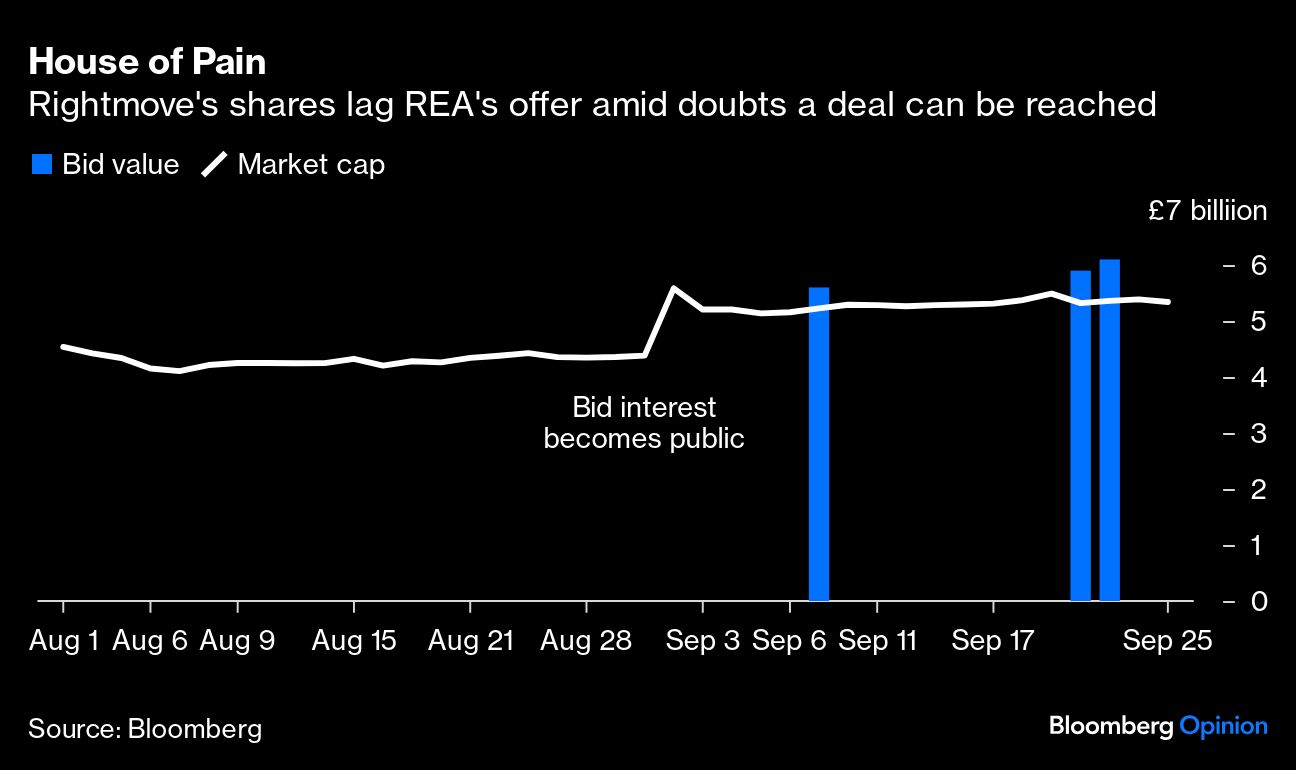

(Bloomberg Opinion) -- Rupert Murdoch has so far made it easy for Rightmove Plc to resist his takeover bid. Three weak overtures have put little pressure on the UK real estate website’s board, which has yet to agree to start talks. If the media tycoon wants to win the battle, he must now deliver one decisive bump.

Australia-listed REA Group Ltd., controlled by Murdoch’s News Corp., is using the standard tactic in UK mergers and acquisitions — go in low and then publicly inch higher, doubtless hoping Rightmove’s shareholders will nudge the company to the negotiating table (as some now are). The first cash-and-shares pitch was priced at a futile sub-30% premium over Rightmove’s value before Murdoch’s interest became public last month. The third, rejected this week, was worth 761 pence a share based on REA’s share price at the beginning of this week. That equates to a 37% premium, valuing Rightmove at £6 billion ($8 billion).

That’s far from knockout territory. It’s attractive if you think Rightmove shares have little chance of hitting that level in the foreseeable future. True, Rightmove has essentially gone nowhere in the last five years, so you might well harbor such doubts. But the rearview mirror is unhelpful here. Rightmove is a relatively young company; it gained its first external chief executive officer, Johan Svanstrom, only last year. He’s diversifying away from residential property ads into mortgage broking, commercial property and services for landlords. The company had put hard numbers on this strategy before takeover interest surfaced, including targeting £420 million of operating profit in 2028. That would be more than 50% over its expected level this year.

Were Murdoch dangling an all-cash offer, it might be a tempting alternative to gambling on Svanstrom dragging Rightmove out of its rut. But REA is looking to pay mainly in its own stock. Some of Rightmove’s shares are likely held by fund managers with mandates forbidding non-UK-based companies. They’d have to sell, despite REA promising a London listing. The more that do, the more that would weigh on REA’s stock price, lowering the real-world value of the takeover.

Rightmove investors who can hold Australian paper face the separate worry that REA’s enviable valuation – a multiple of forecast profit well ahead of peers – is so high it can only go one way: down. They too may just dump any REA stock received as payment.