One of the most widely followed gauges of the stock market, for decades a reliable indicator of future returns, has led investors astray in recent years. Its misdirection comes down to the freakish earnings growth of big technology companies such as Apple Inc. and Alphabet Inc. But there’s a way to revamp this market barometer as worries about elevated expectations and prices grow.

I’m referring to the cyclically adjusted price-earnings ratio, affectionately known as the CAPE ratio. The CAPE attempts to answer a basic question: When investors buy a stock, they are essentially buying a stake in a company’s earnings, so how much are they paying for those earnings? The CAPE normally applies that question to a broad tracker, such as the S&P 500 Index, by calculating the ratio of the index’s price to a 10-year trailing average of its earnings per share after inflation.

So, for example, the S&P 500 closed at 5,319 last Thursday, and its 10-year trailing average earnings are $168 a share after inflation, according to Bloomberg data, which amounts to a CAPE of 32 times. That’s high — nearly double the long-term average since 1881 and the third highest ever, exceeded only at the height of the internet bubble in the late 1990s and earlier this decade.

To CAPE connoisseurs, it’s a worrisome signal of disappointing stock returns ahead because historically, a high CAPE is strongly correlated with lower future returns, and vice versa. But the CAPE has averaged a stubbornly high 28 times since 2010 — near its current level and well above its long-term average of 17 — and yet, the S&P 500 has ground higher. The index returned 13.8% a year through July, including dividends, one of the best 15-year periods on record. Investors who lightened up on stocks in fear of a high CAPE made a costly mistake.

To understand what went wrong, it helps to know why the CAPE worked in the first place. The idea behind price-earnings ratios is that the less investors pay for earnings, the higher the payoff. But profits can be volatile, and if they are not handled with care, P/E ratios can end up behaving exactly opposite to what investors intend.

During economic booms, earnings tend to grow faster than usual, resulting in temporarily high earnings and therefore low P/E ratios. Inversely, earnings tend to collapse during busts, causing P/E ratios to spike. As a result, using current earnings to calculate P/E ratios would signal to investors that stocks are cheap at the height of booms and pricey in the depths of busts. We saw this backwards signaling play out in the run-up to and following the 2008 financial crisis. Substituting with analysts’ forward 12-month earnings estimates wouldn’t help much since they tend to lean on recent results.

Enter the CAPE ratio, which uses a 10-year trailing average of earnings to smooth the ups and downs of the boom-bust cycle. The result is lower earnings and higher P/E ratios when profits are rising during booms and higher earnings and lower P/E ratios when profits collapse during busts — directionally the signal investors want.

During the financial crisis, the CAPE climbed to 28 times at the top of the market in 2007 because 10-year trailing average earnings were a third lower than current earnings. It dipped to 13 times during the 2009 market bottom, this time because 10-year earnings were more than seven times current earnings. Investors who used the CAPE to navigate the crisis were directionally right both times. Problem solved.

The CAPE’s strength, however, can also be a weakness. It implicitly assumes that boom-bust cycles play out every decade or so. But if the cycle takes substantially longer, using a multiyear average of earnings can be misleading.

That’s essentially what has happened since the financial crisis. Aside from a short-lived earnings setback during the Covid pandemic, the US has not experienced an earnings recession in 15 years. And while the earnings boom continues, current earnings will remain meaningfully higher than the multiyear trailing average, resulting in an elevated CAPE even as the market rises alongside profits. The CAPE’s trailing average earnings of $168 a share for the S&P 500 is well short of the index’s most recent full-year operating earnings of $228 a share.

The gap is likely to narrow during the next earnings bust, but it may take longer than investors expect. That’s because some companies are less vulnerable than others, and the heartiest ones have taken over broad market indexes. The S&P 500 is now dominated by a handful of big tech companies with unusually consistent earnings: Apple, Microsoft Corp., Amazon.com Inc., Alphabet, Meta Platforms Inc. and perhaps to a lesser extent Nvidia Corp. together account for nearly a third of the index, providing a strong counterweight to smaller companies with more volatile results.

Even if the growth of big tech slows, as I expect, it may take several years for its weighting in the S&P 500 to shrink. In the meantime, these companies are likely to keep churning out profits. That may help forestall an earnings recession for the broad market that is severe enough to bring current earnings back in line with their trailing average — a realignment that typically topples the market and vindicates the CAPE.

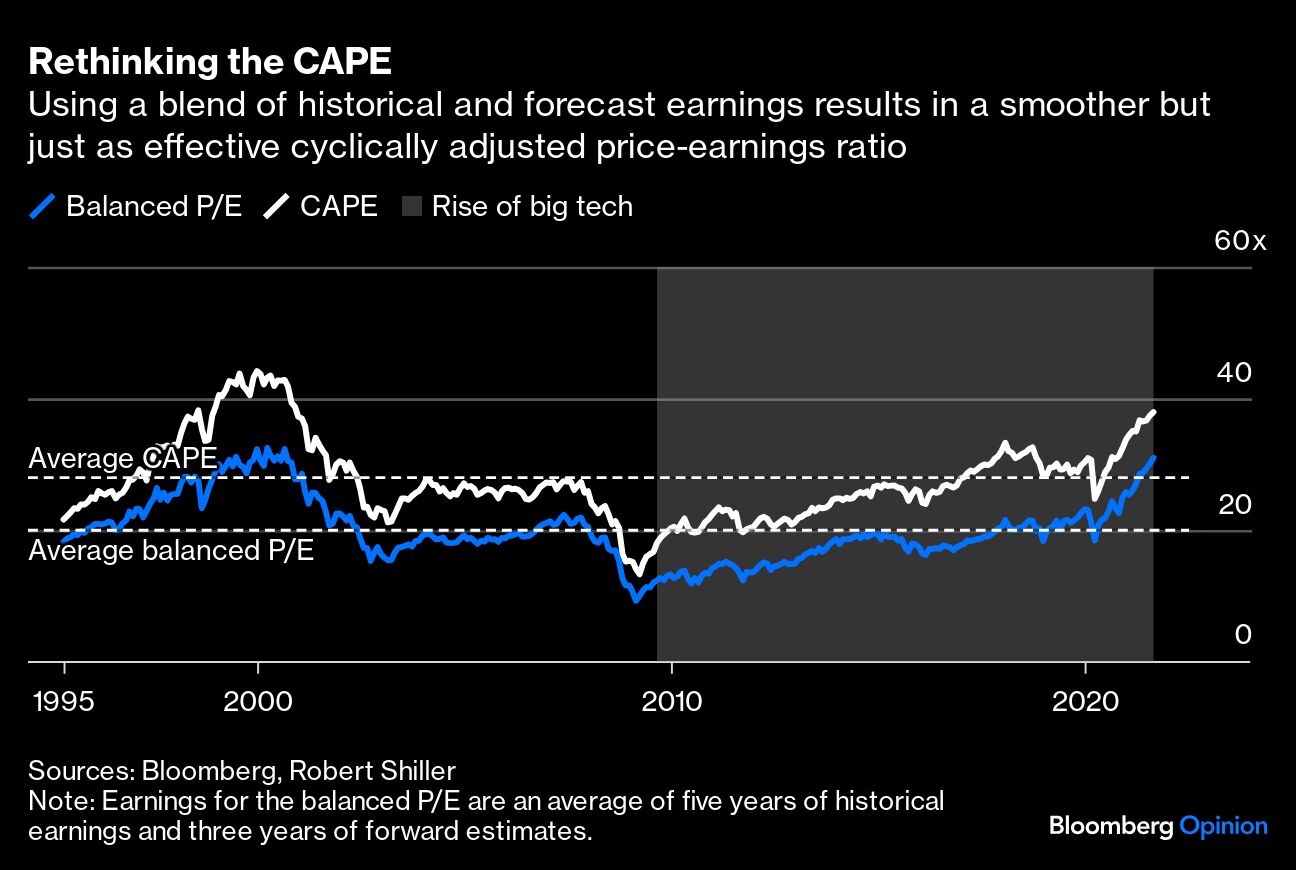

But there’s a way to modify the CAPE that preserves its best qualities and gives investors a hedge against extended booms. Rather than using a 10-year trailing average of earnings, investors could substitute an eight-year average consisting of five years of historical earnings and three years of forward estimates.

This barbell approach will smooth earnings but is less anchored to the distant past. I’m not adjusting for inflation because the historical earnings are more recent, and using three years of forward estimates seems reasonable because it’s harder to see further out.

