It’s Not Just America Trying to Halt Clean Energy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIt’s not just America and Europe that fear the competitive threat from Chinese clean technology. China itself is scared.

Wind and solar developers in the country installed more than 60% of the world’s renewables last year, upsetting a market where coal has traditionally dominated.

The response has been roughly the same as in other countries contending with imported Chinese solar panels and electric vehicles: A push for the government to raise barriers to the disruptive upstarts, and coddle the bloated incumbents.

The measures have been remarkably effective. Despite renewable generation that’s far exceeded the most optimistic forecasts, fossil power in China hasn’t been squeezed out. Instead, coal has largely maintained its position.

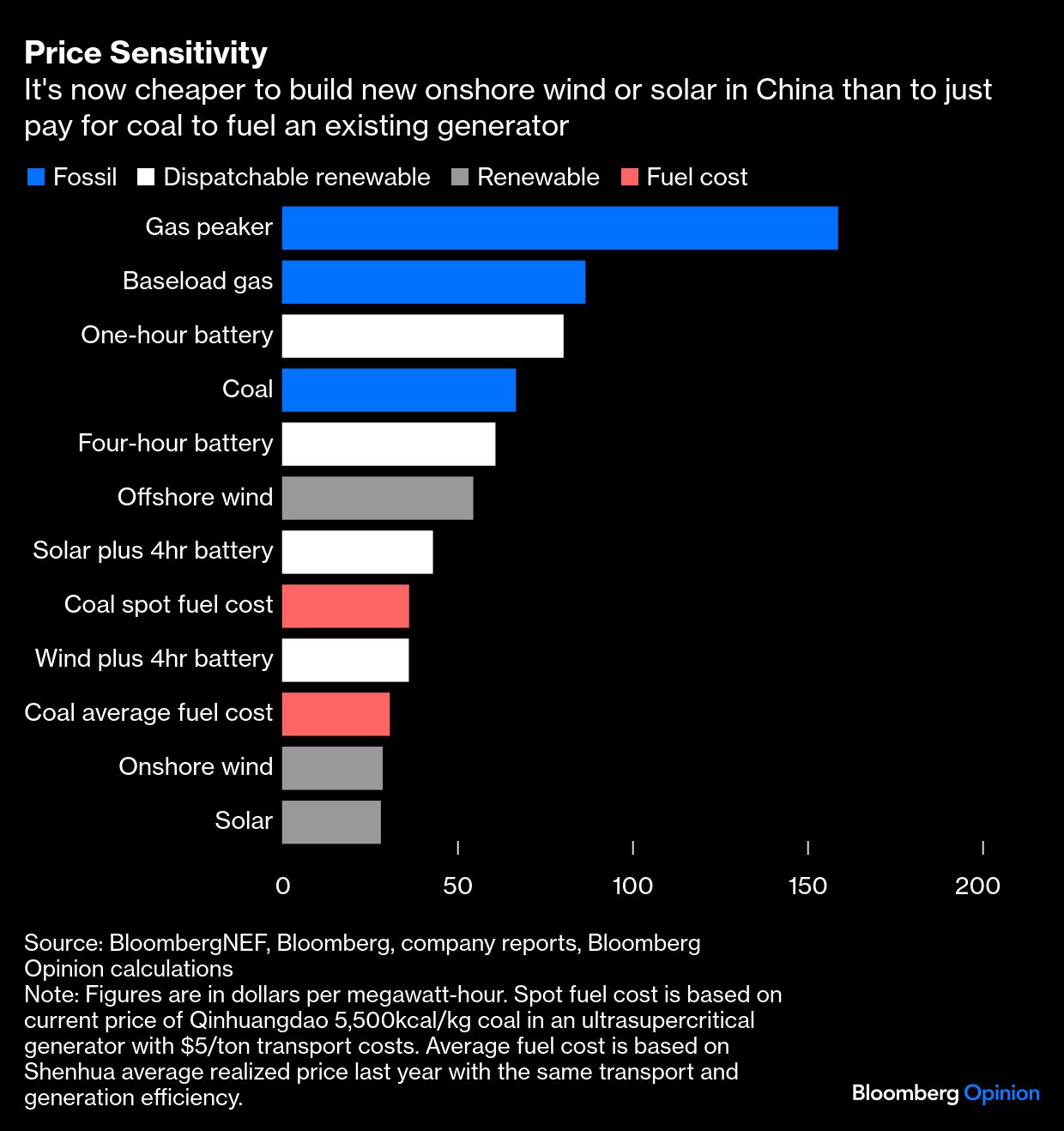

It costs less to build a new wind or solar plant these days than to buy just the soot to fuel an existing thermal power station, not to mention all its other capital and operating costs. Yet somehow, the number of new coal generators China starting building last year hit the highest level since 2015, at a time when the fundamental economics of fossil and renewable power were reversed.

