A time-honored signal heeded by Wall Street’s credit industry — the weekly flow of money — is breaking down.

For years, money pouring in and out of bond and loan funds investing in Corporate America moved in lockstep. One week’s flows were a decent predictor for the following week, and so on. Not so, these days. The likely reason: Easy-to-trade exchange traded funds are booming and sucking in ever-more erratic capital flows, muddling up buy and sell signals for liquidity-obsessed debt investors.

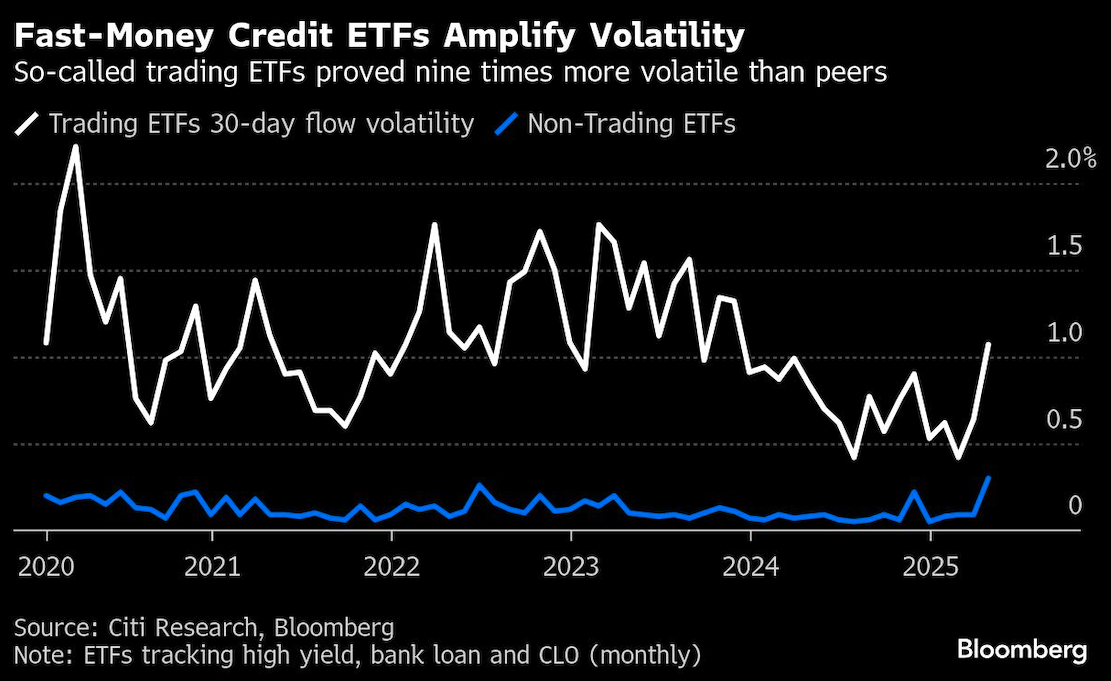

Go-to funds from the likes of BlackRock Inc. and State Street Corp. are increasingly popular with hedge funds and institutions making tactical allocations. Since 2019, money into so-called trading ETFs — heavily traded funds favored by fast-moving institutional investors — has proved nine times more volatile than slower-moving ETFs favored by buy-and-hold investors, according to research from Citigroup Inc. Take what happened in April, for example: HYG, the biggest junk bond ETF, saw choppy flows that fluctuated in and out compared to non-trading ETFs like HYLB and ANGL.

While the ETF boom comes with benefits for investors of all stripes, it’s making life harder for those traders dissecting real-time allocations into investment strategies to gauge sentiment. Though trading ETFs hold 40% of credit fund assets, they drive roughly 80% of exchange volume, according to Citi.

“ETF-driven flows can make short-term moves in credit more volatile,” said Grant Nachman, founder of Shorecliff Asset Management. “That said, the ETFs likely constitute a long-term positive for the market, as they broaden the buyer base, improve liquidity, and help institutionalize the asset class.”

Loan ETFs show the shift. Back in 2017, they made up just 10% of reported loan-fund flows across all kinds of funds, including mutual funds and ETFs. Now, the cohort comprises nearly 50%, thanks to the growth of products from big-name issuers, with tickers like SRLN, BKLN and USHY. So-called portfolio trading and electronification have made it easier to move size quickly, accelerating the “equitization” of fixed income.

“It’s all happening at the same time,” Drew Pettit, director of ETF analysis and strategy at Citi Research, said in an interview. “I’m not sure if the boom in ETFs is shaping the market or if it’s just a symptom of how the plumbing’s changing.”

At least six credit ETFs debuted so far in 2025, following 26 last year, data compiled by Bloomberg Intelligence’s Athanasios Psarofagis show. The group has amassed more than $363 billion in assets with an average trading volume of around $160 billion per month.

ETFs have grown in preference as efficient vehicles for price discovery even in times of stress. This includes the pandemic and the 2023 collapse of regional banks. That’s a boon for a once-fragmented asset class as investors migrate to the cheap trading vehicles. The growth of trading ETFs, according to Pettit, is also a clear indication of the evolution in the underlying liquidity system of the asset class.

Citi strategists use a 10-factor checklist — size, turnover, options volume, short interest and more — to classify what they call trading ETFs, those mostly used by institutions. The top funds attracted 20% of net new money last year, despite driving the majority of activity. That disconnect speaks to how much influence is concentrated in a small set of tickers. And critically, Citi found there’s no statistical link between one week’s flow and the next, especially in high-yield. For managers who relied on those signals, it’s been a challenge.

“They create more noise than signal,” John McClain, portfolio manager at Brandywine Global Investment Management, said of large credit ETFs. “The volatility certainly leads to micro dislocations for a manager like us to take advantage of. But the market structure is now materially different.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Isabelle Lee