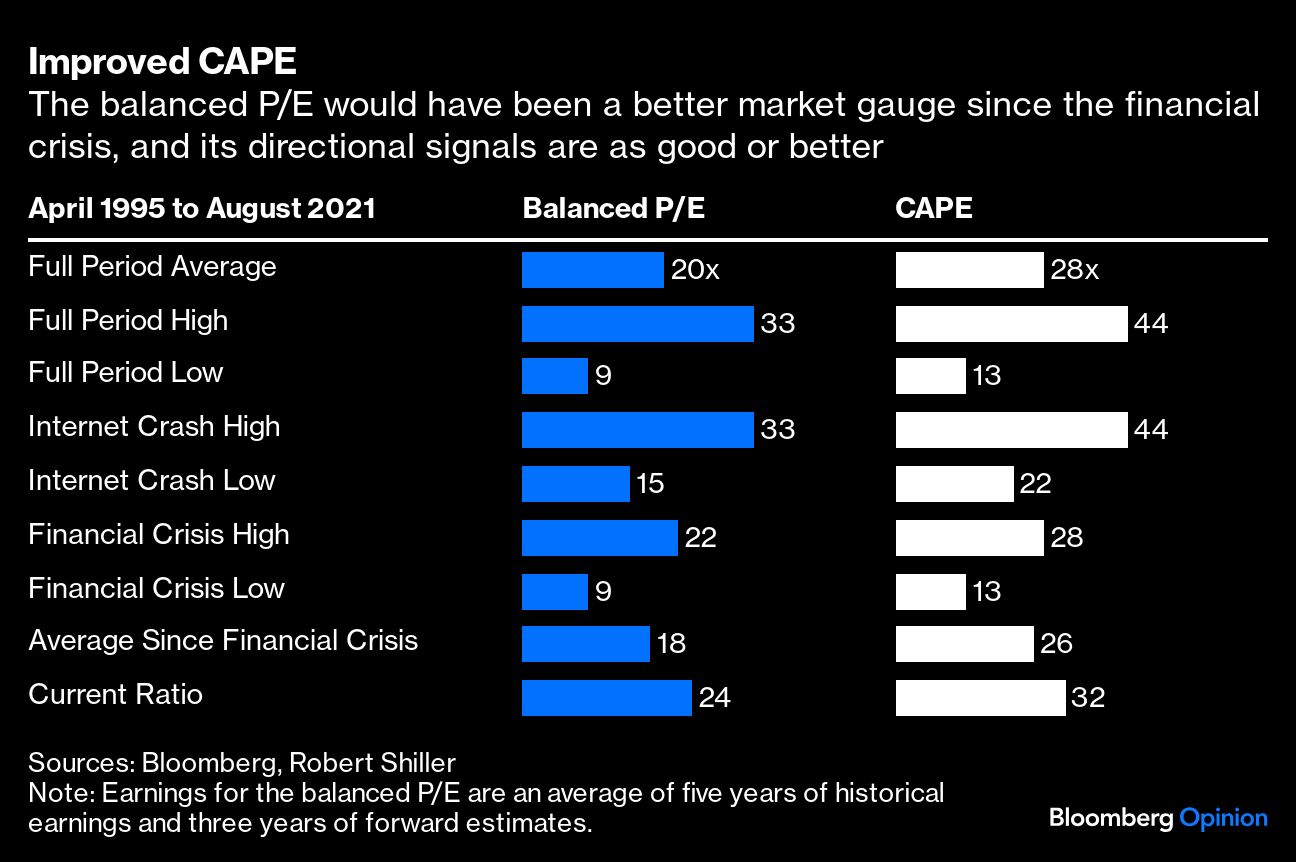

The resulting ratio — let’s call it balanced P/E — provides the same directional signals as the CAPE but better reflects companies’ current financial results, removing some of the extreme CAPE valuations that can arise during earnings booms. Bloomberg has analyst estimates for S&P 500 earnings back to 1990, so I compared the CAPE with my balanced P/E from 1995 to 2021, a test period that includes two epic swells and swoons in the internet crash and the financial crisis.

The average balanced P/E was substantially lower than that of the CAPE, and so was its variability, which means it was less noisy. Still, the balanced P/E’s directional signal was just as good, and in some cases better. During both the internet crash and financial crisis, it was higher than average going in and below average coming out, which wasn’t always true for the CAPE.

The biggest difference is that the balanced P/E would have been a better guide since the financial crisis, averaging 18 times through 2021, as opposed to a more alarming 26 times for the CAPE.

But even the balanced P/E now looks stretched. Its earnings of $221 a share is only modestly lower than the S&P 500’s most recent full-year operating earnings. Yet the market trades at 24 times that, 20% higher than the average balanced P/E during my test period. So, even without an earnings recession, there’s room for valuations to contract.

The CAPE will be right eventually. But the lesson of the past 15 years is that it shouldn’t be the only — and may not even be the best — guide for investors.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar