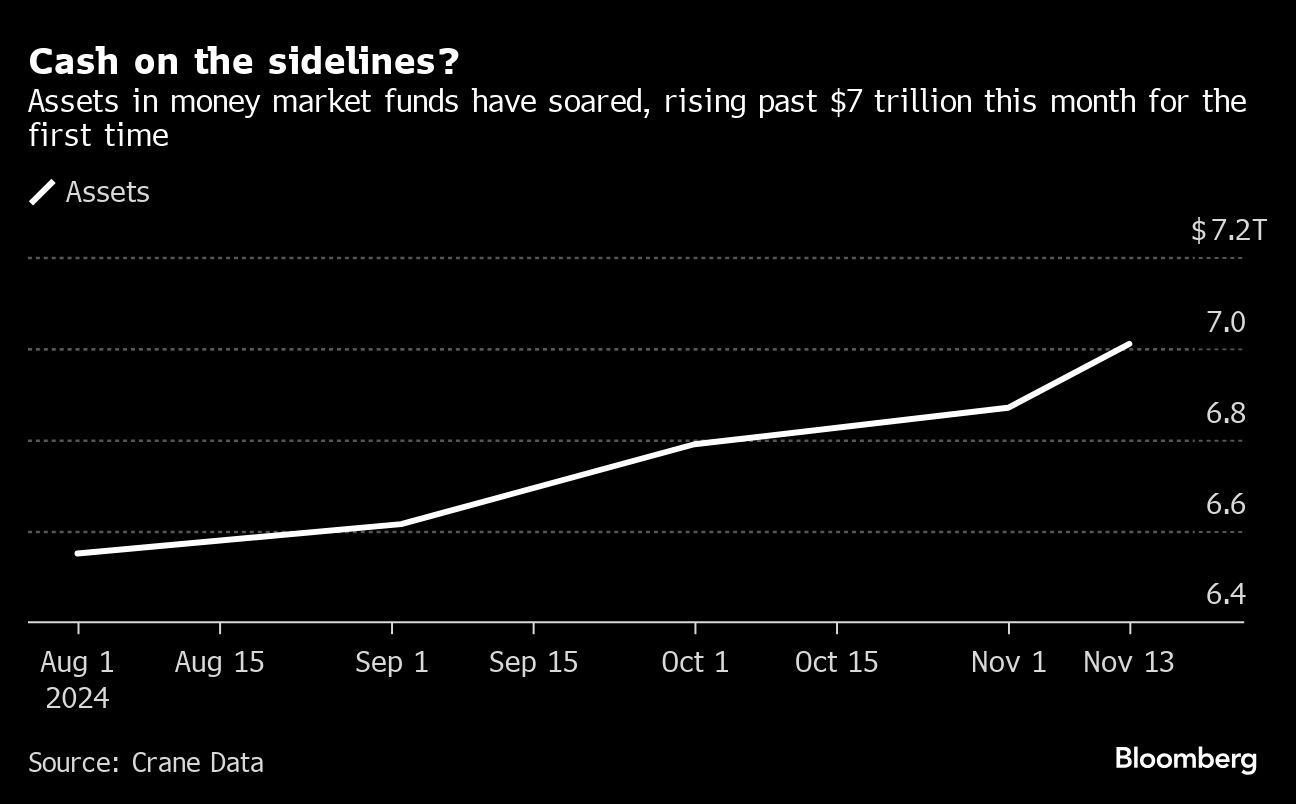

The money-market industry just reached a significant milestone with Crane Data reporting that these cash-like funds have amassed a record $7 trillion in assets. There are many ways to think about this development. One notion is that this huge sum represents “cash on the sidelines,” waiting to be unleashed into stocks, further fueling a bull market that has pushed major indexes to record highs. The idea is misguided.

A rudimentary Google search reveals that pretty much since the first money market fund was created in 1971, each new milestone has fired up equity market bulls. Their premise is simple: Who in their right mind would let cash sit in some fund earning miniscule interest rates thrown off by the safest investments including Treasury bills and commercial paper when there are infinite riches to be had in stocks? Surely these investors, or rather households, must be waiting for stocks to pull back before putting their cash into the market!

There’s little evidence to support that idea. In fact, retail investors are already bulled up. The Conference Board’s monthly consumer confidence survey, released this week, shows that 56.4% of respondents expect equities to be higher over the coming years, the highest percentage in records going back to 1987. While cash levels have risen by 38%, household stock holdings have surged by 50%, so the share of cash in portfolios has actually declined, according to Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors LLC. “This indicates that households are not, in fact, retreating into cash but are actively participating in equity markets with historically high exposures,” Suzuki wrote in a research note. So households’ cash-like holdings have little signal to offer equity bulls.

The picture is more muddled with big institutions. Suzuki noted that Bank of America Corp.’s global fund manager survey, released in October, showed such low cash holdings among institutional money managers — below 4% — that it triggered the firm’s contrarian equity market “sell” signal. But State Street Corp., with about $44 trillion of assets under custody or administration for institutions, is seeing something different. State Street’s monthly Institutional Investor Risk Appetite Index, derived from actual trades by clients, showed in October that the percentage of cash held by these institutions stood at 19%, in line with the average going back a decade. It’s a level that State Street considers “neutral” in terms of positioning. The average was almost 30% in 2007 (a great time to have been bearish) and as low as 10% in 2015 (a good time to have been bullish), according to DataTrek Research. Again, there’s little signal here for equity investors.

So what does all the cash parked in money market funds represent? For one, the rise largely tracks the growth in money supply, which has exploded in recent years as the US government created and spent trillions of dollars of fiscal stimulus to support the economy during and after the pandemic. As Suzuki notes, total household cash levels at some $18.4 trillion are almost three times the assets parked in these funds. It’s an amount that, he says, surpasses the annual combined revenues of the members of the S&P 500 Index and almost matches the federal government’s spending over the past three years.

And it’s likely that households are thrilled to earn a nearly risk-free 4.5% to 5% on their idle money after years of getting nothing due to the Federal Reserve’s zero interest rate policy. “The cash-on-the-sidelines narrative also doesn’t consider that, in recent years, cash has been an attractive alternative to bonds,” Suzuki wrote, referring to the fact that short-term yields have surpassed long-term Treasury yields for more than two years due to an anomaly in the fixed-income market.

Again, this is only part of the story. Much of this cash represents funds used to pay bills, not investment money, notes Jim Bianco of Bianco Research. “It’s growing because money keeps leaving traditional bank accounts, which pay almost no interest, for money market accounts, which pay market-based interest rates and offer the same flexibility as a checking account,” he wrote in a research note to clients. Some $1.29 trillion has left banks since the Fed started hiking rates, while money market funds have gained $1.79 trillion, according to Bianco. “Effectively, all the bank money plus two years of 5% interest rates, and direct deposits being shifted to money market accounts can explain nearly all of the gains in money market fund assets.”

Depending on how you measure it, the current bull market in stocks has been underway since October 2022, when the S&P 500 bottomed following a 25% slide, or since January, when it surpassed the previous record set in 2021. Either way, equities have had a tremendous rally and are considered expensive by historical measures. For stocks to march higher, companies will need to deliver on lofty earnings projections. Investors shouldn’t count on some pile of cash magically being funneled into the market.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.