It’s been the ultimate no-brainer for more than a year: Park your money in super-safe Treasury bills, earn yields of more than 5%, rinse and repeat. Or as billionaire bond investor Jeffrey Gundlach put it last October, “T-bill and chill.”

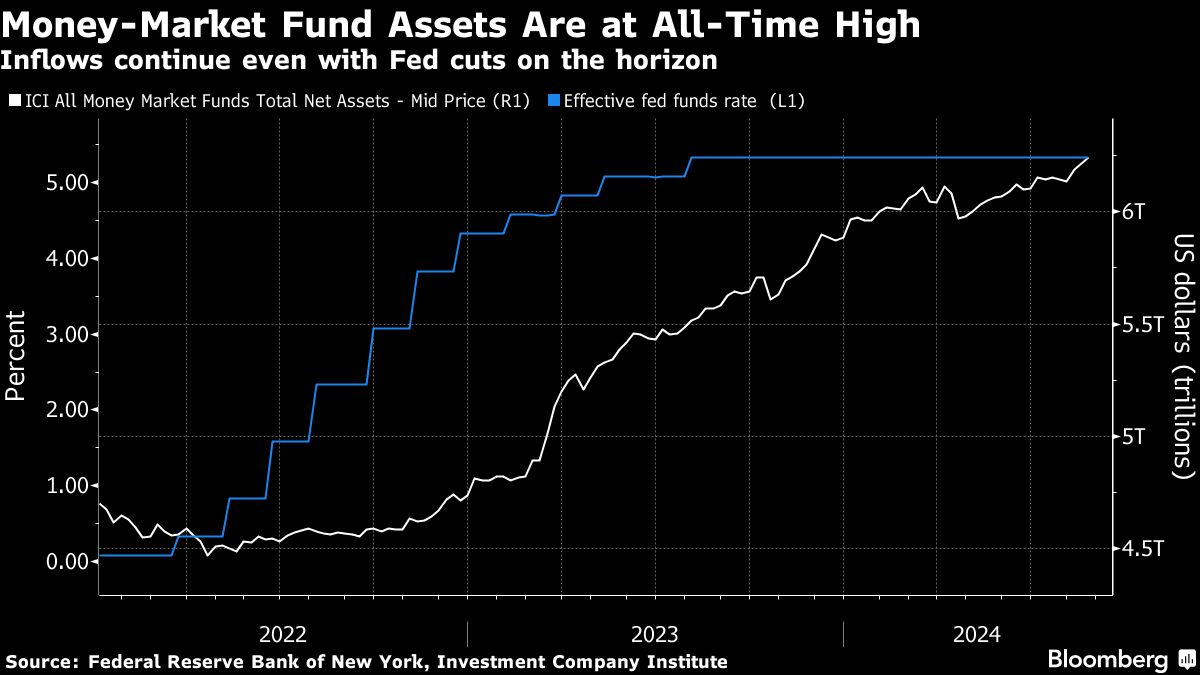

Even now, with Federal Reserve officials poised to ease benchmark interest rates from a two-decade high — a move that would instantly push down yields on bills and other short-term debt — money-market funds are thriving. They raked in $106 billion this month alone and their balances, at $6.24 trillion, have never been higher.

Investors in cash equivalents appear to be perfectly happy to stay where they are for now, despite repeated advice to add exposure to longer-term bonds from the likes of Pimco and BlackRock Inc. — admittedly bond managers themselves. But their point is that while cash returns have nowhere to go but down, debt with longer maturities stands to benefit from capital gains in an environment of deep rate cuts.

“Logically speaking, it doesn’t make a whole lot of sense for $6 trillion-plus to be sitting in money market funds if the yield is going to go down,” Kathy Jones, chief fixed-income strategist at Charles Schwab & Co. “We had a lot of talk about rate cuts and they haven’t happened, so there may be a lot of people who are just actually waiting to see it happen.”

During this year’s bouts of bond volatility, cash has been a good place to be. Money-market rates, which are keyed off of the Fed’s current 5.25%-to-5.5% policy band, have held steady and offered no surprises.

That’s about to change. Fed Chair Jerome Powell signaled last week that rate cuts are coming in September. With inflation ebbing, “the time has come for policy to adjust,” he said, adding that “the direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook and the balance of risks.”

Money markets may continue to appeal, it’s the scope of rate cuts matters. Just 1 percentage point of reductions, for instance, would still leave bill rates in the range of 4%, an appealing return — especially after years of near-zero rates before the most recent tightening cycle, and at a time when longer-term US bonds are yielding far less. This may explain why retail investors are in no hurry to shift their holdings.

“For the first time in recent memory, cash is actually offering some yield and I can understand why people are sort of gravitating to that,” said John Queen, a portfolio manager at Capital Group, which oversees $2.5 trillion in assets. However well that’s worked recently, Queen recommends a classic strategy of diversification, investing in a mix of cash, equities and fixed income.

Of the $6.24 trillion of cash parked in money market funds, roughly 60% of that is from corporations that have been stockpiling cash following the pandemic, while the rest is from mom-and-pop investors who are content to continue earning more yield than what they can earn by merely keeping that money in the bank. Those yields are also significantly higher than what investors can get by moving into longer-term Treasury bonds — though nothing like the stock market’s gains.

Even after the Fed starts lowering borrowing costs, money-market funds should continue to lure at least some cash from retail investors. That’s because they will still offer higher yields than banks and attract institutions that prefer to outsource cash management.

