In a corner of the credit market that regulators last year characterized as a potential hot-bed of greenwashing, there are signs that bankers have been cracking down on corporate pitches.

Paul O’Connor, head of EMEA sustainable finance, debt capital markets at JPMorgan Chase & Co., says corporate clients are now taking the time to “properly” put together their pitches for so-called sustainability-linked loans. As a result, the market is seeing “more sensible structures,” he said.

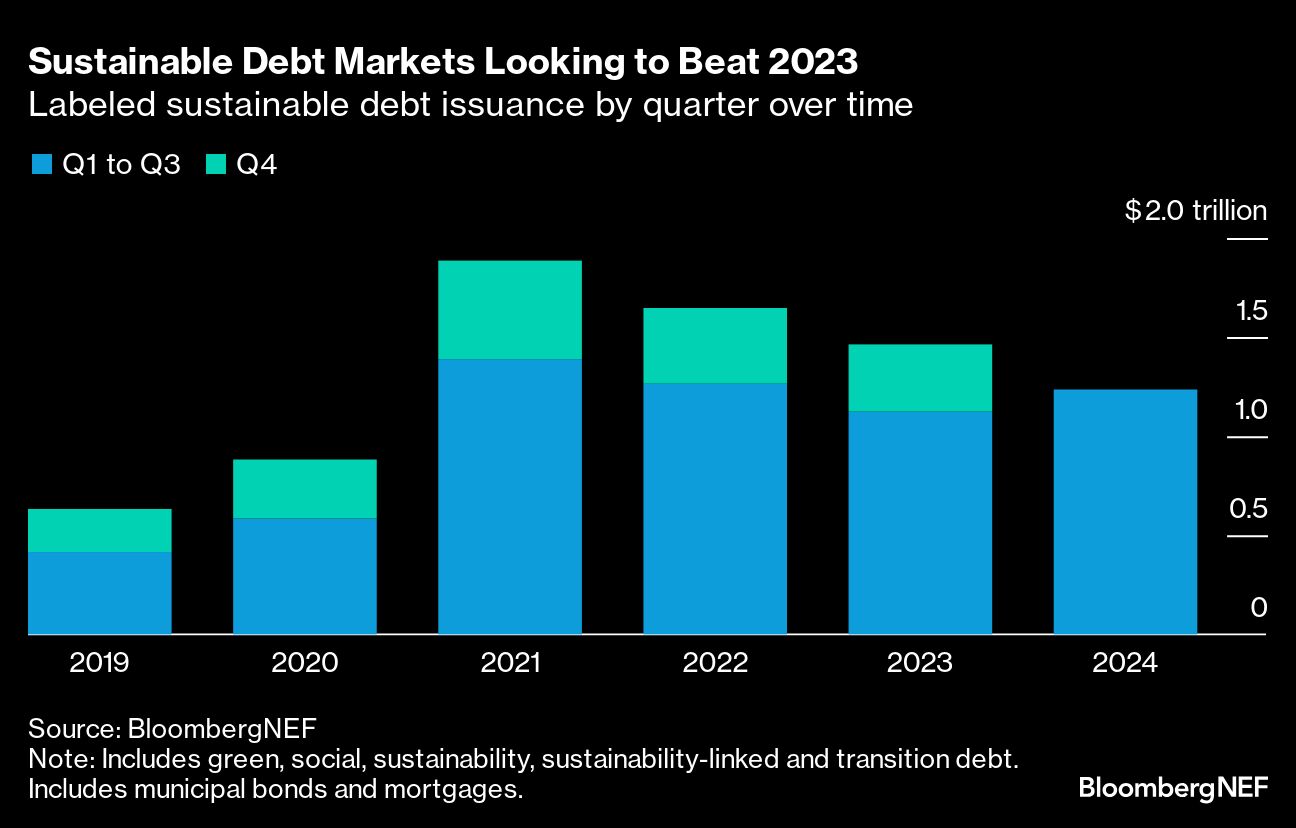

SLLs form one of the least regulated corners of ESG finance. They’re also one of the biggest. Since the first SLL was arranged roughly seven years ago, the market for such loans has grown to almost $1.8 trillion, according to data compiled by BloombergNEF.

“The fear has receded a bit as people have gained experience and they are a bit more confident now about coming forward with these things,” O’Connor said in an interview.

Sustainability-linked loans are supposed to have environmental, social or governance conditions attached, such as emissions reductions. Failure to meet those goals can trigger penalties, for example, in the form of higher interest rates.

To date, there are very few records of SLL targets having been missed or penalties imposed, in large part because the loan agreements generally take place behind closed doors. Among the few to have been made public are SLLs by Enel SpA, which were triggered along with its sustainability-linked bonds earlier this year.

The Loan Market Association provides voluntary guidelines to stipulate that sustainable performance targets attached to SLLs need to be “ambitious, material and quantifiable.”

Last year, however, the UK’s Financial Conduct Authority issued a warning to the SLL market, which it said risked being the subject of “accusations of greenwashing” due to “weak incentives, potential conflicts of interest” and basic “poor design” in some corners of the market.

So far this year, JPMorgan has arranged more than $24 billion worth of SLLs, compared with about $12.7 billion in all of 2023, according to data compiled by Bloomberg. Bank of America Corp. has arranged about $23 billion through the end of October this year, versus roughly $18 billion for Citigroup Inc. and just over $16 billion for Wells Fargo & Co., the data show.

Philip Brown, head of sustainable debt capital markets at Citigroup, told Bloomberg that “the market and governance for sustainability-linked products is maturing and we see well-structured sustainability-linked finance continuing to be an important funding tool for some clients.”

A spokesperson for Bank of America declined to comment.

At Wells Fargo, bankers are looking at SLL pitches from clients in “new segments, most notably fund finance, real estate, energy, and private and middle-market companies in sync with the development of sector-specific sustainability strategies,” said Genevieve Piche, head of sustainable finance and advisory in corporate and investment banking at the San Francisco-based lender.

She says refinancings from established sustainable finance borrowers “contribute to stability in volumes.” However, publicly available data may actually understate the pace of SLL growth, with new deals often “not reported for league tables.”

O’Connor, who declined to provide details of JPMorgan’s deals, said the bank sees a market that’s settling into a more sedate pace of issuance.

Between 2018 and 2021, the SLL market soared more than 984% to $531 billion of annual deals; between 2020 and 2021 alone, the increase was more than 300%, according to BNEF data.

“I think we’re unlikely to see a big jump like we did between 2020 and 2021,” O’Connor said.

What’s really going on in the SLL market can be hard to pin down, though, given the lack of reporting requirements for such deals. Data compiled by Bloomberg, which is largely based on revolving credit facilities carrying SLL labels, indicates growth of roughly 10% this year.

Piche at Wells Fargo says the Biden administration’s 2022 Inflation Reduction Act is part of a package of climate-friendly legislation that is spurring demand for SLLs. Others include the Bilateral Infrastructure Law and the CHIPS Act, she said.

“Complementary to KPI-based SLLs, we’re seeing demand from some corporates for revolving credit facilities available for both general purpose as well as for a mutually agreed short list of strategically-aligned green initiatives,” Piche said.

Meanwhile, banks are increasingly looking into so-called SLL bonds, a structure first tested by Nordea Bank Abp in 2022. The LMA says sustainability-linked loan bonds should live up to similar use-of-proceeds principles as those that apply to green bonds.

The prospect of issuing SLLBs serves as “a bit of a motivator for some banks to actually start promoting these structures to their clients,” O’Connor said. But the bonds “will only work if the underlying portfolio of sustainability linked loans is high quality.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Alastair Marsh