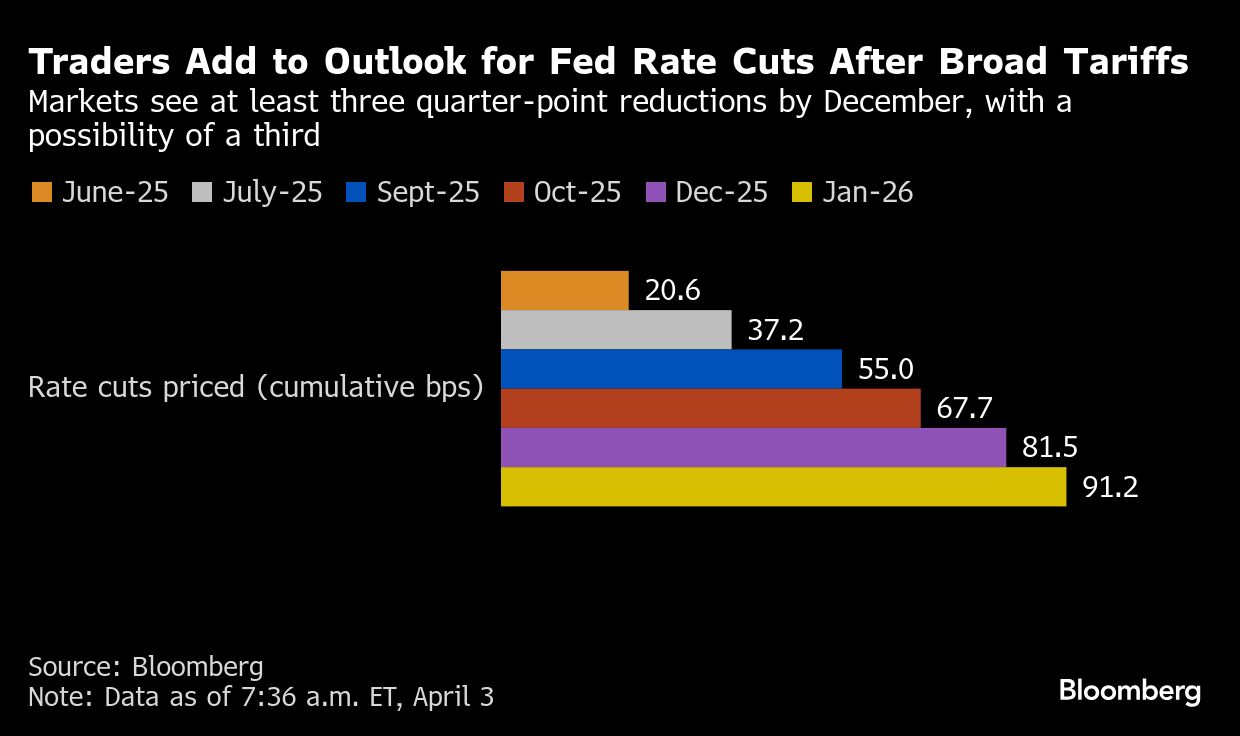

Bond traders ramped up bets on interest-rate cuts from the Federal Reserve amid concern that Donald Trump’s trade war will backfire on the US economy, sending the yield on benchmark Treasuries toward the closely-watched 4% level.

Money markets are now pricing a 50% chance of the Fed delivering four quarter-point rate reductions this year, a scenario that wasn’t even contemplated on Wednesday. Ten-year yields declined as much as 11 basis points on Thursday to 4.01%, the lowest level since October, while five-year rates slid as much as 15 basis points.

Concern that the steepest increase in American tariffs in a century will hammer economic growth is driving a fierce rally in global bond markets, with yields on European and UK bonds also plunging. Similarly, traders ramped up wagers on monetary easing from the European Central Bank and the Bank of England, boosting the chances that both deliver three more cuts this year.

“The bond market is a big winner,” said Kathleen Brooks, research director at XTB. “Central banks are likely to step up to ease some of the pain from the US’ new global trade policy.”

Trump’s tariff plan on Wednesday came much harder than expected, as he announced a minimum 10% levy on all exporters to the US and slapped additional duties on nations with big trade imbalances. The move escalated global trade tensions and sent investors rushing for safe havens.

The response in bond markets was sharp. European yields tanked across the board, with Germany’s policy-sensitive two-year rate down as much as 12 basis points to 1.92%, while 10-year peers fell as much as 10 basis points to 2.63%. Swaps are now pricing 67 basis points of further easing from the ECB this year, compared to 60 basis points on Wednesday.

In the UK, traders added about 10 basis points of rate-cut expectations to the year, and now see a chance of more than 50% that the BOE will lower borrowing costs three more times. Gilt yields fell across the curve, sending the two-year rate to the lowest since October.

Some analysts anticipate Trump’s tariffs will lead European bonds to outperform their US peers. While growth fears dominated on Thursday, concerns about a resurgence of inflation are also lurking if the cost of tariffs gets passed on to the consumer, with that seen as more of a concern for the US than for the European Union.

“In the US, inflationary pressures will be immediate, with the hit to growth only later,” said Nomura economist Andrzej Szczepaniak. Europe, meanwhile, is facing a “double whammy” of a “negative hit to GDP growth and deflation from goods dumping,” he added, referring to the possibility that China redirects goods to Europe to avoid US tariffs.

US inflation risks arising from tariffs have led Morgan Stanley’s economists to push back their call for the next Fed rate cut from June to early 2026. They see a terminal rate of 2.50% to 2.75%.

More Gains

Still, many are wagering on more gains for US bonds ahead. Strategists at Citigroup Inc. upgraded Treasuries to overweight following the tariff announcement, saying Trump was more aggressive than markets expected and the tariffs pose a clear risk to US growth.

“It looks like we’re cruising to recession now unless things change,” said Bob Michele, global head of fixed income at JPMorgan Asset Management on Bloomberg TV, contending that the inflation momentum is very different from post pandemic and is unlikely to be sustained. If these policies stick “the Fed can bring down rates a lot,” possibly to as low as 2.5% from 4.5% currently.

Strategists at Goldman Sachs, Barclays, Royal Bank of Canada and Societe Generale have already cut their year-end forecasts for 10-year Treasury yields. In large parts, they pointed to an uncertain economic backdrop, though questions also remain about Treasury Secretary Scott Bessent’s plans for issuance.

“The disinflationary, recessionary impact will ultimately overwhelm the inflationary impact of tariffs. That’s a one-off price shock,” said Tom Roderick, portfolio manager at hedge fund Trium Capital. He’s receiving 2026 US rates, cautioning that “material flows” into duration are unlikely to pick up until investors actually see a recession.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by