The almost $3 trillion rally in Nvidia Corp. shares over the roughly two years since ChatGPT’s unveiling has virtually rewired the US stock market, giving the artificial intelligence chipmaking giant an outsized influence on a bevy of equity indexes.

Wall Street witnessed that sway during the equities rout earlier this month and the subsequent rebound, in which the S&P 500 Index recovered $4 trillion in market capitalization between Aug. 5 and Aug. 23 as Nvidia’s stock price soared more than 28% in just three weeks. Now, with the company’s earnings scheduled to arrive after the market close Wednesday, traders will be glued to their monitors in preparation for any wild swings.

Going by the options market, Nvidia’s results are expected to send its shares careening nearly 10% in either direction — a move that would shuffle some $300 billion in market cap. And that’s just its own stock. The chipmaker accounts for 6.7% of the S&P 500, making it the second biggest company in the broad equities benchmark after Apple Inc. It also has a more than 8% weighting in the Nasdaq 100, and it makes up 14% of the Philadelphia Semiconductor Index.

“Nvidia is obviously the cleanest sort of pure play way for investors to assess the health of the AI infrastructure space,” said John Belton, portfolio manager at Gabelli Funds. “So Nvidia’s earnings are watched because they have direct read-throughs for so many companies in the AI value chain.”

Seeking Revenue Growth

Sales growth will be the focus on Nvidia’s results after earlier reports from AI darlings like Alphabet Inc. and Amazon.com Inc. showed huge capital outlays producing relatively puny bumps in revenues. For five quarters now, the chipmaker has far outstripped expectations and promised even bigger hauls to come. It has done this by becoming the primary beneficiary of billions in AI spending, so any deviation from that trend would raise questions about the technology’s promise.

That pivotal role has effectively transformed the once obscure semiconductor manufacturer into a key measure of US economic strength.

“It shouldn’t be a bellwether for the economy,” said Shana Sissel, founder and president at Banríon Capital Management. “But it has become one because of the size and the impact of the stock on the overall market.”

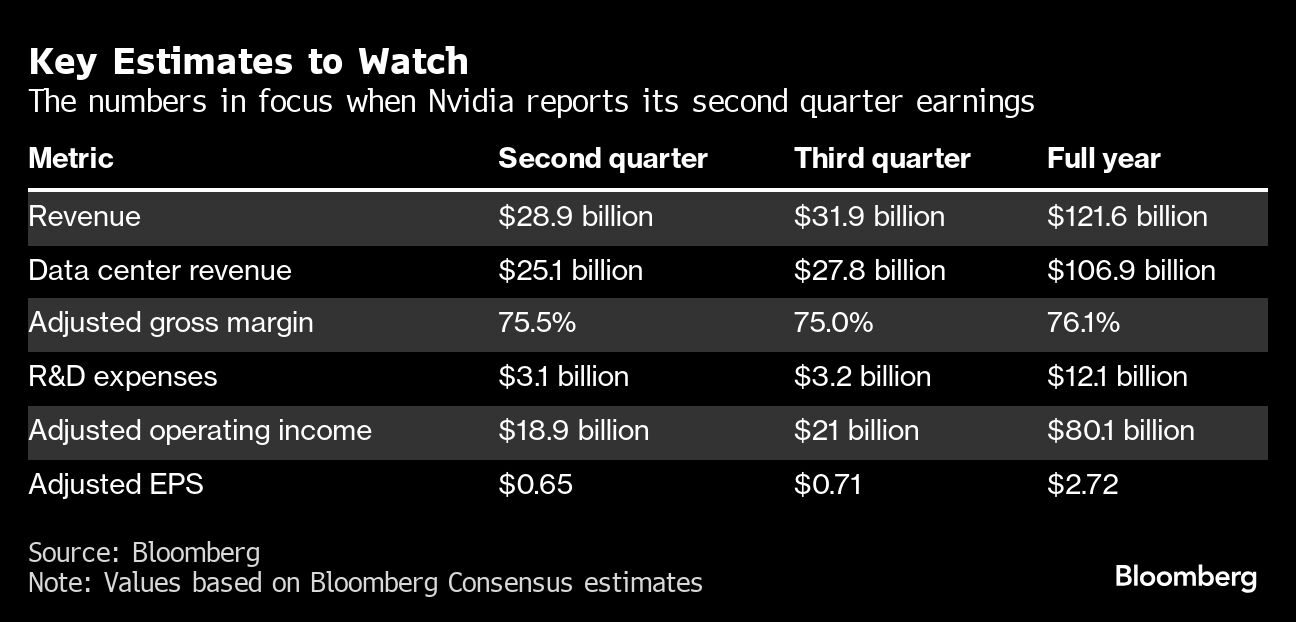

Analysts expect Nvidia’s quarterly revenue to be around $29 billion, more than double what it reported a year ago. And they anticipate another boost in guidance for future sales. But there is one new wrinkle — the company has to give an update on its next-generation Blackwell chip amid reports of delays and design flaws. The company said in early August that production is on track to ramp in the second half of the year.

“Concerns about the Blackwell chip delay could weigh on the upside to expectations for fiscal 2025, making management’s comments — especially a reassuring 2025 outlook — critical,” Bloomberg Intelligence analysts led by Kunjan Sobhani wrote in an Aug. 21 note.

Parsing Commentary

Any commentary about Blackwell on the call is going to be dissected like a Federal Reserve announcement, according to Howard Chan, chief executive officer at Kurv Investment Management.

“Everybody’s going to be mulling over every single word,” he said.

Analysts and investors will also be watching for signs that another Nvidia chip, the H-200, is seeing demand that could offset pushing out revenue from Blackwell. If Nvidia delivers solid results with its current slate of chips, it likely bodes well for the next-generation product.

“It’s probably a good sign if they put up really good numbers here and those are due to strong demand for H-200,” Gabelli’s Belton said. “That probably paints an encouraging picture for incremental demand for Blackwell into next year.”

Of course, Wall Street remains overwhelmingly bullish on shares of Nvidia. The stock has 66 buy ratings, 8 holds and no sells, according to data compiled by Bloomberg. Its 12-month price target of around $145 implies a gain of roughly 13% from where they currently trade. Nvidia’s valuation has also compressed, with the shares trading at a blended forward price-to-earnings ratio of about 38 times, down from 44 times in June and north of 60 times last year. The S&P 500 trades at roughly 21 times its forward earnings.

Concerns about how long heavy spending on AI will continue and worries around the Blackwell chip weighed on the shares in the early August trough. But the rally since shows that investors are still willing to buy dips in the stock as Big Tech’s AI mania shows few signs of stopping — yet.

“The bar has been raised, I think, in the last few quarters,” Belton said. “If you think about what happened with all the megacap stocks throughout this earnings cycle, I think the market definitely wants to see a healthy beat and forward quarter guidance above published estimates. I think this recent run up for near-term trading really matters.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Carmen Reinicke