In a niche corner of the bond market, an almost $140 billion wave of maturing debt is poised to lend momentum to what is already one of Wall Street’s hottest hedge fund trades.

About 40% of all dollar-denominated convertible bonds in the world come due by the end of 2026, according to data compiled by Bloomberg, throwing up all manner of opportunity for an arbitrage strategy beloved by fast-money players like AQR Capital Management and Man Group.

The bet is the corporations that issued the debt — notes that can turn into equity if conditions allow — will likely opt to refinance as maturities approach, creating a potential double windfall for opportunistic hedge funds who have snapped up the paper.

First, issuers typically buy back old bonds at a premium of a few percentage points to their trading price, allowing holders to make easy money. Second, companies will often issue new converts simultaneously, giving favorable allocations to existing investors in the process.

“That often does quite well out of the gate, because most converts trade up after a new issue,” said Michael Youngworth, Bank of America’s head of global convertibles and preferred strategy. Refinancing “has been a very lucrative source of alpha for hedge funds this year,” he said.

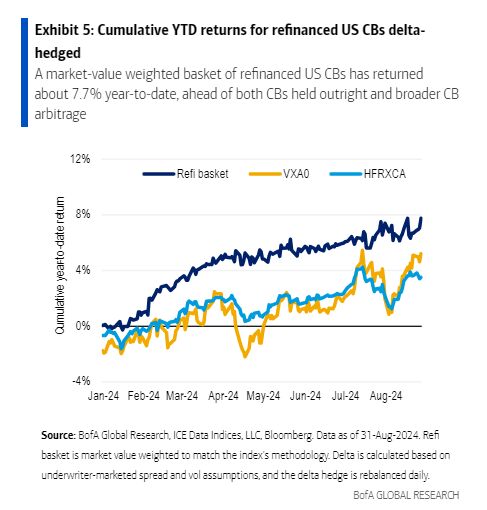

The trade ties in perfectly with broader convertible arbitrage strategies, which typically involve buying the debt and selling the underlying shares short to create a hedged position with upside either way. A Bloomberg index tracking this tactic has gained 8.7% in 2024 so far, compared with 7.8% for a gauge of hedge fund strategies overall.

The wave of maturities stems from an issuance bonanza during the pandemic era, and the market is hot right now because companies typically review refinancing needs one to two years before their debt comes due. Many prefer to control the timing of when they raise new debt, so move early rather than wait to maturity. In some instances, holders of their debt may also push for an early refinance.

The pool for potential arbitrage bets is large as about 70% of existing paper due by the end of 2026 is “out of the money,” according to BofA data. That means the underlying share price is below the conversion level, making the bonds plausible refinancing candidates.

In August, JetBlue Airways Corp. announced the sale of five-year convertible notes worth $400 million to repurchase a portion of its existing paper due 2026. Eventbrite Inc. bought back some some of its notes maturing in 2025. Share prices for both companies were well below the conversion levels of their respective bonds.

To maximize returns from deals like this can require both a high degree of confidence and deep pockets, however. When companies replace convertible bonds, they often do a private placement instead of a public offer. That limits how much of the debt they can buy back and how many holders can participate in the new deal, leaving other investors potentially stuck in an original note that’s just become smaller and less liquid.

“You want to be in the top 10 holders, give or take, to get the call from bankers pitching,” said Eli Pars, co-chief investment officer of Calamos Advisors. In a $500 million bond, that would generally mean owning paper worth tens of millions of dollars.

A Bloomberg analysis shows Marshall Wace, Man Group, Point72 Asset Management, Oaktree Capital, Sculptor Capital and Advent Capital were among the top holders of JetBlue’s 2026 convert as of mid-year, when the price was around 85 cents on the dollar. The paper climbed above 90 cents before the August buyback. All of the firms declined to comment.

The trade comes with other risks. Sometimes a company may leave their existing convertibles outstanding until maturity, creating a potential headache for any manager who borrowed money to finance their position in expectation of a swift exchange.

For instance, despite being seen as a prime refinancing candidate by the investor community, Shift4 Payments Inc. in August opted to issue straight debt instead of a new convertible.

Credit risk is also ever-present — in other words, the chance a debt holder won’t get repaid at all. While there is a specialized cohort targeting convertibles from distressed names, most traders tend to focus on high quality issuers with solid balance sheets and limited repayment risk in refinance trades, according to Erik Mahland, managing director at Glazer Capital.

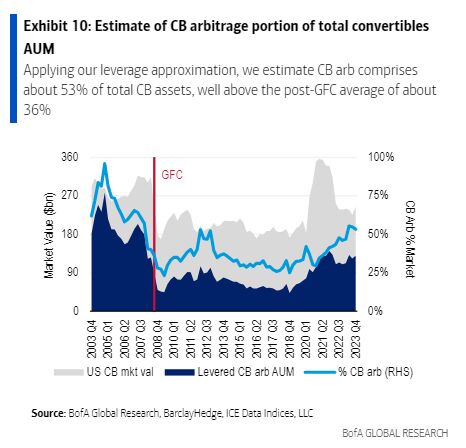

Meanwhile, the influx of fast money means hedge funds now account for about 53% of the ownership mix of convertible bonds while long-only investors make up 47%, according to Youngworth. That’s a reversal of the past 15 years, which saw an exodus of arbitragers after they were crushed during the financial crisis.

Stephane Mantelin, the global head of convertible and derivative arbitrage at Sculptor Capital, says the trade is getting too crowded, with prices of some refinancing candidates surging to levels that don’t make sense.

“We are actively looking for short-dated bonds and potentially good candidates for this trade, but want to be discretionary and opportunistic, not buying every bond,” he said.

Still, the calendar is not the only thing powering the arbitrage trade just now. New issuance is booming, not only because firms are refinancing, but also thanks to new entrants attracted by interest rates generally below that of conventional debt.

The strategy has also benefitted from a slew of corporate events like takeovers and bankruptcies, as well as occasional bouts of market turbulence. These throw up dislocations between company share prices and debt that can be exploited using the hybrid instruments.

“That’s the beauty of convertible arb, there is a diverse set of participants buying and selling convertible bonds for different reasons,” said Mahland. “The variance of these valuation drivers between participants in many cases can result in attractive arbitrage opportunities.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Yiqin Shen