Saturday marks two years since OpenAI posted an oddly named widget called ChatGPT to the web. Its staffers placed bets on how many users it would accumulate, the highest estimate being 100,000. How wrong they were.

ChatGPT quickly became the fastest-growing app in history, with about 200 million active users today. When it first came out, social media was ablaze with examples of how this fluent little text box was a leap ahead of Amazon Inc.’s Alexa or Apple Inc.’s Siri. It could write poems and high school essays. It would probably reshape Hollywood and the education system. Some of that has come to pass, with schools rethinking how they assign homework, for instance, while its impact on other areas of life and business is still an open question.

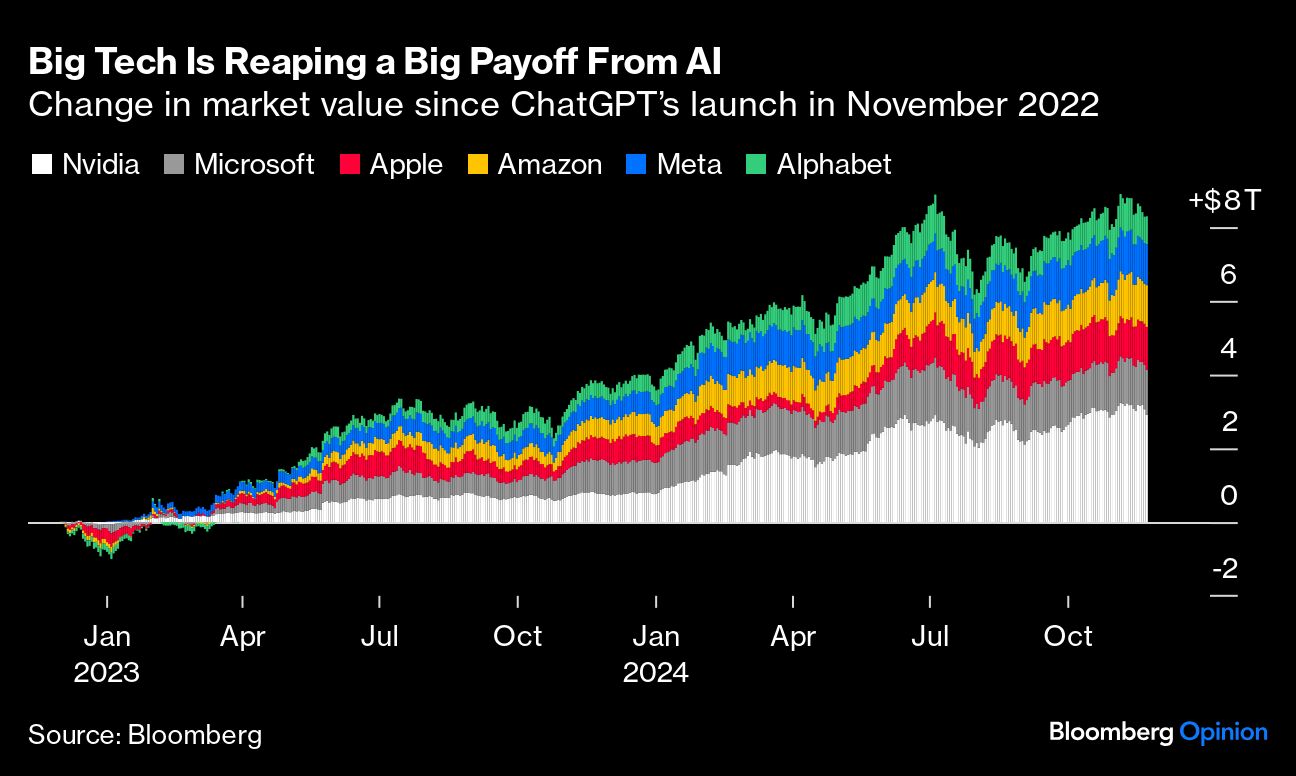

What’s clear is that in two years, the biggest beneficiaries of the kind of AI that will one day “benefit all humanity,” according to Sam Altman, are a handful of tech firms. The six biggest have seen their market capitalizations grow in aggregate by more than $8 trillion since ChatGPT’s launch.

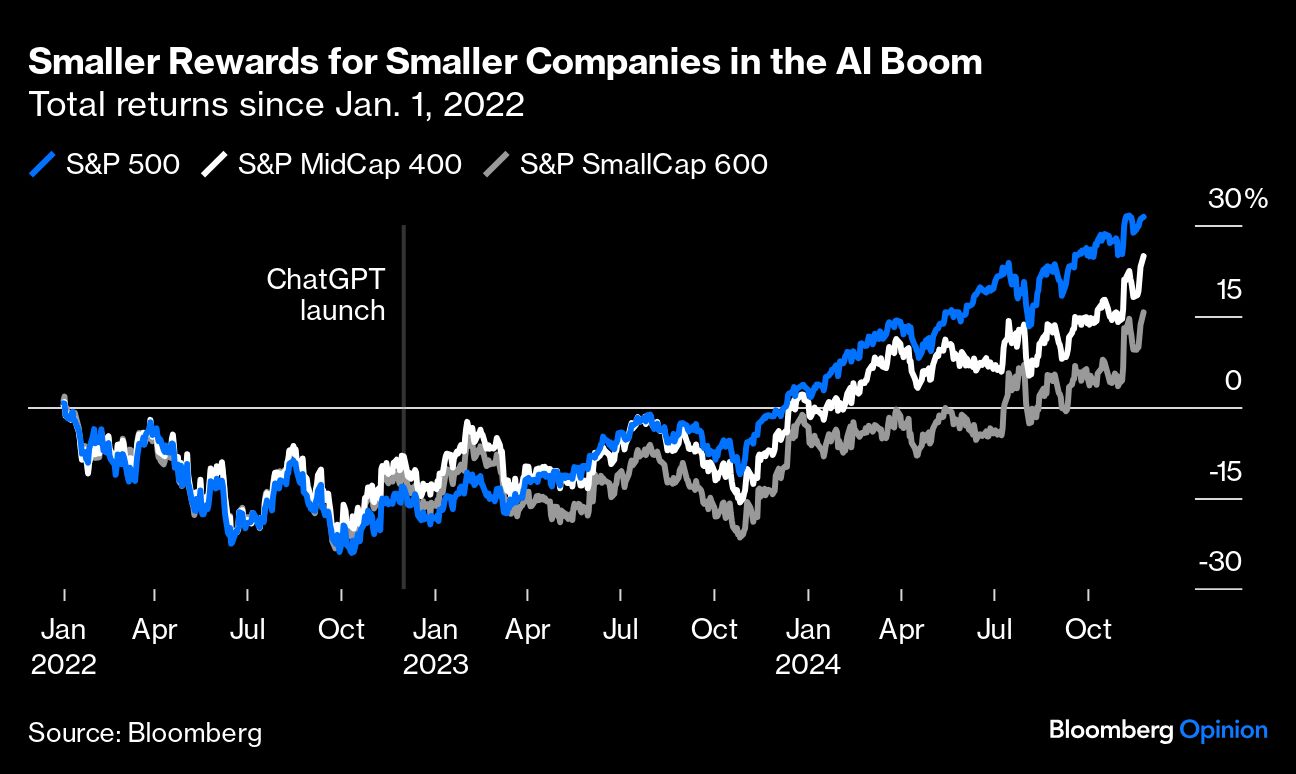

The tech sector has driven a 30% gain in the S&P 500 since January 2022, while small-cap companies have seen a more modest 15% return. That defies the trend of small- and mid-cap companies outperforming their larger counterparts over the two decades prior to ChatGPT’s launch.

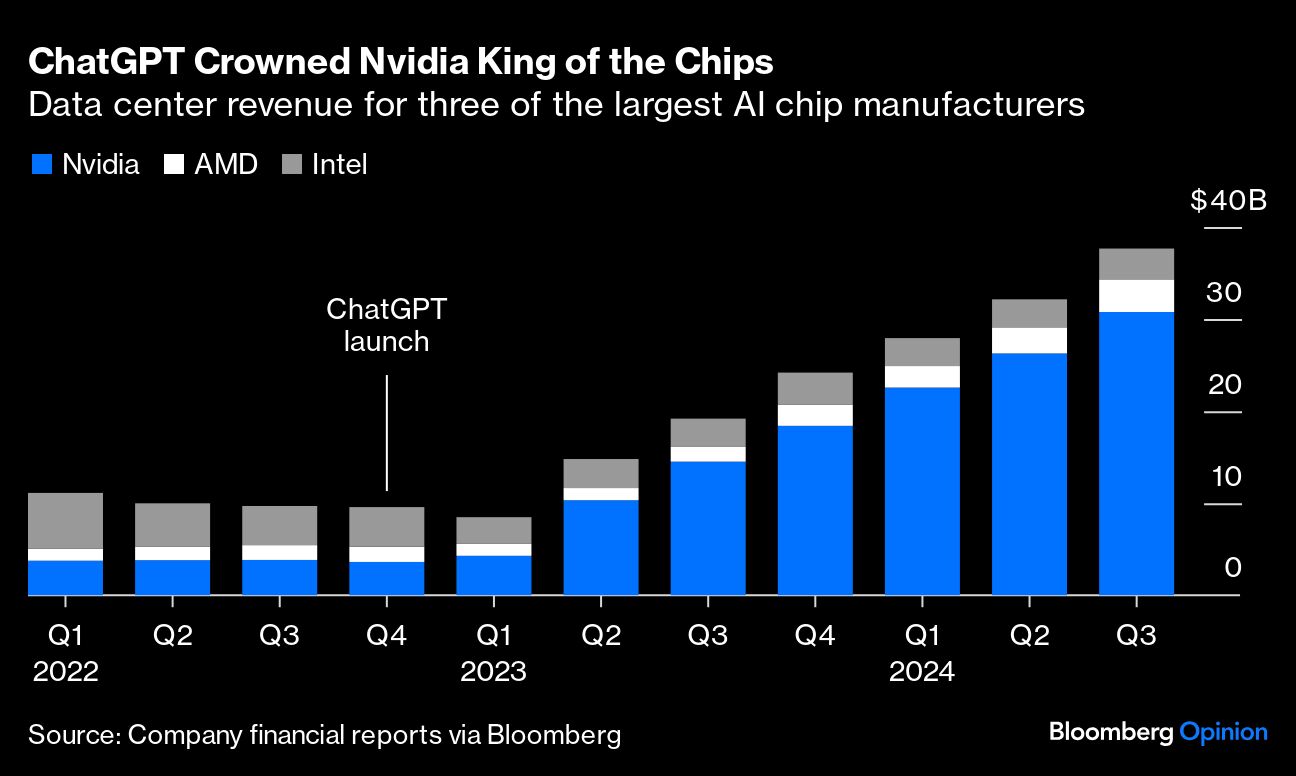

Nvidia Corp. has meanwhile leapfrogged Advanced Micro Devices Inc. and Intel Corp. to become the world’s top chip company.

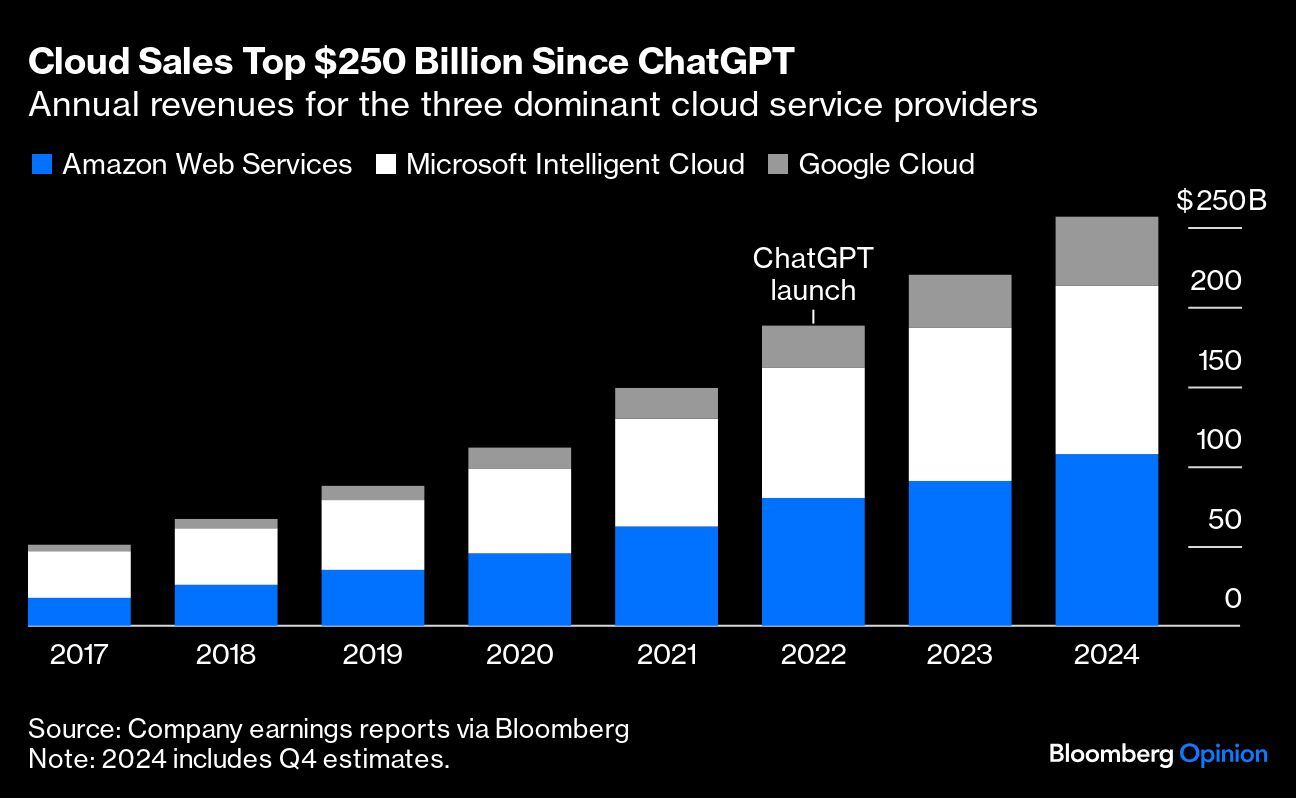

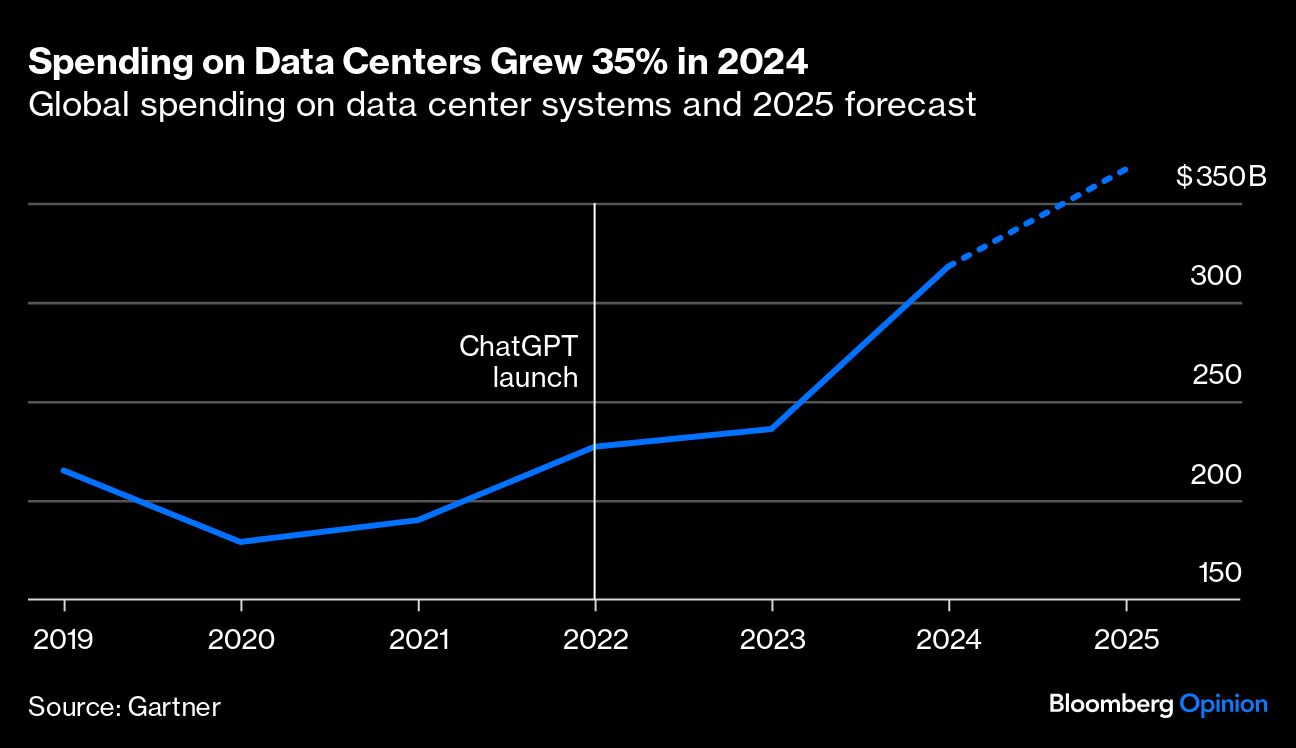

And cloud revenue has accelerated for Microsoft Inc., Amazon and Alphabet’s Google.

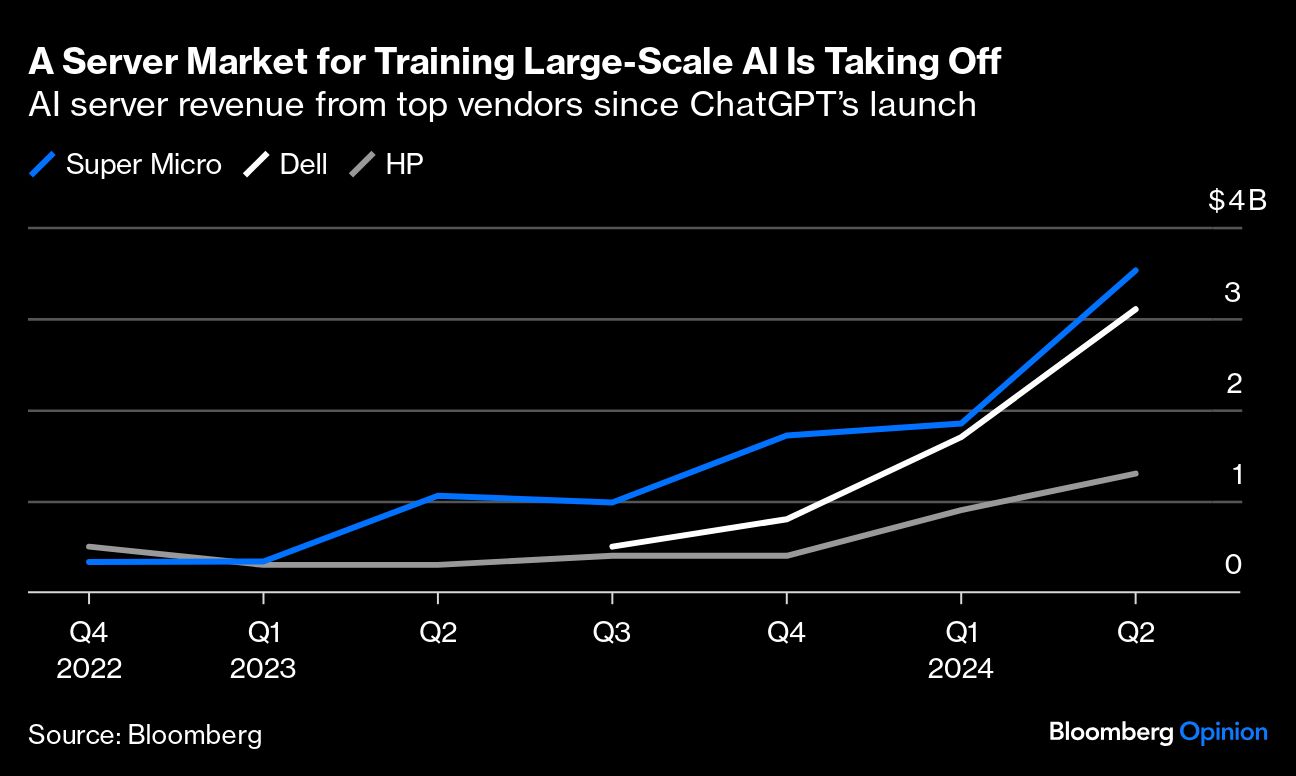

The charts in this column illustrate all the ways new money has flowed to tech giants and others in their orbit, from consultancy firms to server vendors like Dell Inc., as hype about an AI revolution gripped the market and sent businesses scrambling to remain competitive. That raises an uncomfortable prospect: that this supposedly revolutionary technology might never deliver on its promise of broad economic transformation, but instead just concentrate more wealth at the top.

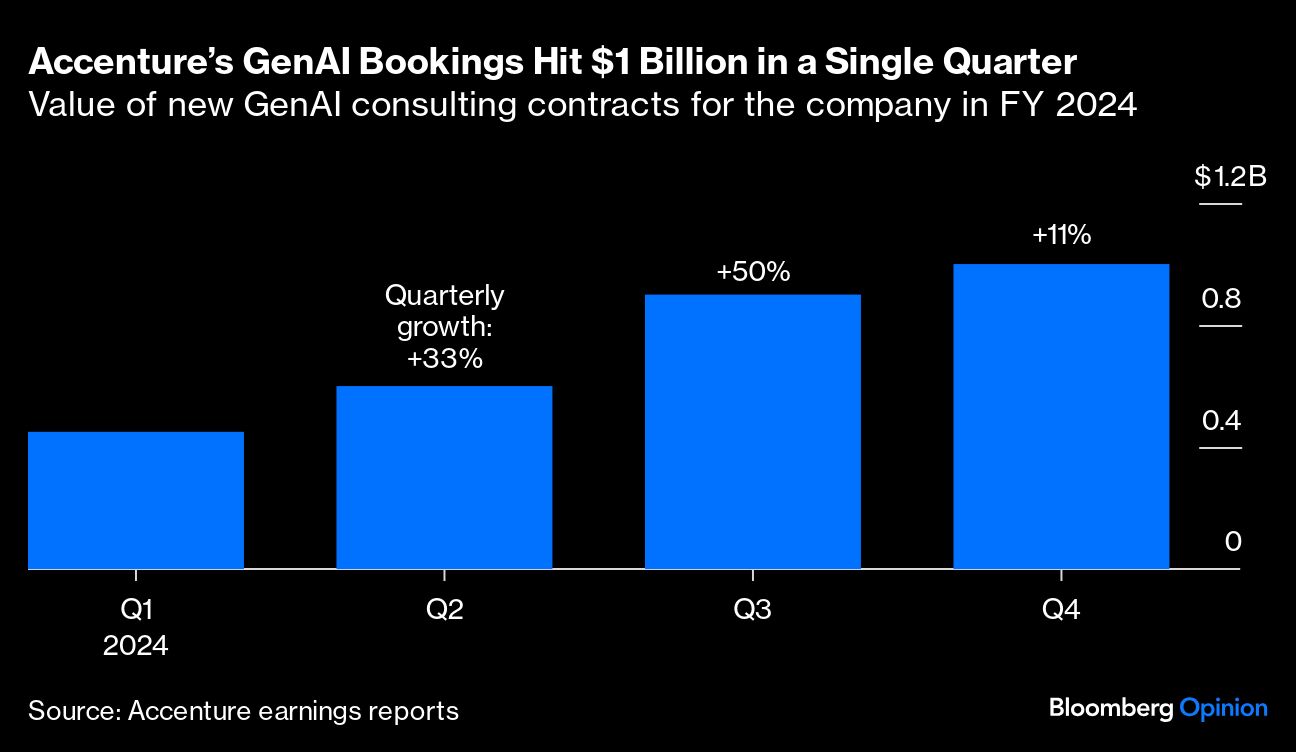

Consulting giants, a notoriously opportunistic bunch, have been the proverbial vendors of picks and shovels in this gold rush. About 40% of McKinsey’s business this year will be related to generative AI, according to The New York Times, while International Business Machines Corp. has seen its generative AI book of business jump to $3 billion, earlier this year. Accenture plc.’s gen AI bookings soared from $300 million in the last six months of 2023 to $1 billion for just the last quarter of 2024.

A healthier outcome from all this would be for startups and non-tech firms to capture more of these rewards — AI is meant to be transformative for them after all. But doing so remains difficult. Already, building a business around apps or enterprise software is risky because of the possibility that a tech giant will release the same feature and drive them to insolvency. App builders famously hate watching Apple’s World Wild Developers Conference — its annual showcase of new software features — out of fear that their startup idea will now come standard with iPhones.

The situation is arguably worse for the new crop of entrepreneurs. It’s prohibitively expensive to be in the business of building “foundation models” that compete with ChatGPT, Google’s Gemini, Anthropic’s Claude or Meta Platforms Inc.’s Llama, products that barely have a moat.

So most founders of generative AI startups focus on building services that act as a “wrapper” around existing models like OpenAI’s GPT-4, which itself underpins ChatGPT. The problem is that they too run the risk of being snuffed out by a larger player aping their product. When OpenAI released Whisper in 2022, for free, it made life more difficult for a whole swathe of speech-recognition startups.

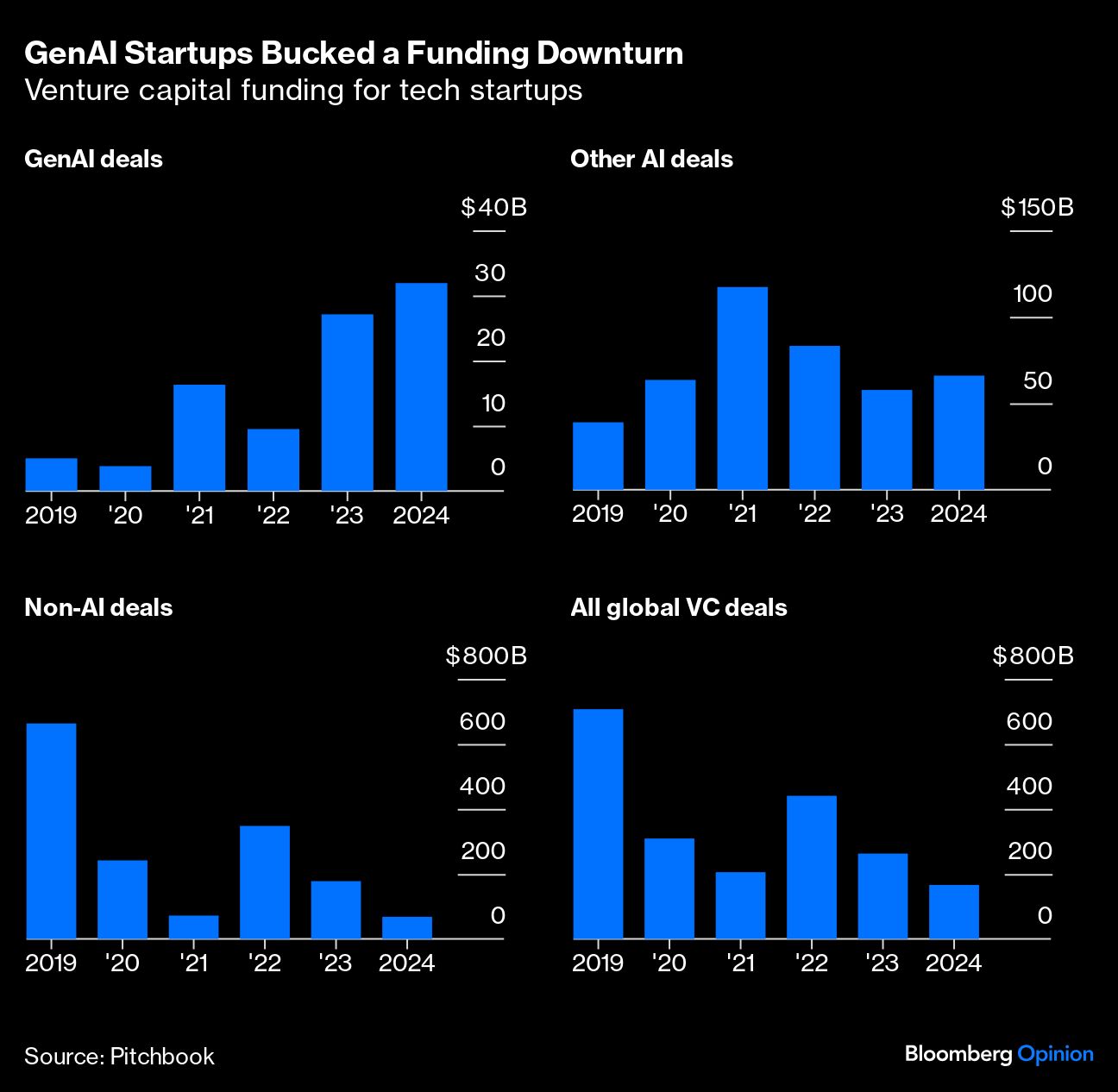

Entrepreneurs building generative AI products are, at least, sucking up a bigger proportion of venture capital funding, even as higher interest rates led to a decline in startup funding over the past year. But they must still find ways to inoculate themselves from the dominant players.

One way is to focus on building niche products for areas like healthcare, law and finance. Those narrow use cases are harder for Microsoft and Google to go after, given their focus on building general-purpose AI systems.

There’s further reason for optimism that a stranglehold on AI by incumbents might loosen. Tech firms are talking more about a shift toward selling smaller AI models focused more on specific tasks. It’s an approach lauded by AI safety advocates like Max Tegmark, who argues that the all-knowing, God-like AI systems that tech giants are chasing will eventually prove disastrous for civilization. It so happens that smaller models are cheaper and easier to steer for accuracy’s sake.

A recent plateauing in AI’s capabilities means businesses could also have more breathing space to try and plug generative AI into their processes, and scrutinize it for a return on investment.

Two years after capturing the public’s imagination, it seems ChatGPT’s main legacy has been in padding the finances of tech’s biggest players. The next phase of AI may prove more democratic, as smaller, specialized models lower the barriers to entry. But for now, the revolution that was meant to reshape our world has mostly extended Big Tech’s wealth and influence. Who would have guessed that AI’s most astounding feature would be making the world’s most powerful companies even more powerful.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.