The Treasury Department said it’s now looking at “enhancements” to its buybacks of older US government debt securities, just weeks after Scott Bessent hinted at the potential to beef up the program in the event of any major market turmoil.

“Treasury will evaluate a broad range of possible enhancements such as: changes to maximum purchase amounts, buyback operation scheduling and frequency” and other details, it said in a statement Wednesday.

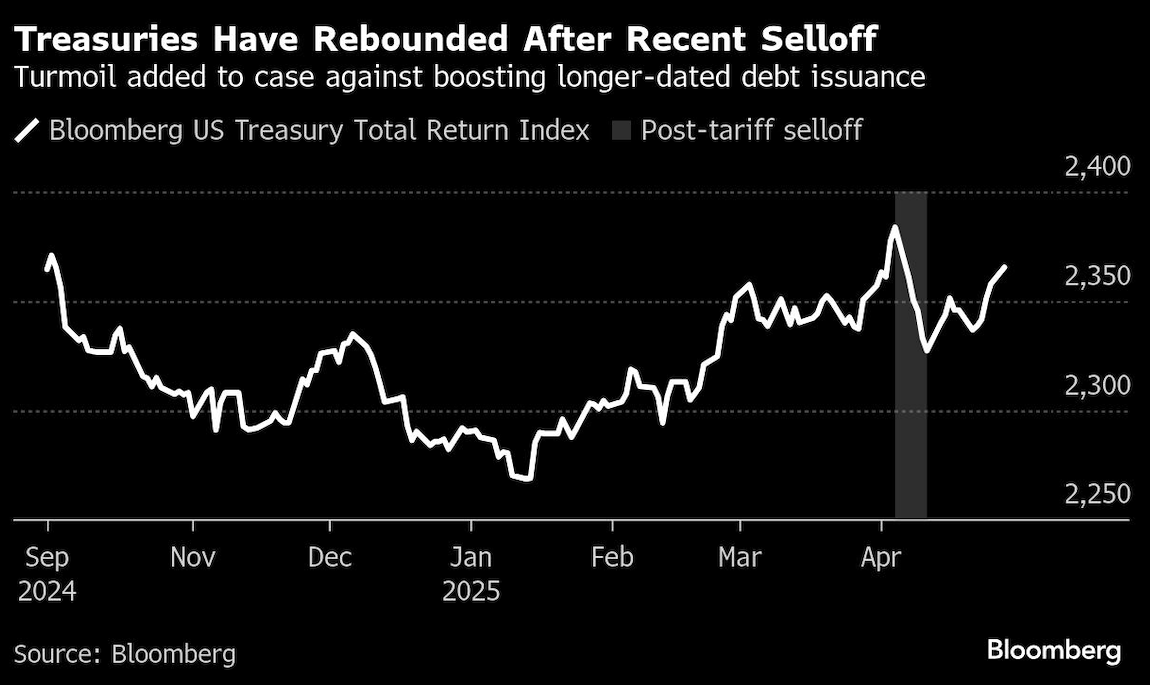

After an unusual tandem selloff of Treasuries with stocks and the dollar that saw yields climb the most since 2001 earlier this month, Treasury Secretary Bessent said in a Bloomberg interview that his department had a “big toolkit” to deal with emergencies. He said, “We could up the buybacks if we wanted.”

That “extreme volatility” in Treasuries was caused by factors including concern over President Donald Trump’s tariff announcements, concerns about any threat to Federal Reserve independence, uncertainty about the economic outlook and a bout of de-leveraging by investors, according to the Treasury Borrowing Advisory Committee — an outside panel of dealers, investors and other bond market participants.

“Treasury’s buyback program remained well received by the market through this period, in keeping with its objectives to support liquidity and cash management,” the TBAC said in a report to Bessent, also released Wednesday. Even so, the panel “felt it important that broader metrics” such as the overall weighted average maturity of Treasuries be managed by its normal issuance decisions.

Steady Issuance

As for immediate issuance plans, the department — as dealers had widely forecast — said it will sell $125 billion of securities at next week’s so-called quarterly refunding auctions, which span 3-, 10- and 30-year maturities.

Reiterating guidance that’s been in place since January last year, the department said, “Based on current projected borrowing needs, Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.” FRN refers to floating-rate notes.

The refunding documents were released at the same time as US gross domestic product data. Treasury yields jumped after those figures showed an jump in a gauge of prices last quarter, though the move eased as Wednesday’s session wore on.

While Bessent once criticized his predecessor, Janet Yellen, for holding down sales of longer-dated Treasuries to suppress borrowing costs and juice the pre-election economy, he has continued to keep her issuance plan. The recent market turmoil only added to the argument against boosting issuance of notes and bonds.

Many dealers estimate the Treasury won’t need to resume boosting the size of note and bond auctions again until late this year or early 2026. Outsize fiscal deficits, running near $2 trillion a year, mean most analysts see an increase as inevitable at some point.

As for next week’s refunding auctions, the $125 billion will be made up of the following:

- $58 billion of 3-year notes on May 5

- $42 billion of 10-year notes on May 6

- $25 billion of 30-year bonds on May 8

The refunding will raise new cash of about $30.8 billion.

The Treasury also said it was continuing to nudge sales of some Treasury Inflation Protected Securities, or TIPS, higher in order to keep their share of the overall Treasury market stable, announcing the following adjustments:

- To increase the June 5-year TIPS reopening by $1 billion

- Boost the July 10-year TIPS new issue by $1 billion

Along with uncertainty about future revenue projections given shifts in tariff policy and the economic outlook, US debt managers are currently operating under the challenge of the statutory debt ceiling. That leaves them unable to boost the overall net supply of Treasuries, forcing them to deploy cash reserves and so-called special accounting measures to make good on payment obligations.

The department said it expects to release an update on “how long its cash and extraordinary measures may last” during the first half of May.

Until the debt limit is increased or suspended, there will be “greater- than-normal variability” in bill sales, the department also advised.

Some dealers had been on the lookout for any hints that the Bessent Treasury may be leaning toward boosting the share of bills over time — setting aside past criticism of Yellen. The department has questioned dealers on the potential bill demand from stablecoins, in one possible indication officials are contemplating a structural change in the market.

Minutes of a meeting of the Treasury Borrowing Advisory Committee, a panel of dealers, investors and other bond market participants, said that “dealers agreed that the digital asset space was important to monitor on an ongoing basis as a potential source of Treasury demand.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Daniel Flatley, Christopher Anstey