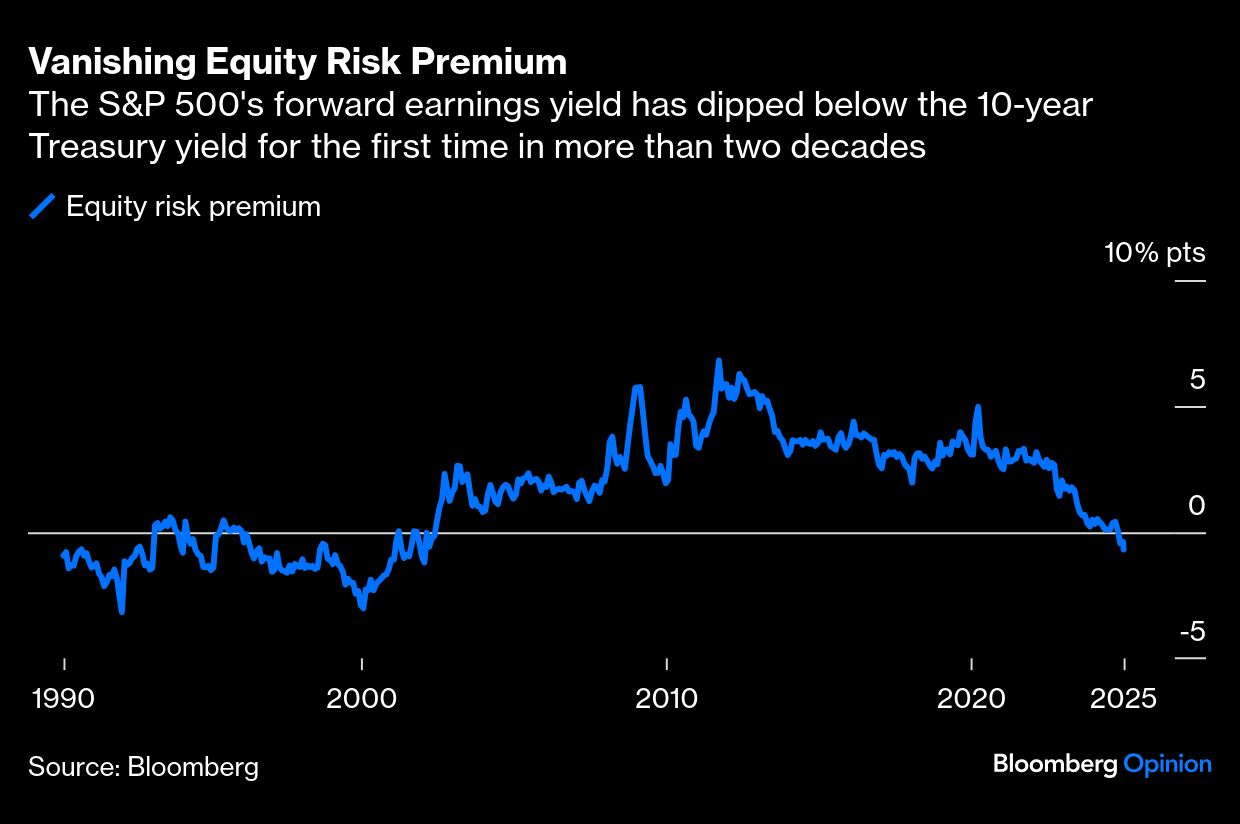

Stock investors have been watching the runup in US Treasury yields with considerable alarm of late. The widening premium of the 10-year yield over the earnings yield on the S&P 500 Index has garnered particular attention. It’s not supposed to be this way after all. Treasuries are broadly considered the world’s safest investment, whereas stocks are among the riskiest. Earnings yields are, therefore, normally higher than Treasury yields — what finance wonks call an equity risk premium.

But the equity risk premium turned negative late last year for the first time in more than two decades. The earnings yield, which is simply the inverse of the better-known price-earnings ratio, dipped down to 3.9% in November, based on Wall Street analysts’ consensus estimates for companies’ current fiscal year. Meanwhile, the 10-year Treasury yield drifted up to 4.4% and is now closer to 4.7%, while the S&P 500’s earnings yield hangs around 4%.

Implicit in the hand-wringing is that a negative equity risk premium is a bad omen for stocks. It has been historically, but not in the way you might fear or for the reason you might think. Importantly, it does not mean that a correction or more severe downturn is imminent. However, low or negative equity risk premiums have tended to be followed by lower-than-average stock returns over the medium term.

I looked at monthly equity risk premiums back to 1990 — the longest period for which analysts’ earnings estimates are available — and compared them with subsequent one-, three-, five- and 10-year total returns for the S&P 500. I found little or no correlation between the equity risk premium and subsequent one-year (0.09), three-year (0.18) or five-year returns (0.21). That suggests the equity risk premium is not a reliable signal for how the market is likely to perform this year or even over the next few years.

There is a moderate correlation, though, between the equity risk premium and subsequent 10-year returns (0.51), meaning that a lower equity risk premium tends to be followed by more muted medium-term stock returns. But the equity risk premium is a function of two variables, and it’s important when making investment decisions to understand if its predictive power is driven by earnings yields or Treasury yields, or some combination of the two.

To find out, I calculated the correlation between Treasury yields and subsequent stock returns, and then did the same thing using earnings yields. I found no correlation between Treasury yields and stock returns over one-, three- and five-year periods, and weak negative correlation between yields and subsequent 10-year returns (-0.13). In other words, the level of interest rates does not appear to signal future stock returns.

That must mean the equity risk premium’s predictive power lies in earnings yields, and that’s exactly what the data suggest. While the correlation between earnings yields and subsequent one-year stock returns is still weak (0.19), it strengthens over longer periods, approaching a near perfect correlation with subsequent 10-year returns (0.85).

The takeaway is that stock investors should pay more attention to valuations and less to interest rates. In fact, the level of interest rates dilutes the signal from valuations, as reflected in the fact that correlations with forward stock returns are higher for valuations alone than for the equity risk premium.

Those numbers shed light on some confusing past signals from the equity risk premium. For instance, the equity risk premium was negative during the early 1990s. Yet over subsequent 10-year periods beginning in 1990 to 1992, the S&P 500 returned anywhere between 9% and 19% a year.

One reason stocks performed so well in the 1990s was that the S&P 500 traded at just 13 times forward earnings when the decade began, resulting in a generous earnings yield of nearly 8%. The low valuation, however, may have been neglected by investors paying attention instead to the negative equity risk premium that resulted from a 10-year Treasury yield of 9%.

Applying those lessons to this moment, the trouble with the S&P 500 is not so much that the equity risk premium is negative or that interest rates are rising but that, at 25 times forward earnings, the index is expensive. That likely means medium-term returns will be lower than average from here, as many Wall Street banks and brokerages have already warned.

That doesn’t mean rising interest rates are not at all concerning. Highly levered investments, such as private equity and real estate, are less profitable — and some no longer viable — as borrowers are forced to pay more interest on their debt. The same goes for anyone with hefty debt, be they businesses, consumers or the US federal government. Higher interest costs, in the aggregate, could even drag down the broad economy.

But the stock market isn’t the economy. Profitable companies with manageable debt will continue to be good investments regardless of the level of interest rates — if investors don’t overpay for them.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar