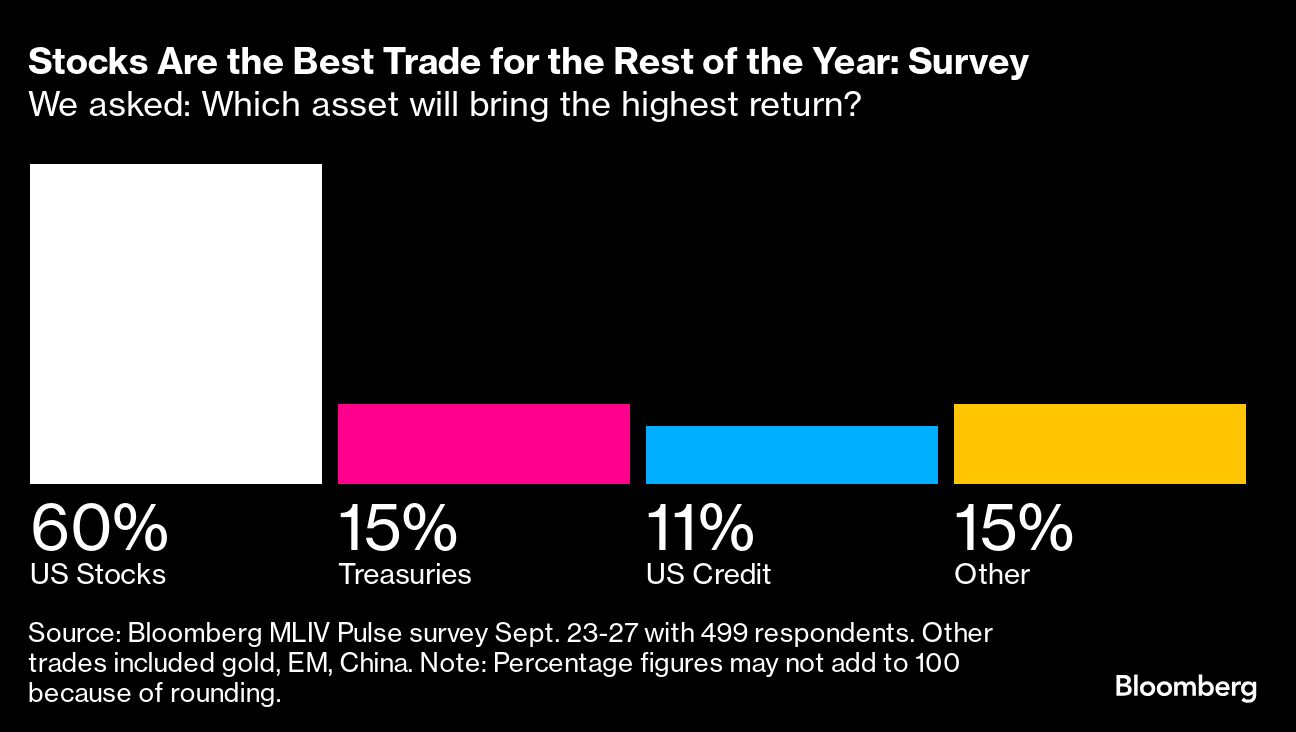

US stocks will outperform the nation’s government and corporate bonds for the rest of this year as the Federal Reserve keeps cutting interest rates, the latest Bloomberg Markets Live Pulse survey shows.

Exactly 60% of the 499 respondents said they expect US equities will deliver the best returns in the fourth quarter. Outside of the US, 59% said they prefer emerging markets to developed ones. And as they ramp up these bets, they’re avoiding traditional ports of calm, such as Treasuries, the dollar and gold.

It’s a risk-on view that dovetails with bullish calls emerging on Wall Street following the Fed’s half-point rate cut this month. China’s biggest stock rally since 2008 after Xi Jinping’s government ramped up economic stimulus also helped boost the bullish attitude.

“The biggest challenge that the US economy has been facing is actually high short-term interest rates,” said Yung-Yu Ma, chief investment officer at BMO Wealth Management. “We’d already been leaning into risk assets and leaning into US equity,” he said, and “if there were a pullback, we would consider even adding to that.”

The Fed slashed its benchmark rate from the highest level in two decades on Sept. 18, and the median official forecast projected an additional half-point of easing across the two remaining 2024 meetings, in November and December.

‘Room to Cut’

The MLIV Pulse survey showed that 59% expect the Fed to deliver quarter-point cuts at each of those two gatherings. Thirty-four percent anticipate steeper reductions in that period, totaling three-quarters of a point or a full point. That’s more in line with swaps traders, who are pricing in a total of around three-quarters of a point of cuts by year-end.

Investor confidence that the Fed can engineer a soft landing has grown, putting the S&P 500 Index on track to gain in September — historically the gauge’s worst month of the year — for the first time since 2019.

“The Fed has a lot of room to cut as do many other central banks,” said Lindsay Rosner, head of multi-sector investing at Goldman Sachs Asset Management. “That sets up a good backdrop for the economy in the US, in particular. That doesn’t erase the tightness of valuations, but makes them more justifiable.”

When asked which trade is best to avoid for the rest of the year, 36% — the biggest group — cited buying oil. Crude has slumped because of concern that rising production outside of the OPEC+ alliance will create an oversupply next year. The runner-up was buying Treasuries, with 29%.

Treasuries are still on course to gain for the fifth straight month. And while rate cuts can buoy bonds, there are plenty of questions about fixed income given diverging views around how quickly the central bank will drop borrowing costs, with the job market proving resilient. Investors are particularly wary of long-term Treasuries, given the risk that inflation could heat up again as the Fed eases.

What Bloomberg strategists say ...

“Term premium of longer-dated Treasuries is set to rise, while liquidity risks — already heightened as the government runs persistently large fiscal deficits — is likely to deteriorate.”

- Simon White, Macro Strategist on MLIV

The survey also showed limited enthusiasm for the US dollar, another traditional haven asset. Eighty percent of respondents expect the greenback to end the year either roughly flat or down more than 1%. The Bloomberg Dollar Spot Index is up less than 1% year-to-date.

The MLIV Pulse survey was conducted Sept. 23-27 among Bloomberg News terminal and online readers worldwide who chose to engage with the survey, and included portfolio managers, economists and retail investors. This week, the survey asks if the worst is over for commercial real estate debt.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.