Earlier this year, the Federal Reserve seemed to have time on its side. Payrolls were growing at a healthy clip and the unemployment rate hovered near a five-decade low. Even though there were signs that inflation was licked, there didn’t appear to be much harm in keeping interest rates elevated for a while longer — just in case. Unfortunately, policymakers can no longer take the resilience of the labor market for granted.

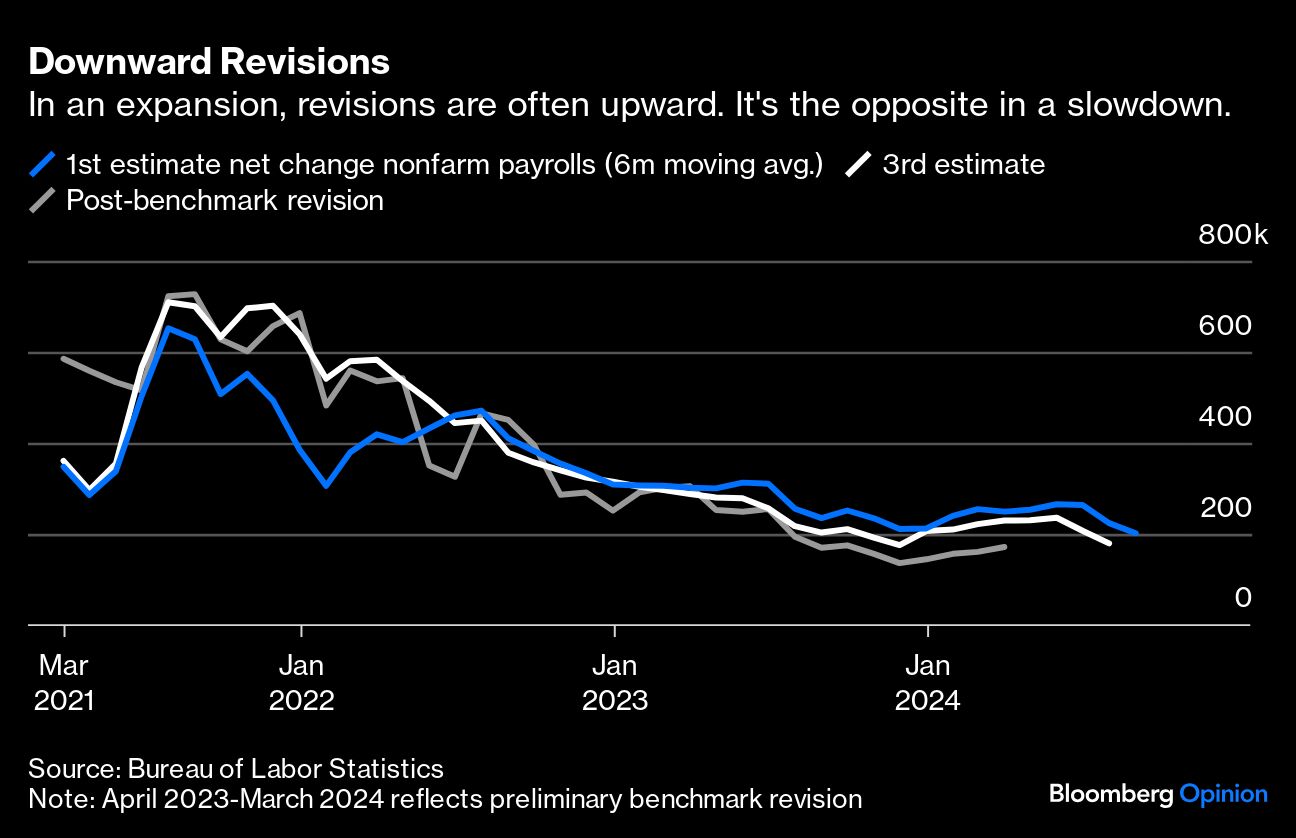

Perhaps the most salient detail in the August payrolls report was the net negative revision of 86,000 jobs in the previous two months’ data. The Bureau of Labor Statistics does the best job it can to deliver timely labor market data to the public, but the first drafts often end up being imperfect. Numbers are revised a couple of times as additional survey responses roll in, and there are further — sometimes larger — revisions during an annual benchmarking process. This means that the monthly data is often foggy, with large margins of error.

That brings us to last week’s news that the US added 142,000 jobs last month, which is quite fine on the face of it. All we can really say with 90% confidence though is that the actual number is somewhere between 7,600 and 276,4000, according to confidence intervals provided by the BLS. That’s a wide range! And history has shown that the revisions can be procyclical: positive in expansions, but often negative in slowdowns and recessions.

The experience of the last several years seems to echo that pattern, especially after you account for still-preliminary benchmark revisions announced last month that are expected to reduce April 2023-March 2024 payrolls gains by 818,000. All in all, a risk-management approach to policymaking demands that the Fed assume that the latest numbers are also somewhat worse than meets the eye.

Fed Governor Christopher Waller said this month that, with the August revision, the three-month average of payrolls numbers is now below the breakeven pace for job creation that holds the unemployment rate steady.

There could be a few reasons why revisions turn negative during downturns. On a month-to-month basis, it may be that struggling businesses are overrepresented among late responders in the Bureau of Labor Statistics’ Current Employment Statistics survey of 119,000 businesses and government agencies. In a perfect world, you might be able to make statistical tweaks to account for such a bias, but you can’t really count on biases to remain stable over time. Meanwhile, survey response rates have been in secular decline for a decade.

What’s more, the US is coming off a historically unique burst of business creation that has strained the BLS’s birth-death model. One of the fundamental challenges of tracking payrolls changes is that there are constantly companies being created and shutting down that aren’t in the survey sample. The birth-death model tries to adjust for that. Yet after the entrepreneurial spurt of the pandemic and post-pandemic years, the model appears now to be overestimating actual job creation as business closures picked up and business creation cooled. That was a significant factor behind the large downward preliminary benchmark revisions last month. Bloomberg Economics estimates that the model is still overestimating this year’s payrolls numbers by around 91,000 a month.

Personally, I’m not ready to conclude that the US labor market is completely out of gas. But if you’re a policymaker focused on risk management, you have to assume a worst-case scenario — that the actual pace of payroll gains is already well below 100,000 and falling. Data from the household survey, jobless claims and the Job Openings and Labor Turnover Survey all generally point to an anemic pace of hiring. Thankfully, there isn’t much firing going on yet.

The key to sustaining the expansion is for the Fed to expeditiously reduce policy rates from currently restrictive levels toward reasonable estimates of “neutral,” where economic activity is neither fueled nor restrained. At a current 5.25%-5.5%, Fed voters have a long way to go to reach even the high end of neutral estimates around 3.75%-4%. Hawks can always find a reason to be concerned about inflation, but it mostly seems to be defeated, and the risks of a resurgence now look modest compared with the risks of further softening in the labor market. Nobody knows for sure where we are in that process, but one thing is clear: Time is not on policymakers’ side.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.