Traders Eye Longer-Term Options to Hedge Post-Tariff Shock Rally

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs April’s volatility storm fades into memory, traders are left balancing calmer markets and the ever-present risk of a fresh round of headline shocks.

A consensus had developed among derivatives strategists heading into 2025: While regular option selling by income ETFs and other funds would keep volatility broadly in check, there would be more short-term shocks like Aug. 5. Following the April 2 tariff selloff that sent the Cboe Volatility Index spiking before a reversal, that view looks prescient so far.

The question for investors of how best to hedge may boil down to which Greek word they prefer at the moment: gamma or vega. Oversimplified, that’s the difference between owning short-term options that benefit from brief periods of large intraday moves, or longer-term contracts that gain value during seismic shifts in the market.

While in April short-term options were the big winners, the big intraday and close-to-close gyrations may not repeat if stocks slide back to last month’s lows. That has strategists pointing again to longer-dated contracts — a popular trade heading into the April 2 tariff shock — expecting that the current rally that has erased all of the early April losses will run out of steam.

“While we can’t entirely rule out a sudden equity market shock, we expect a more gradual repricing driven by weaker forward guidance — in essence, a low-volatility bear market,” said Antoine Bracq, head of advisory at Lighthouse Canton.

Future tariff announcements may have a diminishing impact on volatility, especially as Trump has shown the propensity to re-align himself with financial markets within days, particularly if the bond market is sending signals. So market participants are looking for ways to play equity downside while staying short or neutral volatility.

With the market one trade headline away from a sharp reversal, hedges need to be actively managed to cash in a winning position quickly before conditions change. That adds a further complication.

“Theoretically, the most effective hedge would be to short futures, but the challenge lies in knowing precisely when to lift it,” said Bracq. “Because of this, we see a more practical approach in exploiting the current levels of implied volatility (with the VIX now back around 22) by buying a December 2025 100%-80% put spread.”

Amid the market uncertainty, there are a number of alternatives in the listed and over-the-counter arenas. One popular OTC short-stock/short-volatility play is through so-called volatility knock-out — or VKO — puts. The buyer owns a put on the S&P 500 Index, for instance, until realized volatility rises above a preset level. At that time the option knocks out and expires worthless.

Such trades are more akin to a speculative bet than a true hedge given that investors may not actually be protected when they really need it. The attraction: They are 40% to 50% cheaper than vanilla options, depending on where the volatility knock-out barrier is set.

Hedge funds were reported to be active in VKOs during the recent market drawdown to capitalize on better entry points — betting on both lower equities and lower volatility. The entry point is critical: A position put on April 1 was likely to knock out quickly, while a six-month trade entered Jan. 1 is probably still live, depending on the barrier level.

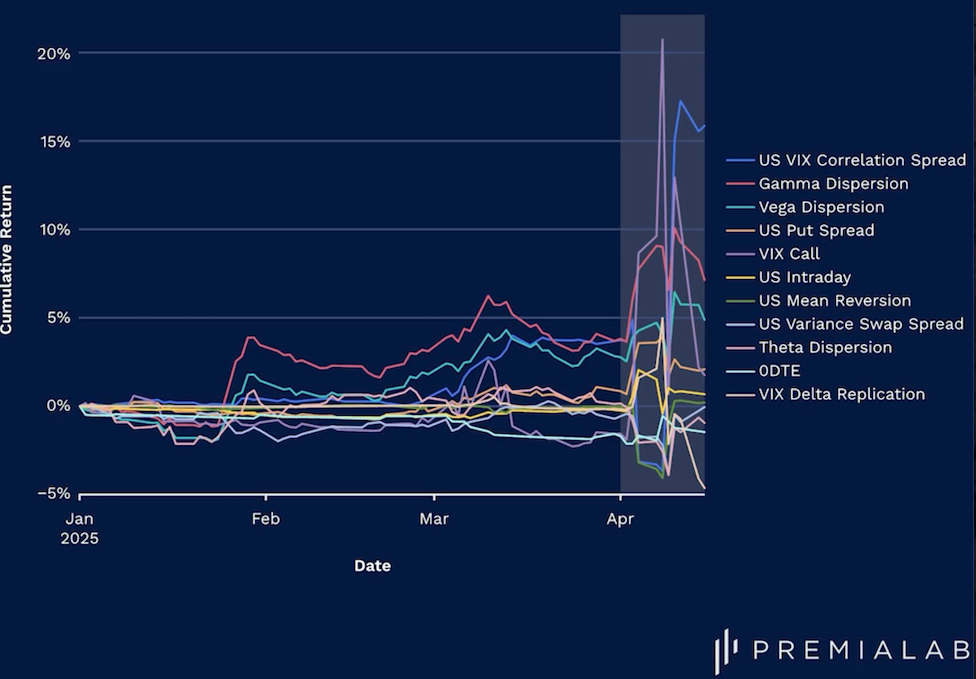

Investors may also look to hedge via the growing number of Quantitative Investment Strategy products on offer, in which case a blended approach of several strategies is likely to be appropriate given how performance diverged over the April turmoil.

In European markets, institutional desks have been seen buying far out-of-the-money tail-risk protection. The low-cost, low probability binary-style put spreads — June 3,975/3,925 put spreads on the Euro Stoxx 50 Index, for example — can pay out more than 75 times the premium paid if markets collapse.

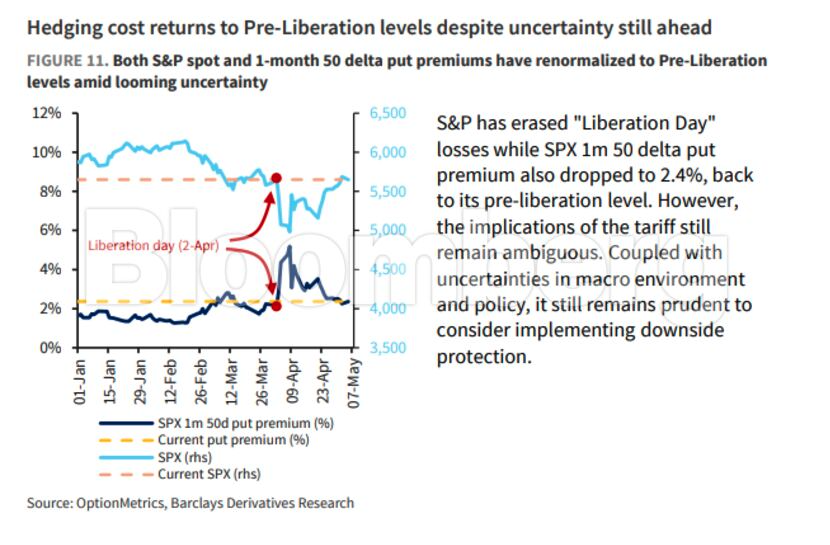

The good news for hedgers, whether looking at short- or longer-term contracts, is that costs have fallen back to levels last seen in late March, according to Barclays Plc strategists.

BNP Paribas SA strategists’ base case is for earnings downgrades and valuations’ compression to push equities down to retest 2025 lows. But while headline shock defined the previous downturn, they expect a renewed decline to be a grind lower. That will keep fixed-strike volatility from jumping like it did in the early April selloff.

“Gamma massively performed following ‘Liberation day’ amid the the huge intraday swings in price, but the Trump ‘put’ may limit the extent of the payoff if there is another leg lower,” said Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All