President Donald Trump’s new reciprocal tariff policy is straightforwardly bad for the US economy and markets. The only conceivable reason that the S&P 500 Index was down just 4% on Thursday is that investors still don’t believe it will stick. Unfortunately, there’s no quick way out of this quagmire. No easy off-ramps via negotiation. No stock market “put” from the Federal Reserve. And no federal tax cuts or other stimulus that can sufficiently offset the hit.

Let’s take those issues one at a time.

In the very earliest days of the second Trump administration, investors saw The Art of the Deal version of Trump use short-lived tariffs for pure coercion. Perhaps the clearest example was when Trump threatened Colombia with 25% tariffs over its refusal to accept deportees transported under degrading conditions. Within days, Colombia accepted the deportees and the tariffs went away. Anyone hoping for that outcome with Trump’s “reciprocal tariff” policy is, sadly, delusional.

Trump, who has been talking up the merits of tariffs in trade policy since the 1980s, won the 2024 election on a Big Tariff platform. The nature of his latest proposals basically forecloses on the possibility of a deal that all parties can agree to quickly. His broadsides hit just about every country around the world, and the tariff rates were based on the false premise that bilateral trade deficits are inherently bad (they’re not). They punish lots of legitimate bad actors in trade (such as China), and many others (friends in Latin America) that have mostly just tried to play the role of good neighbors.

It would be one thing if the White House had set the new tariffs to match other countries’ tariffs on us, but that’s not what it did. The actual tariff rates ended up being much higher, in many cases, than pure tariff reciprocity would imply. As Bloomberg News’ Josh Wingrove has written, the formula essentially divides a country’s trade surplus with the US by our total imports from that country, based on data from the US Census Bureau for 2024.

In other words, some countries will get hit hard simply because they sell a lot of goods that Americans desire, irrespective of their actual policies. The Trump administration has argued that countries use policies such as food inspection standards and value-added taxes as shadow barriers to trade (which is highly controversial to begin with). But the actual tariff policy announced didn’t account for those things, so there’s no reasonable basis for negotiations. (Despite the unfairness, the economic impacts are so damaging for some economies that they will probably come to the table anyway. But the odds of a swift outcome that satisfies both sides are close to zero.)

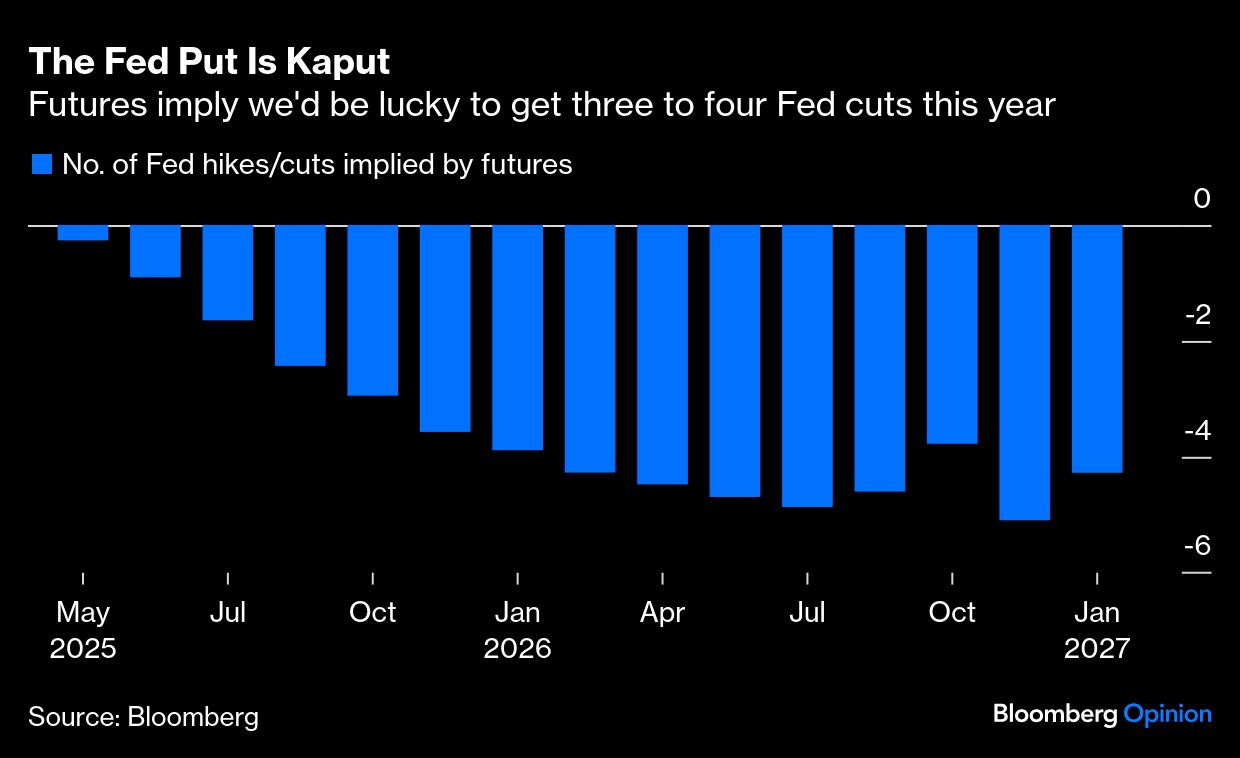

Next, some market participants might cling to hopes of major monetary policy support, but that’s a fantasy as well. At the time of writing, futures trading implied about three Fed cuts this year, with better than even odds of a fourth. On the one hand, 0.75 to one percentage point of cuts over many months would hardly be the sort of stimulative bazooka that markets have come to expect in times of extreme stress — the so-called “Fed put” made famous during the chairmanship of Alan Greenspan.