Countries Risk Overestimating Debt Capacity, Jackson Hole Paper Shows

Governments in the US and other developed countries, thanks to their central banks, may be deluded over how much debt they can pile up without significantly raising their costs to borrow.

In a paper presented Friday at the Federal Reserve’s annual gathering in Jackson Hole, Wyoming, economists argued that central bank asset purchases, used in recent years to calm dysfunctional markets and spur growth alongside government stimulus, have muted the impact on bond prices of deficit spending.

“It is not inconceivable that governments in some mature economies have overestimated their true fiscal capacity as a result of these large-scale asset purchases,” the authors, Roberto Gomez Cram, Howard Kung and Hanno Lustig wrote.

The trio describe an environment known as a risky debt, or fiscal dominance, regime. Under this scenario, governments — in an attempt to insure taxpayers against spending shocks — issue large amounts of debt unfunded by taxes.

This ultimately forces bondholders to reprice the cost of securities, which may result in large yield changes in the markets, the authors said. By comparison, monetary dominance, or a safe debt regime, insures bondholders through a government’s commitment to pay for surprise spending with future taxation.

“Large-scale asset purchases by central banks in response to a large government spending increase have undesirable public finance implications,” the economists said, noting that such a program subsidizes bondholders at the expense of taxpayers. “These purchases may also distort the incentives of governments and impair price discovery in government bond markets.”

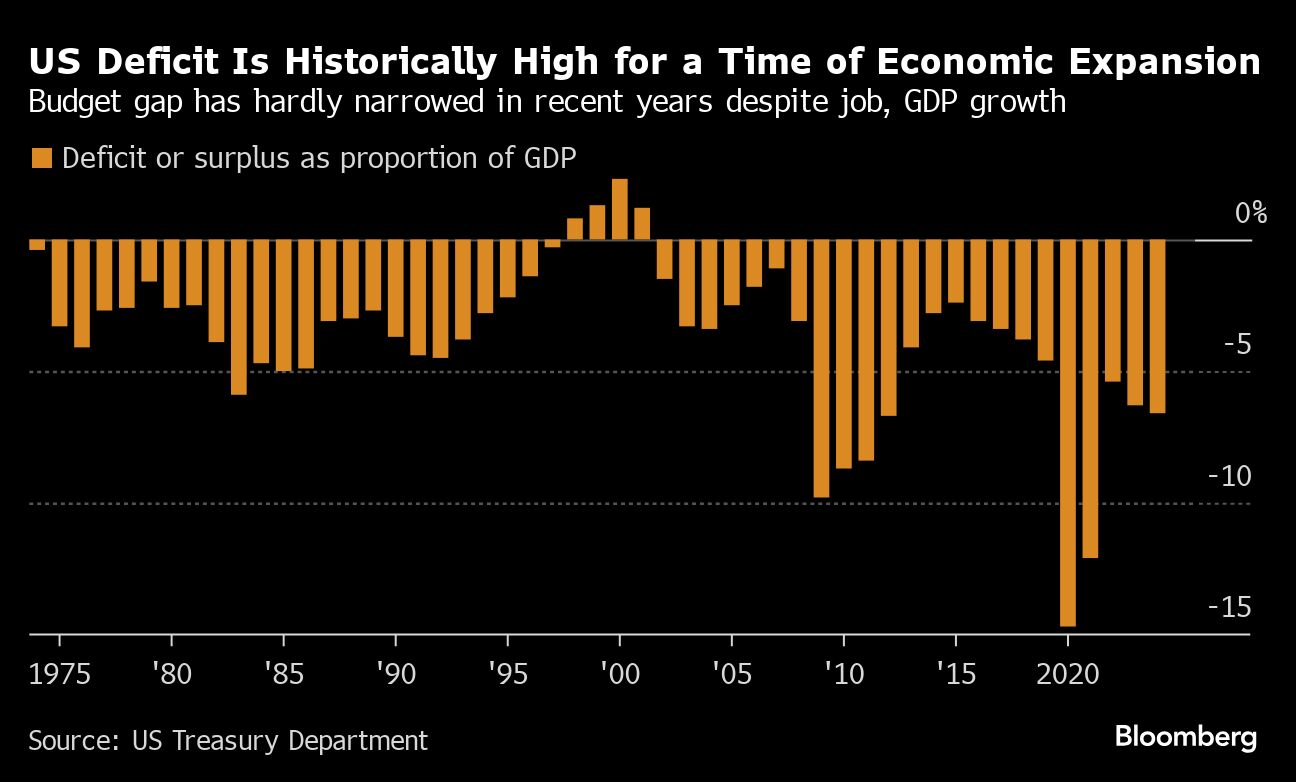

Concerns about fiscal dominance in the US have swelled in the wake of the Covid-19 pandemic, when government borrowing skyrocketed to support the economy. During that time, the Fed’s balance sheet more than doubled to almost $9 trillion as the central bank bought Treasuries and mortgage-backed securities, first to support market functioning and then to stimulate the economy.

Yet now, with total debt outstanding around $35 trillion and the Congressional Budget Office estimating another $20 trillion worth of borrowing over the next decade, some economists are worried the growing debt will prevent the central bank from holding down inflation.

Other notable takeaways:

- During the pandemic, US Treasury yield increases were concentrated on days with significant fiscal news, either in releases of CBO cost estimates for large bills or in Bloomberg News articles — the footprint of a risky debt regime.

- In March 2020, foreign investors sold long-dated Treasuries in a flight from maturity, which the authors described as a time when US debt wasn’t trading as the world’s safest asset, but like sovereign bonds issued by other mature economies.

- Policymakers, including central banks, should “internalize this shift” to fiscal dominance when assessing whether bond markets are functioning properly.

- Before Covid the US hadn’t seen large responses to fiscal shocks in the Treasury market, including during the 2008 financial crisis.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.