Warren Buffett’s longtime business partner Charlie Munger brought quality to value investing. Now Buffett is bringing value to quality investing.

At Berkshire Hathaway Inc.’s annual meeting in May, Buffett revealed that he had trimmed his stake in Apple Inc., inarguably one of the best businesses in the world. Buffett reassured the Berkshire faithful that he is no less enthusiastic about the company, calling the iPhone one of the greatest products of all time and Apple an even more wonderful business than American Express Co. and Coca Cola Co., two prominent investments in Berkshire’s portfolio.

That turned out to be just the beginning. Earlier this month, Berkshire announced that it had sold nearly half its position in Apple, presumably not because the iPhone maker became any less wonderful in the intervening three months. Buffett hinted in May that tax planning was behind the sale. Some observers have speculated that Buffett is simply trimming Apple’s outsize position in Berkshire’s portfolio.

I suspect there’s another, more important, reason: Apple has become too expensive.

When Buffett began his career, he was a deep value investor, buying, in Munger’s words, fair businesses at wonderful prices. In the 1960s, Munger persuaded Buffett to flip the formula and buy wonderful businesses at fair prices. Investors have started to embrace the strategy of putting quality before value. I counted 115 stock mutual funds and exchange-traded funds with quality in their name. The vast majority are less than 10 years old, but investors have poured in $141 billion so far and that number is growing.

In essence, quality looks for companies that are highly profitable, churn out reliable earnings and have little debt, or some combination of those attributes. Valuation is less important. In fact, the biggest quality funds track indexes that look for high-quality companies with little or no regard for valuation.

The strategy has a lot of data to recommend it. Shares of the most profitable 30% of US companies, sorted by return on equity and weighted by market value, have outpaced the least profitable 30% by 4.1 percentage points a year since 1963 through June, including dividends, according to data compiled by Tuck School of Business Professor Ken French. They also won 92% of the time over rolling 10-year periods. So, on a relative basis, quality stocks won most of the time regardless of valuation.

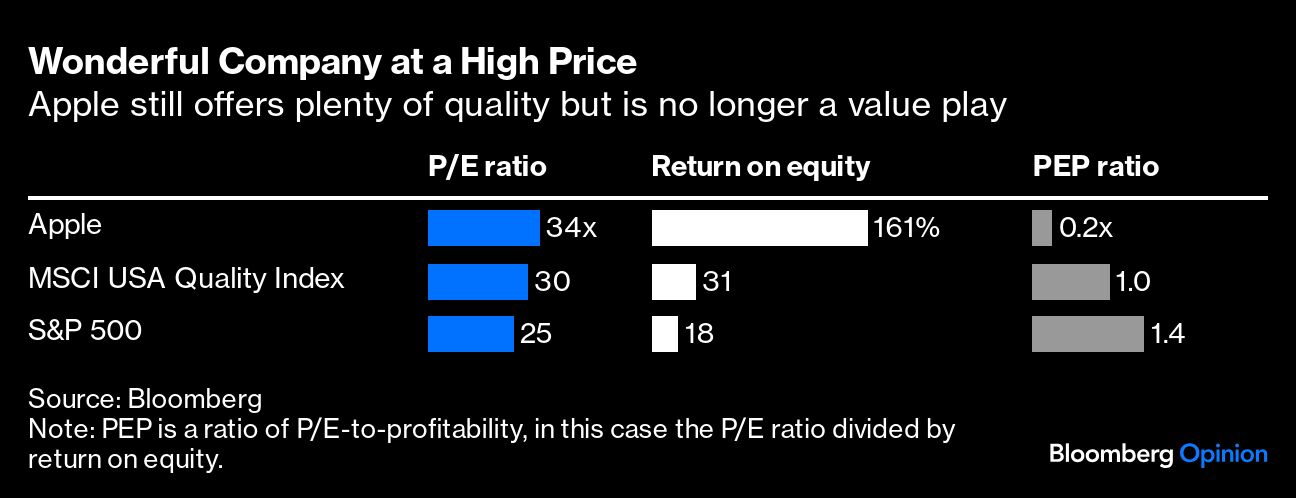

On an absolute basis, however, valuation was more important. The most profitable stocks in the data are further split based on price-to-book ratio. The weighted average P/B ratio of the cheaper group doesn’t vary much and appears to have no impact on future returns (monthly correlation of -0.08 with forward 10-year total returns). The P/B ratio of the pricier group, on the other hand, varies wildly and is strongly negatively correlated with subsequent 10-year returns (-0.67), meaning that a higher ratio was most often followed by a lower return, and vice versa.

When it comes to high-quality stocks, in other words, the more investors pay, the less they should expect to earn. Or, in Munger’s parlance, buy wonderful companies but watch that price closely. Which brings us back to Buffett. When he started buying Apple in 2016, it wasn’t just a wonderful company at a fair price — it was a steal. I prefer price-earnings ratios to P/B ratios when valuing technology companies because they generally own fewer assets than, say, banks or manufacturers, which can make their P/B ratios seem chronically high by comparison.