What’s going on? The best explanation is that regulations have sheltered thermal power from the vagaries of the free market, while solar and wind are increasingly expected to stand alone.

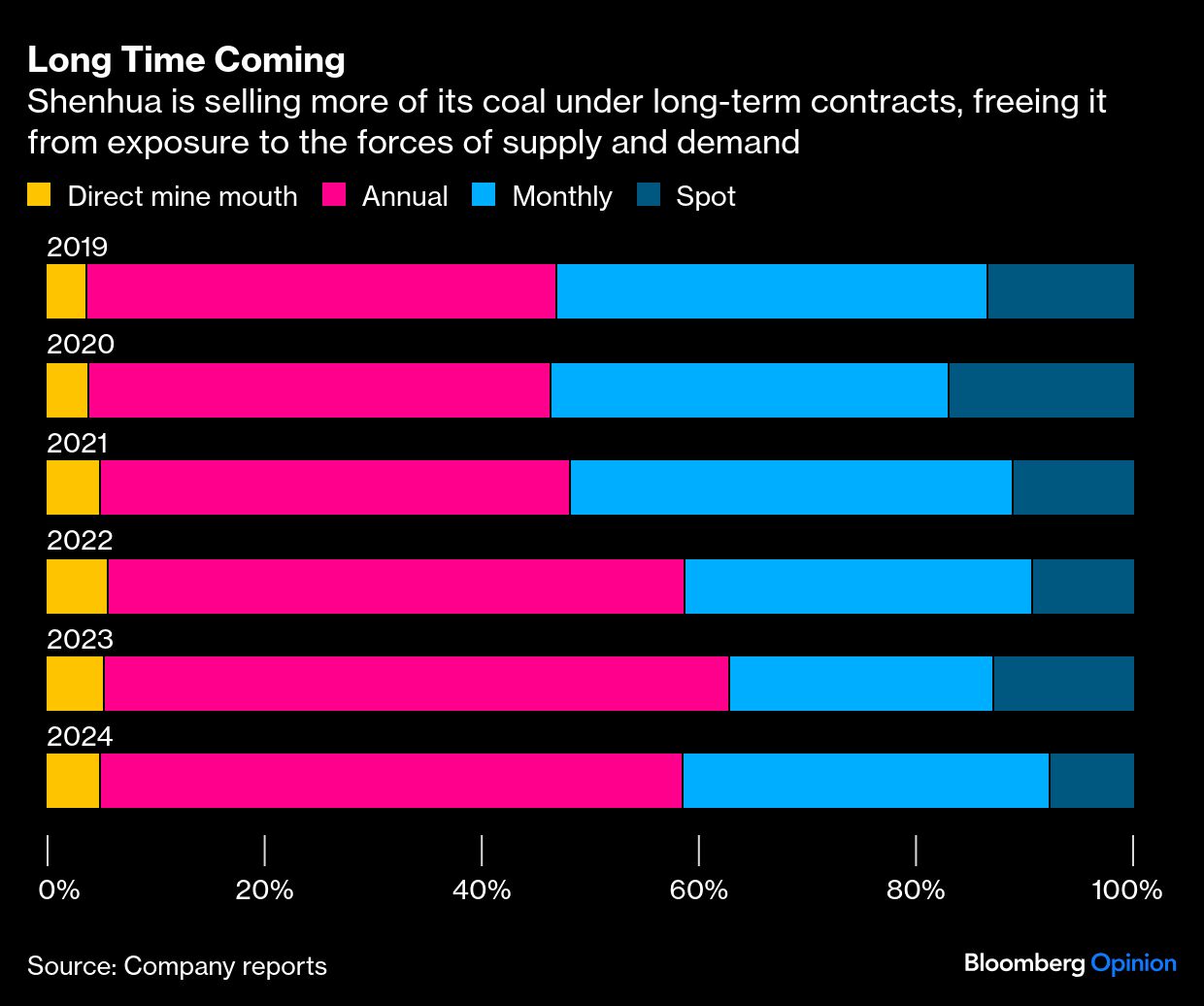

Since a run of power cuts in 2021 spooked Beijing, layer upon layer of rules have been implemented to keep coal in rude health. Generators were ordered to shift to long-term contracts, which lock in miners’ revenue years in advance. If you’re going to have to pay for fossil-fired kilowatt-hours anyway, you may as well switch on the furnace, even if cheaper renewables are available.

You can see the shift by looking at the financial statements of the country’s biggest coal miner China Shenhua Energy Co. The share sold on annual contracts has increased more than 10 percentage points since 2021.

Then there are capacity payments. These are a common feature of many markets experiencing a rapid shift to renewables, which compensate generators for keeping their fossil-fired plants on standby, ready to be sparked up to cover shortfalls in wind and solar. As with the long-term contracts, they’re a way of guaranteeing revenue.

In China, they are particularly generous. Since last year, coal plants have been able to recover 30% of their capital costs through such payments, recouped via a levy on customers’ bills. That share will rise to 50% from next year.

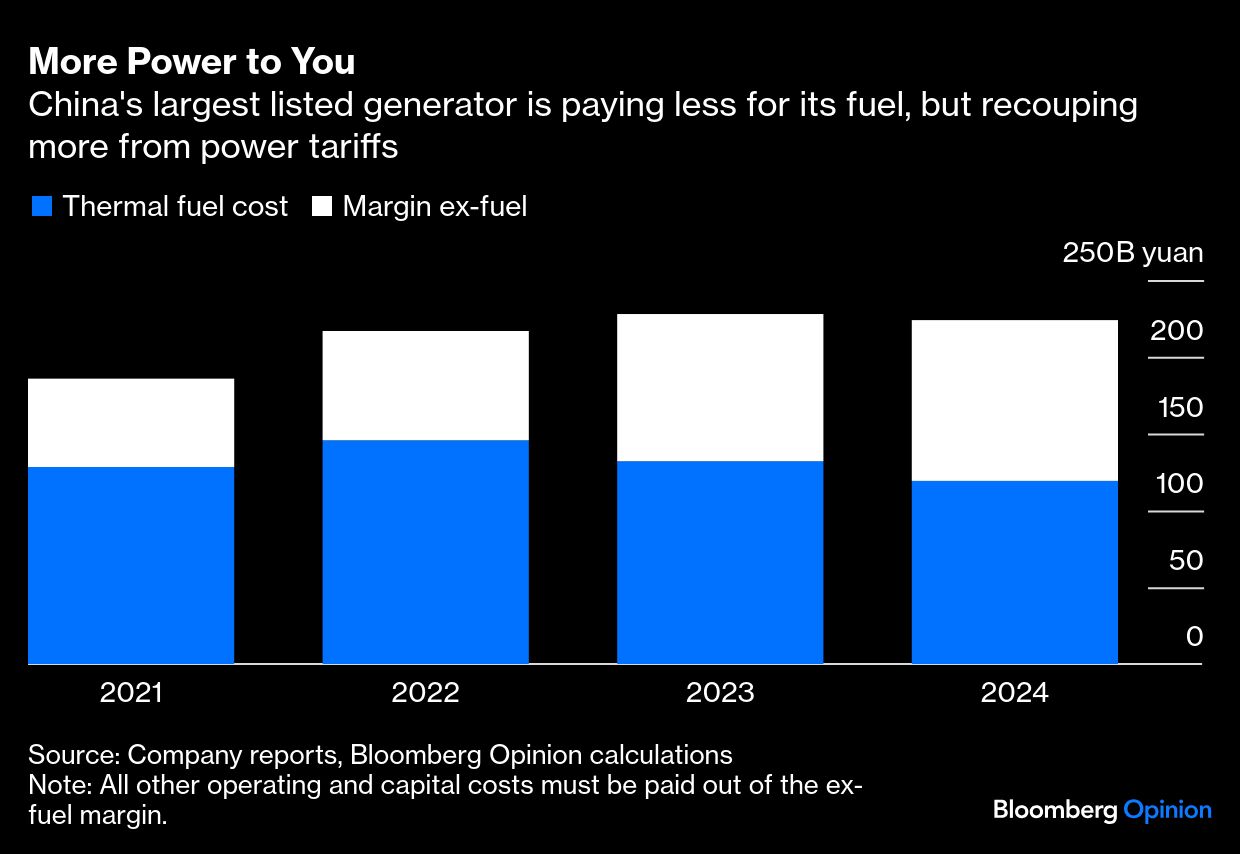

Once again, the effects are visible in companies’ financial statements. Huaneng Power International Inc., the biggest listed generator, has been able to push up power tariffs 14% since 2021, even as it generates a smaller share of fossil electricity. As a result, the margin out of which it has to pay its non-fuel costs has increased to 47%, from 31% in 2021. Put simply, it’s more profitable to burn coal than it was four years ago, despite the availability of cheaper and cleaner alternatives.

Renewables, meanwhile, are being exposed to the full force of the market. Subsidies for wind and solar were eliminated in 2021 so that developers received the same benchmark prices as coal. That wasn’t enough to hobble the energy transition — but the latest plan announced last month ratchets up the pressure further. This time, new renewable projects will be obliged to enter reverse auctions similar to those in Europe, the US and India, receiving prices that will always be lower than the coal benchmark.

Renewables’ fundamentally cheaper costs should favor them in a free market. But that’s not what’s on offer here. Instead, they’re going to be exposed to the full force of the grid’s red-in-tooth-and-claw volatility, while their incumbent coal-fired rivals are treated to the feather-bed of government-directed prices.

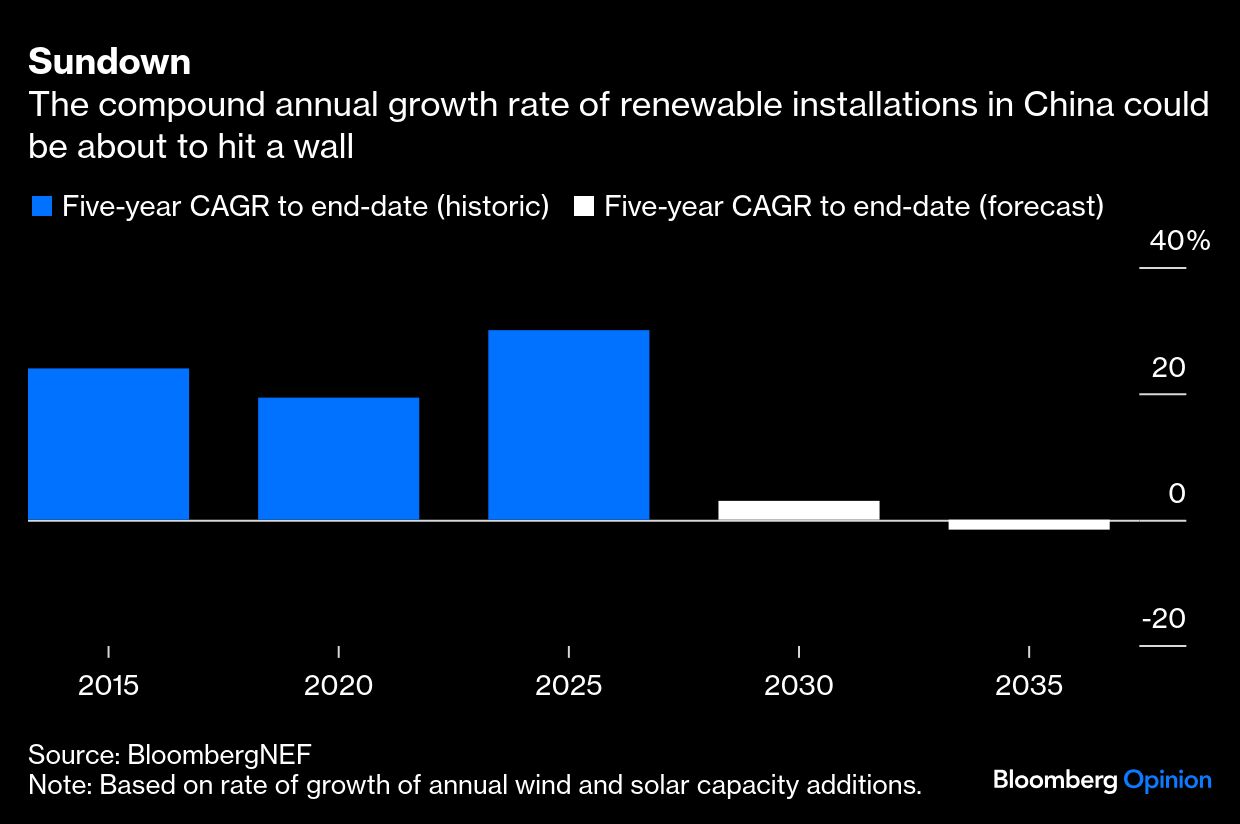

The results of the latest rules could be brutal. New renewable installations will “almost definitely” drop this year, according to David Fishman, an analyst at the Lantau Group, a consultancy. The China Photovoltaic Industry Association expects solar installations to fall as much as 23%, and in a worst-case scenario won’t recover to last year’s level until 2029. BloombergNEF reckons pre-existing projects will keep things stable this year, before a dramatic slowdown: They’re now forecasting a 3% compound growth rate for the second half of this decade, a brutal deceleration from the 30% pace since 2020.

The optimistic case for the energy transition is that the fundamentally lower costs of clean energy will always see it win out. The pessimistic case is that incumbents have remarkable ability to set the rules of the game to their advantage. We’re about to see a test of which side is right, in a power grid that accounts for about 15% of the entire planet’s emissions. The prospect is disturbing. Pile enough burdens on even the strongest player in a team, and eventually they’ll break.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All