For some investors enjoying high rates on short-term savings, there is a growing recognition that this won’t last forever and they are becoming more attentive to the day when cash returns suddenly drop.

Steven Roge, chief investment officer at R.W. Roge & Co, a private wealth manager with $350 million of assets, says for much of this year the toughest discussions with clients were about teaching them the reinvestment risk of staying too long in a money market fund or high-yield savings account.

“Reinvesting in bond funds over time, that’s been a difficult conversation,” said Roge. “These talks are becoming easier with Fed rate cuts on the horizon.”

The lost opportunity for cash investors is that unlike bills, bonds generate capital gains from price appreciation as interest rates decline.

Bond managers highlight how a 10-year Treasury note yielding less than 4% today has already benefited from capital gains since the benchmark topped 5% less than a year ago. A Bloomberg index of 7 to 10 year Treasuries has gained 13.3% versus a cash return of 4.5% since last October.

Of course, for some the choice isn’t just between bills and longer-term bonds. Warren Buffett’s Berkshire Hathaway Inc. increased its holdings of Treasury bills to $234 billion in the second quarter after cashing in on investments in equities including Apple Inc. For investors like him, holding cash equivalents while rates are still reasonable makes sense until fresh bargains in stocks appear.

But from the perspective of fixed income, the math still works for owning a 10-year Treasury now yielding around 4% versus cash, should the bond market rally towards 3% as the Fed cuts towards a neutral policy setting. Longer-dated Treasuries would enjoy a double-digit return from price appreciation and coupon interest.

“In that scenario, no you’re not better in cash,” said Neil Sutherland, portfolio manager at Schroder Investment Management. “I don’t think it’s unreasonable to think that the 10 year could get down towards 3% and under that environment quite quickly you’re getting up to double-digit returns.”

Digging In

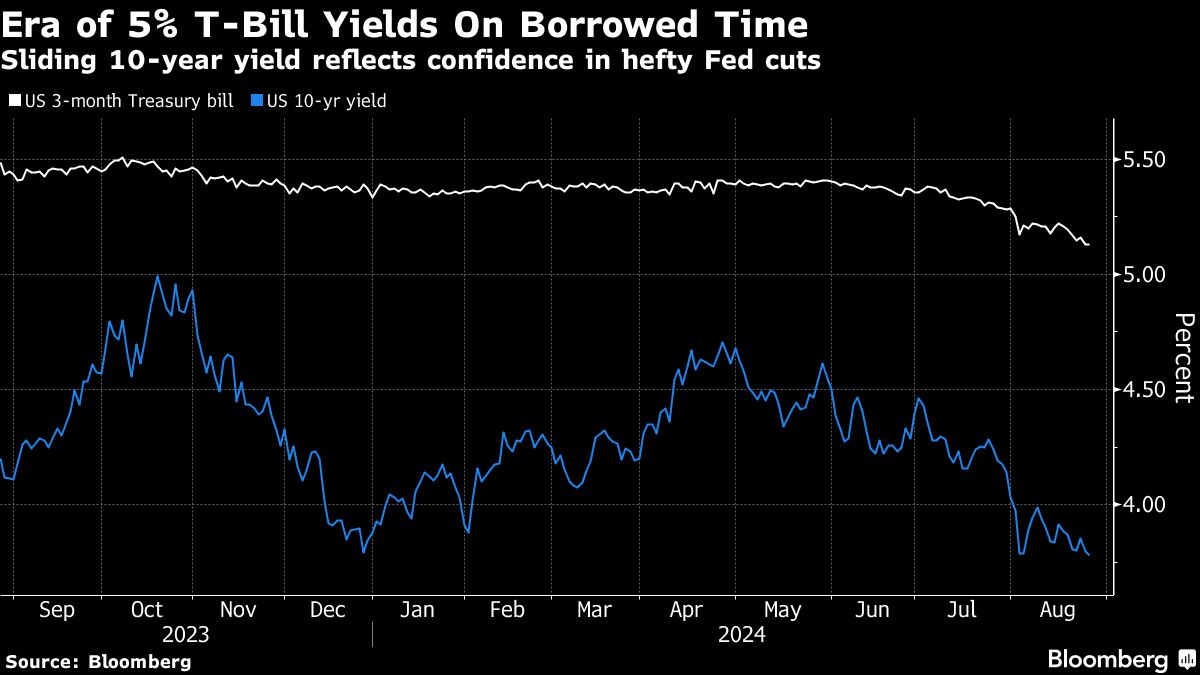

Don’t tell that to Bill Eigen, manager of the $10 billion JPMorgan Strategic Income Opportunities Fund. For him, the idea of moving money into a US 10-year note currently yielding around 3.82% has little appeal. His fund held 54% in cash at the end of July, according to the latest filing.

“You can get mid-5% in cash, get 6% in short-term investment grade floating rate,” Eigen said. “I won’t lend to the government for 10 years and get paid less.”

Eigen has been hoarding cash for a while, a move that has helped the fund return 9% over the past three years, compared with a loss of 6% in the Bloomberg Agg Index. But that was then.

As cash-equivalent rates start moving down — and by all estimates they will — “T-bill and chill” won’t be such a no-brainer anymore.

“Once investors look at what they’re getting, they’ll decide where they are isn’t that attractive anymore,” said Schwab’s Jones.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Michael Mackenzie, Ye Xie, Alexandra Harris