If you’re unfamiliar with synthetic risk transfers, there’s a chance you’ll hear all about them when the next financial crisis hits. They’re the latest way for big banks to game rules designed to safeguard the system, and they’re growing fast. So far, regulators seem all but oblivious.

Financial resilience depends largely on one line in banks’ balance sheets: equity. Also known as capital, it’s funding from shareholders who, unlike creditors, have agreed to absorb losses. The more equity banks have, the better they’re able to keep lending in difficult times. Bank managers, however, prefer to use more debt, because it comes with various government subsidies and boosts key profitability measures in good times.

The largest global banks have lately been very successful in minimizing equity. They’ve fended off plans for incremental increases in both the US and Europe. As a result, their capital typically amounts to about 5% to 6% of assets, far less than what experts and research indicate would be needed to weather a severe crisis.

Yet the banks think that’s still too much. They’ve revived a practice from before the 2008 subprime-mortgage crisis: Reduce capital requirements by repackaging loans into securities and buying protection against losses from other financial institutions. The banks keep the assets, the risk purportedly goes elsewhere. Hence, synthetic risk transfer.

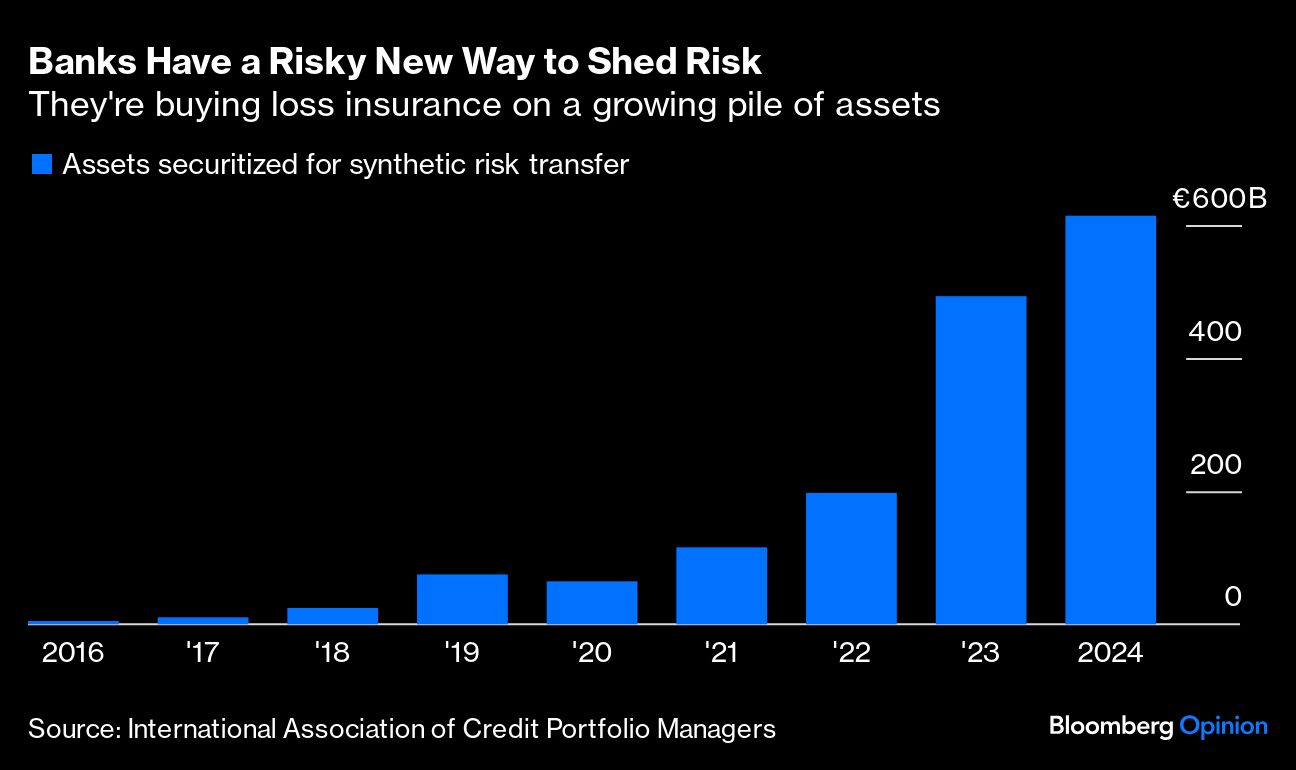

It's booming. The relevant pool of synthetically securitized assets amounted to €614 billion ($661 billion) at the end of 2023, up from just €5 billion seven years earlier. European corporate loans dominate, followed by auto and other retail loans in the US. Sellers of insurance, including private credit and pension funds, enjoy returns of 8% to 12%.

The insurance has legitimate uses, such as rebalancing banks’ exposures. But it entails its own risks. Unlike equity, it doesn’t absorb any and all losses. It applies only to the designated assets, and it could prove worthless in a crisis if the counterparty can’t pay. That’s what almost happened with insurer American International Group in 2008, necessitating one of the largest bailouts in US history.

Worse, there’s a twist. As Bloomberg News has reported, banks are lending to the same nonbank financial institutions that are providing the insurance — meaning that in aggregate, some of the risk isn’t leaving the banking system at all. While the magnitude of such “round tripping” is hard to know, overall bank credit to nonbanks has grown sharply in recent years. In the US, it amounted to more than $1.8 trillion in 2022.

One might expect regulators to be sounding the alarm. On the contrary, the European Central Bank is working to facilitate synthetic risk transfers, despite its own finding that banks don’t fully understand their exposures to the counterparties. Europe needs more securitization to boost investment, but it should involve transparent asset sales, not opaque contracts of uncertain value.

At the very least, as the International Monetary Fund urges, regulators should require the disclosure needed to assess the largely private transactions and their potential systemic risks. Ultimately, they should insist on equity, rather than settling for poor substitutes. There’s nothing like the real thing.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors