More than any of the megacap technology stocks, Amazon.com Inc.’s big spending ways are coming at the expense of profits, and its shares are being punished as a result.

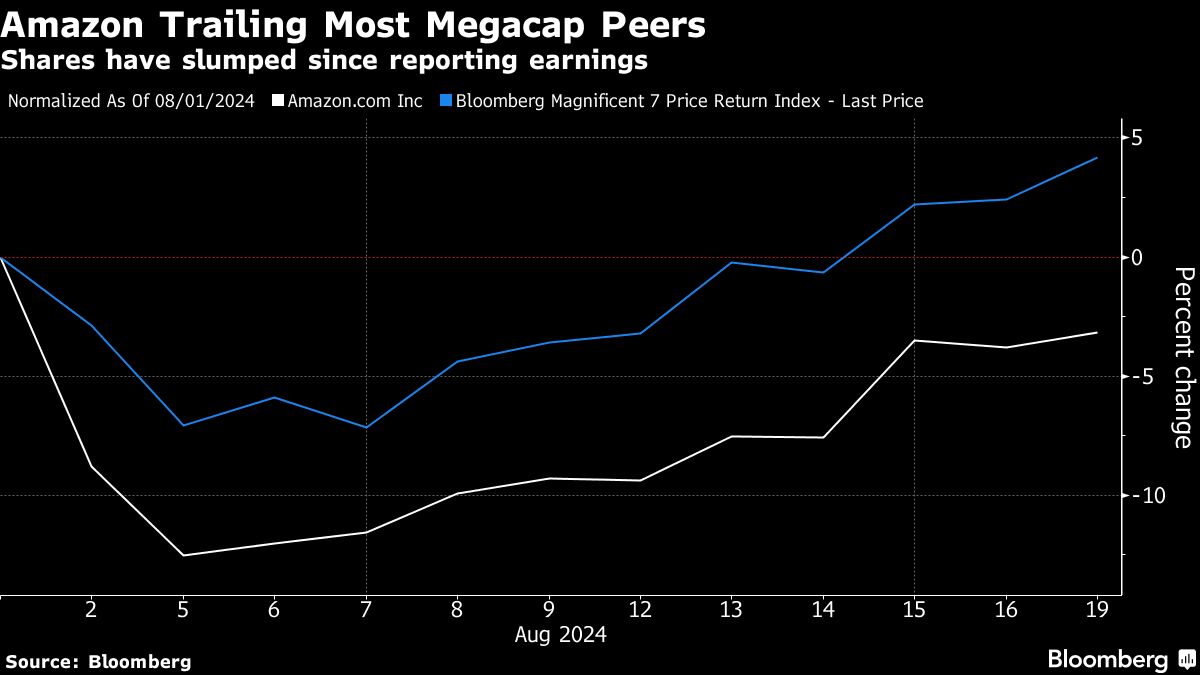

Amazon’s stock performance has lagged its megacap peers since its earnings report at the beginning of August, when the e-commerce giant signaled to investors that it would be prioritizing spending on artificial intelligence computing. The move is a shift back into investment mode after a period of cost cutting that led to a surge in profits and helped fuel a rally that’s seen the shares more than double from a late 2022 low.

“Investors are worried that the increase in capital spending will impact cash flows,” said James Abate, chief investment officer at Centre Asset Management LLC. Amazon shares tend to outperform when it’s focused on improving profitability, compared with when it’s boosting investments, Abate said.

The switch back to spending mode “has investors recognizing that the significant period of outperformance for the stock may be at least on pause if not over for a period of time,” Abate added. Amazon shares remain more than 3% below where they traded prior to the results, compared with a gain of about 4% for the Bloomberg Magnificent Seven Index over that span.

The worry that increased spending will crimp profitability is top-of-mind for investors, given that margin expansion was among key trends that lifted Amazon shares during a run of more than 30% to a peak in early July. Daniel Kurnos at Benchmark sees that positive momentum now potentially at risk.

“A confluence of particular timing of events could conspire to put incremental downward pressure on margins for the next couple of quarters,” according to Kurnos. This could also put a “sharper focus back on the top line at a time when the macro appears to be unstable at best,” he wrote in an Aug. 2 note.

The “macro” affects Amazon differently to its megacap tech peers because of the company’s mix of offerings. The combination of retail, video streaming and film and television businesses sets it apart and also brings varying exposure to developments in the broader economy. While the AWS cloud unit remains a bright spot, a weaker US consumer could drag on retail.

“It seems like investors are waiting on the sidelines to get more information on the consumer,” said David Wagner, portfolio manager at Aptus Capital Advisors LLC. “That’s probably why it’s lagged relative to some of the other peers.”

Investors may also be growing weary of Amazon’s rising cash pile and history of not returning it to shareholders. The company is one of the only megacap technology firms that doesn’t have a dividend. It has also been much less generous than its big tech cohort when it comes to buybacks.

While the rest of its peers have approved tens to hundreds of billions of dollars in repurchases, Amazon’s $10 billion buyback program, which it approved in 2022, was less than half complete at the end of June. The company didn’t complete any share repurchases in the last quarter.

Pressure to compete for investor capital may be even higher for Amazon now that Meta Platforms Inc., Alphabet Inc. and Booking Holdings Inc. have all added dividends on top of their buybacks, Morgan Stanley analysts led by Brian Nowak wrote in an Aug. 18 note.

That leaves Amazon alongside only Tesla Inc. among tech megacaps without “an impactful capital return policy,” Nowak wrote. “If nothing changes by year end ‘25 we estimate AMZN’s net cash balance will make up ~8% of its total market cap.” That would rank it second-highest among the top-25 S&P 500 companies by market value, he added. “In our view a sustained capital return policy would likely lead to a higher multiple on AMZN’s cash flow.”

Still, there are signs investors are stepping back into beaten-down technology shares, buying the dip in Amazon as well as Nvidia Corp., Microsoft Corp. and Apple Inc. Amazon’s stock is up about 11% from the most recent trough on Aug. 5.

The latest downturn in its shares took Amazon’s valuation to about 28 times forward earnings, a discount to most of the so-called Magnificent Seven — only Alphabet has a lower multiple. It’s also at only a slight premium to the Nasdaq 100 index, which trades at about 26 times future earnings.

“People have muscle memory and the winning trade for most people has been to use any dip in the Magnificent Seven as a buying opportunity,” said Abate. “And, you know, until that doesn’t work anymore, people are gonna continue to do it.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Carmen Reinicke