Despite what you may have heard from the doomers, the US labor market is hardly falling apart at the seams. Layoffs are still extraordinarily low and a report Friday showed that the overall unemployment rate slipped to just 4.2%. This is not an economy that’s heading for an imminent recession — far from it. It is, however, a uniquely challenging labor market for recent graduates and other new entrants trying to find their first job. That’s reason enough for the Federal Reserve to start lowering interest rates, perhaps even aggressively.

In his closely watched speech in Jackson Hole, Wyoming, last month, Fed Chair Jerome Powell told the public that he and his colleagues wouldn’t “seek or welcome further cooling in labor market conditions.” Most people took that to mean rising layoffs, which can contribute to a negative feedback loop in economic activity. If people lose their jobs, they’ll curb consumption, and those employed in other parts of the economy may eventually lose their jobs as well. That’s not happening, and we should all take some comfort in that.

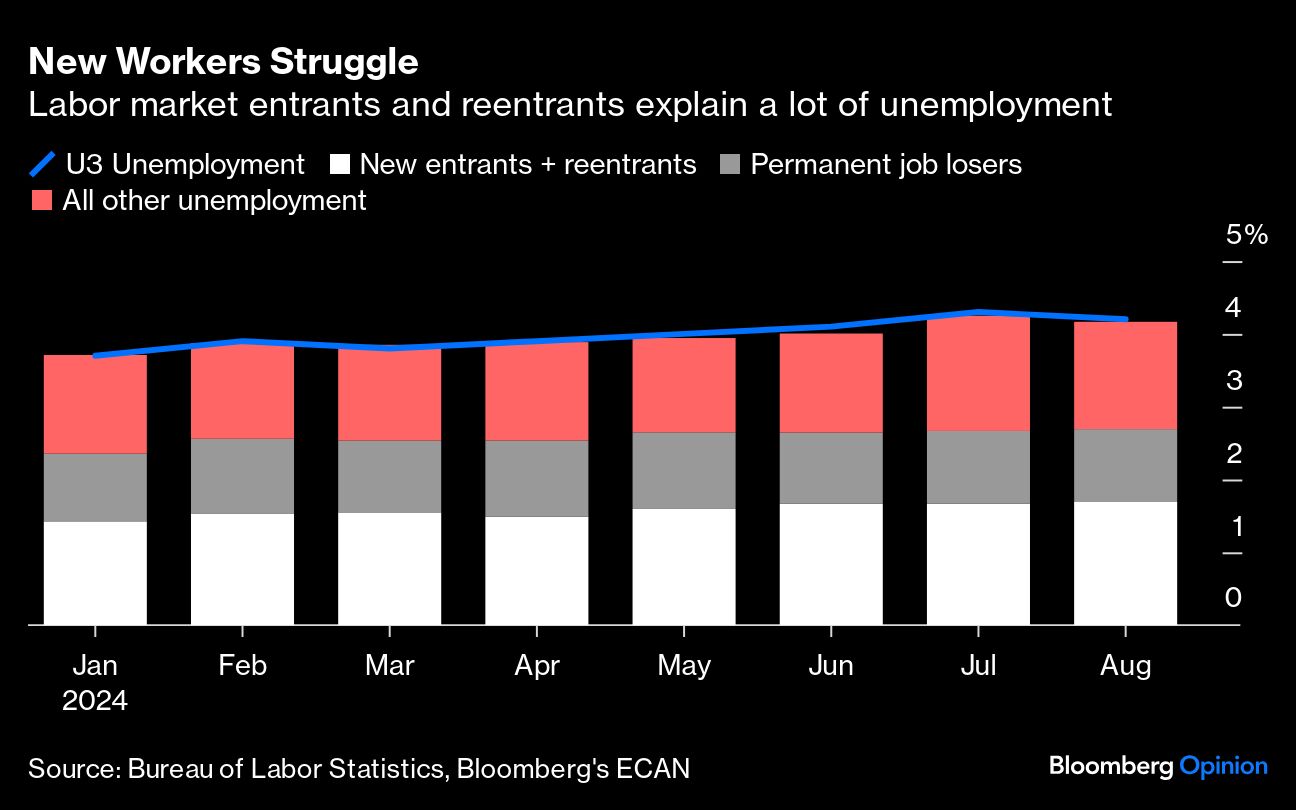

But a labor market can exhibit alarming weakness in other ways as well. In this bizarre post-pandemic economy, companies are adjusting to uncertain times by dramatically cutting hiring, a trend that has continued as the Fed keeps policy rates at a two-decade high. For the most part, unemployment has moved up over the past six months because adults entering the labor force aren’t finding jobs.

About 718,000 new entrants to the labor force (such as high school and college graduates) were unemployed as of August, the most since April 2017. If you add in “reentrants” who have worked before but were recently out of the labor force (such as parents who took time away to focus on kids), the numbers are still well above pre-pandemic norms from 2017-2019. As the overall unemployment rate has climbed to 4.2% from 3.7% at the start of the year, about half of the move has come from entrants and reentrants who don’t immediately find work.

If the Fed doesn’t take meaningful action, odds are that component of unemployment will continue to rise. We see that in the hires rate — the percentage of new hires per 100 employees — which sits at just 3.5%, a level consistent with the frustrating labor market of a decade ago, when the US seemed to be experiencing a “jobless recovery.” We also see it in the swiftly declining numbers of job openings in the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey.

If young people and former stay-at-home parents can’t find jobs, that’s a problem for the entire labor market: It means that companies are light on the skills and perspectives that, for instance, parents and recent graduates bring. It also means that the next generation of managers is getting a slow start to their careers — an issue that could weigh on their savings and the economy years and decades down the road. That’s why Fed policy makers should see the soft labor market for entrants and reentrants as a challenge that demands policy action.

Encouragingly, policymakers are paying attention, with Fed Governor Christopher Waller saying in remarks Friday that “the current batch of data no longer requires patience, it requires action.” He also said that he would advocate for “front-loading rate cuts if that is appropriate,” though it would depend on data flow.

Inflation has been moderating for two years running, and policymakers have plenty of room to reduce rates just to get to a “neutral” policy stance that’s neither restrictive nor stimulative. The challenges facing new workers tell me that they should lean toward “faster” rather than “slower.” That means a 50-basis-point rate reduction at the policy meeting later this month. There’s no point in waiting for layoffs to accelerate to kick rate cuts into high gear when so many willing and ready workers are already struggling.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin