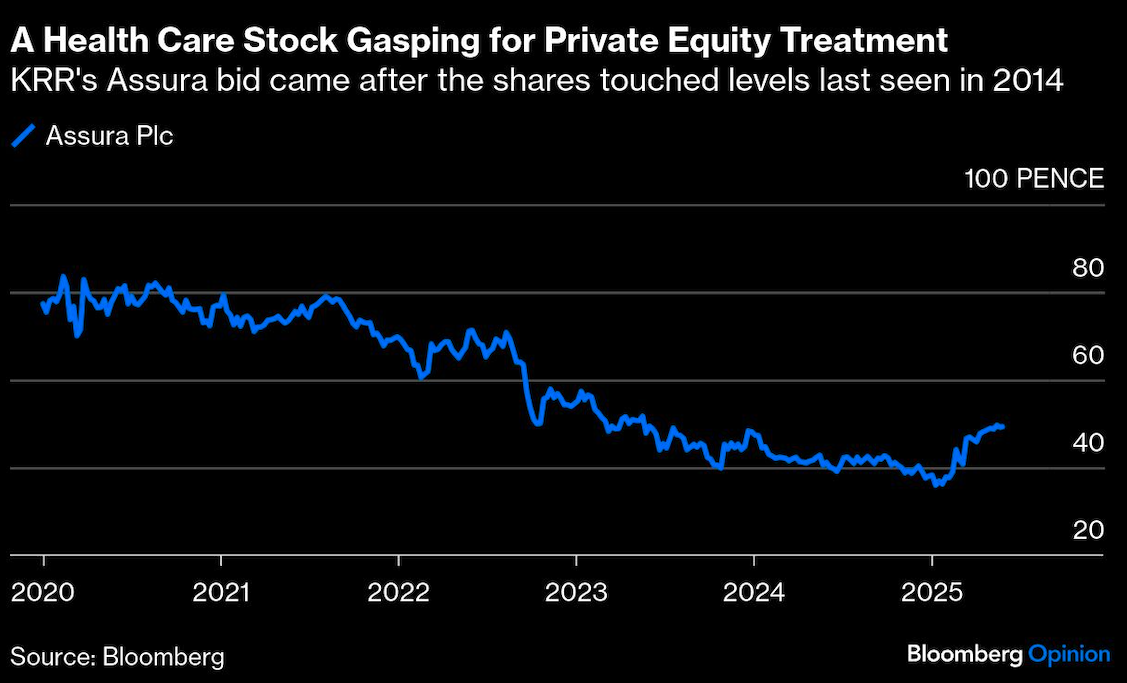

Assura Plc accepted KKR’s £1.6 billion ($2.2 billion) offer in April in a textbook UK public-to-private transaction. The property company’s long-term growth potential is plain to see, given it specializes in hospitals and surgeries. The stock had nevertheless traded at a discount to net asset value (NAV), making it vulnerable to predators. That was heightened after management overstretched to buy a hospital portfolio last August and chose to pay partly in shares, making Assura a target for short-selling hedge funds.

A KKR infrastructure fund saw off competing interest from Assura’s listed peer Primary Health Properties Plc (PHP) to reach a deal priced 32% above the share price and matching NAV. That’s so familiar with UK mid-cap takeovers: Buyers can snap up assets at roughly fair value even after paying a conventional top-up on the market value.

The US buyout firm was just doing its job in the financial ecosystem, and Assura’s board was right to acquiesce given uncertainty over the company’s ability to fund its standalone strategy. Shaking hands with KKR (and partner Stonepeak Partners LP) has also prompted PHP to make a serious counterproposal, which is now being evaluated.

Emotions are running higher than you might expect for a relatively small transaction. There’s the realistic chance of something extremely unusual happening — an agreed UK private equity deal collapsing because investors see better prospects for the target remaining a public company in London in a tie-up with a listed peer.

The backdrop here is the continuing exodus from the London market. Just this month, DoorDash Inc. agreed to acquire Deliveroo Plc, the takeaway delivery company once held up as the UK’s next big thing in tech. Last week, Honeywell International Inc. agreed to buy the bulk of chemicals firm Johnson Matthey Plc. London’s ability to nurture and grow its companies is in the dock.

There are also echoes of 2014, when the relationship between institutional investors in the UK and the private equity industry was strained in the other direction. BlackRock Inc. reportedly complained about the then-poor quality of initial public offerings, often assets that were former leveraged buyouts.

It would be great PR for the UK market if a domestic buyer offering to pay in shares saw off a cash buyout bid. The creation of a larger, more liquid real estate stock would boost the sector as a whole and help fix its lack of global visibility. While specialist investors and analysts arguing against KKR have a vested interest in preventing a cash bid, there is something at stake here for London more broadly.

But this deal needs to be decided on its merits, not patriotism. KKR is offering certainty. Its bid is 100% clear in value and lacks the regulatory hurdles of PHP’s rival proposal. At around the same price — as of Tuesday’s close — the private equity bird-in-hand would usually be unassailable.

The snag is this situation isn’t happening in a vacuum. Investors would want to reinvest the cash coming from KKR. How would they do that? Assuming they desire exposure to health-care real estate in the UK, they would use the proceeds to buy PHP stock. Accepting stock and cash in a takeover offer from PHP itself looks like a cleaner way of doing that. KKR has been quick to attack the PHP proposal for creating a more levered and financially risky business that would need to sell assets to assuage trustbusters. The potential for synergies — and lower borrowing costs in time — mitigates those risks, giving PHP a fighting chance. It’s far from clear the bidding is over here.

No one should be too sentimental about all this. Assura’s job is to get the best deal for its shareholders, mindful also of the impact of any transaction on the UK National Health Service. Its role is not to promote the London Stock Exchange. If the current competitive tension leads to a truly knockout private equity bid, and another stock market exit, that’s not such a bad outcome either.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes