The Federal Reserve is widely expected to begin cutting interest rates this week as moderating inflation allows the central bank to roll back some of its previous rate increases. I expect that some investors will be tempted to chase stocks given the stubborn conventional wisdom that interest rates and stock prices move in opposite directions. They should reconsider.

The theory is that stock prices reflect the present value of companies’ future earnings, a calculation that relies in part on prevailing interest rates to “discount” future earnings to the present. As the math goes, the lower the interest rate, the more future money is worth today, and vice versa. By extension, growth stocks should be more sensitive to interest rates than value ones because faster-growing companies generate more earnings in the future.

The problem is the available data doesn’t seem to agree, at least when it comes to rising rates. In 2022, I looked at how the stock market fared during the Fed’s 13 rate-hiking campaigns since 1954 and found that the S&P 500 Index was higher on 11 of those occasions. I also looked at how growth and value stocks performed during those 13 episodes and found that growth won in three of the last four. So much for theory.

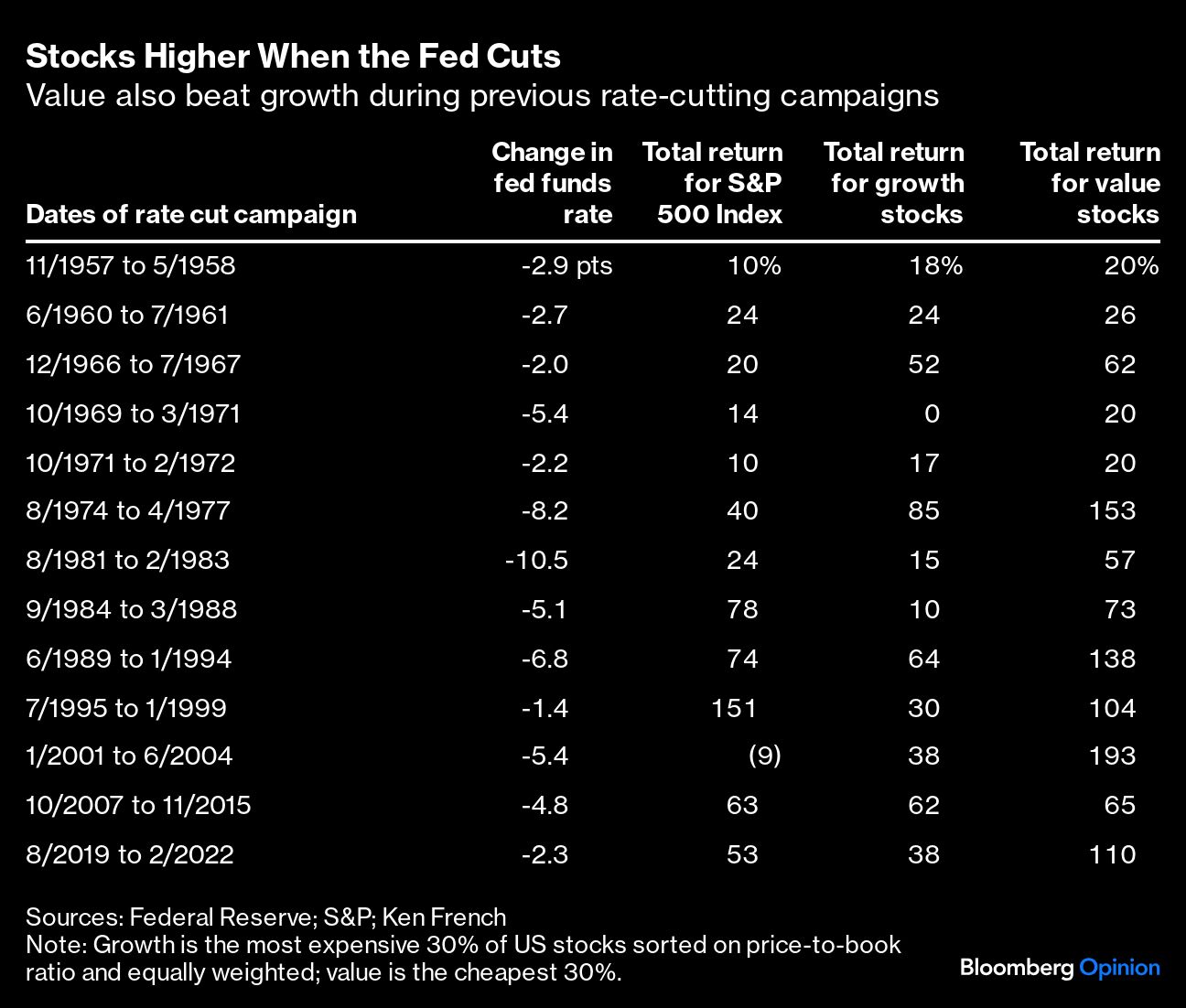

With interest rates now headed lower, I decided to look at how stocks performed during the Fed’s rate-cutting campaigns and up to the point when rates begin rising again over the same period. This time, the record is more supportive. As the following table shows, the S&P 500 posted a positive total return on 12 of 13 occasions. Value beat growth every time.

What investors should do with that information is less clear, but raising their allocation to stocks in anticipation of lower rates is probably a mistake for several reasons.

First, no one knows how much the Fed will cut on Wednesday or what it will do next. Inflation may remain subdued, in which case the Fed can continue to cut. But it might also remain stubbornly above the Fed’s 2% target for an extended period, or even move higher. After the inflation scare of 2021 and 2022, the central bank may be forced to pause rate-cutting or reverse course.

Second, if stocks are paying any attention to short-term interest rates, there’s a good chance they have already digested most of the Fed’s expected policy easing. Assuming inflation recedes to the 2% target, the Fed can move to a “neutral” rate, what is generally understood as a range of 0.5 to 1 percentage points above inflation, or 2.5% to 3% on a nominal basis. The two-year Treasury yield, which anticipates the fed funds rate and ultimately tracks it closely, has declined to 3.6% from 5% in April, so it’s already most of the way to the supposed neutral rate. What the bond market knows, the stock market knows, too.

Finally, and most consequently, investors who increase their allocation to stocks will be left with some hard decisions. If they reduce that allocation when the Fed raises rates again, they will have to accept a lower return because, as the historical record shows, stocks usually climb whether the Fed raises or lowers rates. On the other hand, if they maintain their higher allocation to stocks, they will have to live with a riskier portfolio than they presumably wanted before they began fiddling with interest rates.

The only other alternative is enticing but fantasy — that investors will raise and lower their stock allocation at just the right time. It’s improbable because few investors can sell stocks in a rising market. More likely, their portfolio will take a beating during the next bear market, and they will pare back their equity allocation in a panic at exactly the wrong time, undoing whatever incremental gains they may have captured when interest rates declined and possibly netting a loss from the whole misguided adventure.

In other words, contrary to conventional wisdom, there’s no reliable relationship between interest rates and stock prices, so the movement of interest rates can’t be relied on to decide when to buy stocks. The same is true for the relative performance of growth and value.

That doesn’t mean there are no bases on which to make allocation decisions. There’s an inverse relationship, for example, between valuations and expected stock returns, and valuations point to lower-than-average returns ahead. The S&P 500’s forward price-earnings ratio is 32% higher than its historical average since 1990. That’s not necessarily an argument for reducing stock exposure, but it’s a mark against raising it.

As for the Fed, it’s probably best to ignore its interest rate moves when deciding how much to allocate to stocks.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar