The new thing in electricity is datacenters. The new new thing is … coal?

Two companies you’ve probably never heard of have signed a deal that captures a seismic shift on America’s biggest power grid, with implications for household bills, climate change and the artificial intelligence revolution.

Energy Capital Partners LLC, a private equity firm, is buying Lightstone Holdco LLC, a joint venture between Blackstone Inc. and Arclight Capital Partners LLC that owns four power plants in Ohio and Indiana. Three are gas-fired. The other is one of the largest coal-fired plants in the US, the General James M. Gavin facility; briefly famous in 2001 when a prior owner dealt with local residents’ complaints about pollution by buying their town.

ECP isn’t a household name, but it is perhaps the savviest trader of power assets in the US, with one example being its spectacularly well-timed buyout of Calpine Corp. in 2018, swooping in when public markets had tired of the generation sector and with Calpine now worth multiples of what ECP paid. As with Calpine, the majority of the value in the Lightstone deal likely rests on those younger, more flexible gas-fired plants. Still, while we are a decade into mass coal-plant closures in the US, the private equity firm now also appears to see some value in taking on a 50-year-old, 2,700 megawatt coal facility.

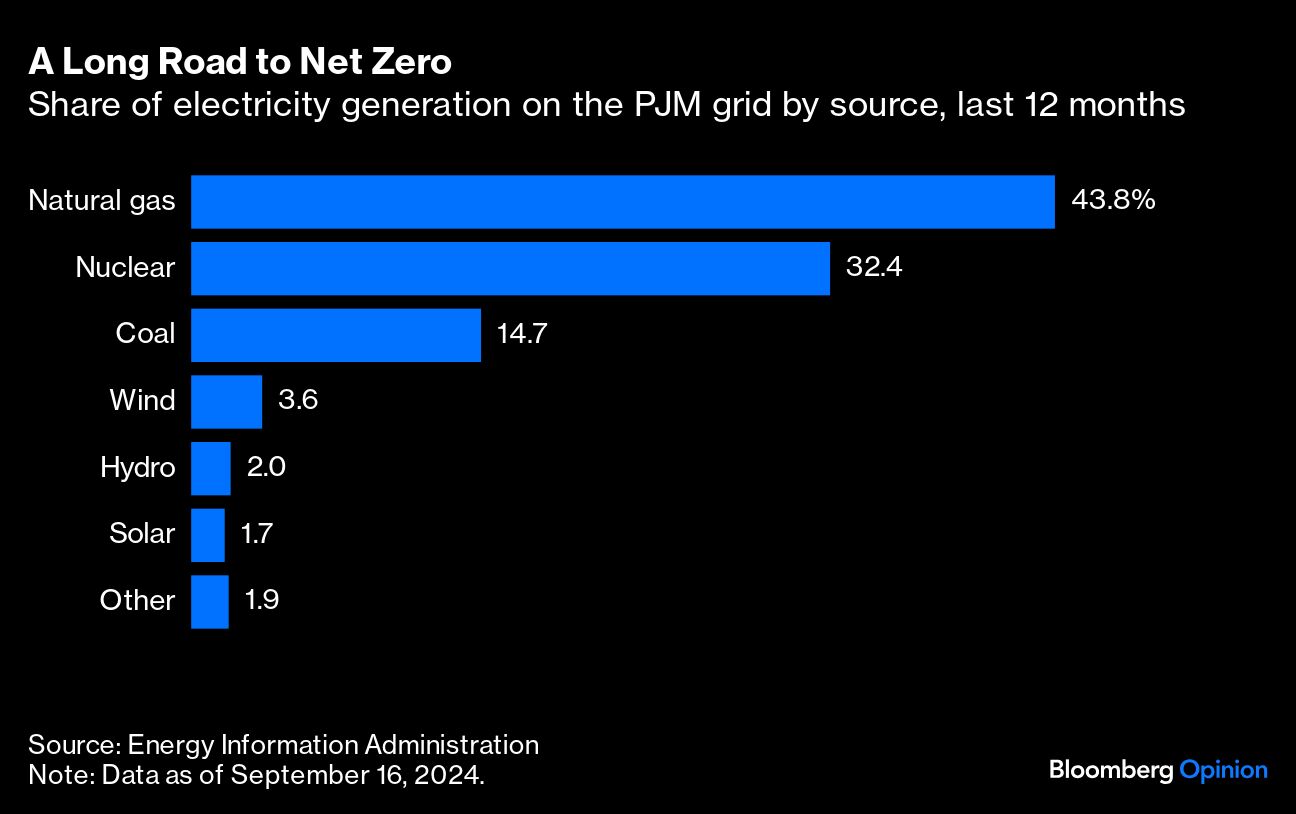

This is the latest surprise in what’s been a year of them for the PJM grid, which covers Ohio, part of Indiana and other states across a swath of the Midwest and mid-Atlantic. In January, the grid operator suddenly tripled its forecast for annual demand growth, centered on proliferating power-hungry datacenters conducting AI operations. Two months later, Amazon.com Inc. announced a deal locking in the output from a nuclear reactor for a co-located datacenter in Pennsylvania. This sparked a frenzy for generator stocks, with Vistra Corp. now second only to AI chip giant Nvidia Corp. on this year’s S&P 500 leaderboard. Then, in late July, PJM’s capacity auction, which sets the amount paid to power plants just to be there if needed, including 30 gigawatts of coal-fired capacity, notched a price increase of 833%.

The Gavin plant’s acquisition would, therefore, reinforce a trend of rising anxiety about the PJM grid and the value of generating capacity rising in tandem. Under conservative assumptions, bidding half the plant’s capacity into the auction would generate payments adding 30% to implied revenue, potentially covering the plant’s entire fixed running costs.1 The deal’s gas plants also benefit from a tightening market.

Hugh Wynne, an analyst with Sector and Sovereign Research LLC, warned some months back that accelerating demand would flip the script on coal plants in PJM.2 Rather than retiring and being replaced with a mix of wind, solar and gas-fired capacity, Wynne says coal plants will stay open — and PJM’s emissions will likely rise through the end of the decade, rather than declining by up to 22% under the old demand forecasts. Separately, Andy DeVries at CreditSights notes that the Gavin plant doesn’t have a scheduled retirement date. While its age and tightening federal regulations — November and the Supreme Court majority notwithstanding — suggest the plant doesn’t have a long life ahead of it, PJM’s new situation will put off the day of reckoning.

This is not a comfortable narrative for Big Tech, which is a big reason why Amazon locked in that nuclear contract. But there are few spare reactors and if it comes to a choice between being first in AI or first in net zero, I suspect the robots win. The priority is to get a grid hook-up as fast as possible. Alphabet Inc.’s Google has already delayed its net-zero targets and Microsoft Corp. is also struggling to balance AI and green ambitions. So-called hyper-scalers are highly unlikely to sign contracts for coal-power, but their rising burden on the grid means they will rely on such plants indirectly anyway.

When electricity prices rise, generators respond, keeping old plants open or building new capacity — that’s what rising prices are supposed to do. The big question concerns how the datacenter operators respond.

PJM’s capacity auction only locks in payments to generators for a few years, enough runway to keep an existing plant open. Encouraging new projects lasting decades requires big buyers such as datacenters to sign long-term supply contracts. In the near term, we can probably expect more bilateral supply deals, including some with gas-fired plants justified on the grounds that they emit less carbon than coal-power and act as backup to renewables. But more than that will be needed, especially as electrification of vehicles and other processes push up demand alongside datacenters and pressure intensifies to make good on net-zero pledges.

Big Tech could try three broad approaches. The first involves efficiency, since the cheapest, cleanest kilowatt-hour is the one you don’t use. The datacenter industry has proven adept at reducing energy consumption in the past, and the twin incentives of rising costs and reputational damage should spur greater efforts. This includes temporarily reducing consumption when power is tight, with the grid operator rewarding such demand management.

The second involves commitments to developers of new zero-carbon supply. That includes renewables, plus batteries, obviously, but those are growing from a low base in PJM and dispatchable generation remains crucial to deal with rising demand.

Might this be when some deep-pocketed tech giant signs a contract with a developer of small modular reactors or gas-plants fitted with carbon capture equipment? There are formidable obstacles of cost, timing and risk (see this and this) — which is precisely why the proponents of such technologies could use the backing of strategically constrained customers such as Big Tech. It is worth mentioning that Calpine is developing carbon capture demonstration projects at gas plants in Texas and California, backed by Department of Energy grants.

The third approach, which isn’t mutually exclusive, is self-help in the form of onsite backup. Datacenters’ need for reliable power, and a recent history of weather-related blackouts or near misses on major US grids, mean any serious operator will incorporate generators and batteries to step in when necessary. Generators tend to run on natural gas or diesel, though, which emit carbon.

On the other hand, having them on-hand to deal with fluctuations in grid supply makes a datacenter operator more comfortable signing contracts for new renewable energy projects. Moreover, if the datacenter boom is real, and lots of backup capacity is installed alongside them, that capacity could also help support the grid broadly, says Wynne. While any datacenter would prioritize its own needs during an actual blackout, it could offer capacity to the grid operator in periods when conditions are tight and extra increments of generation have high value (similar to when peaker plants fire up). In a sense, the datacenters themselves could compete away some of the revenue going to old power plants staying open to deal with their demand growth.

AI’s energy challenge is that its futuristic visions are tethered ultimately to the same old grid we all use and pay for, putting further strain on it and in the midst of climate change. Few things emphasize the acuteness of this dilemma like a new deal for old coal plants.

1 At the latest auction price of $269.92 per megawatt-day, the payment to the Gavin plant if it bid in half its capacity would be $133 million. I assume half (rather than 100% of capacity) because any capacity bid into the auction that subsequently fails to perform gets penalized. The Gavin plant ran 57% of the time in 2023 (source: CreditSights) for output of 13.5 terawatt-hours. Spreading $133 million of capacity payments over that would equate to just under $10 per megawatt-hour. That is about 30% of the average around-the-clock whole electricity price for the PJM West hub in 2023, which was $33.07 per MWh (source: Bloomberg). In addition, assuming a fixed operating cost for a coal plant of $50 per kilowatt-year, the implied cost of simply keeping the Gavin plant running, before generating electricity for sale, is about $135 million, meaning the capacity revenue would more or less cover that expense. These are all purely indicative figures, since I lack detailed information on Gavin's capacity-auction participation and realized prices may differ due to timing of output and hedging.

2 "PJM Hosts More than Half of America’s Data Centers; How Will Their Growth Affect PJM’s Generators?" Eric Selmon and Hugh Wynne, Sector and Sovereign Research, June 3, 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liam Denning