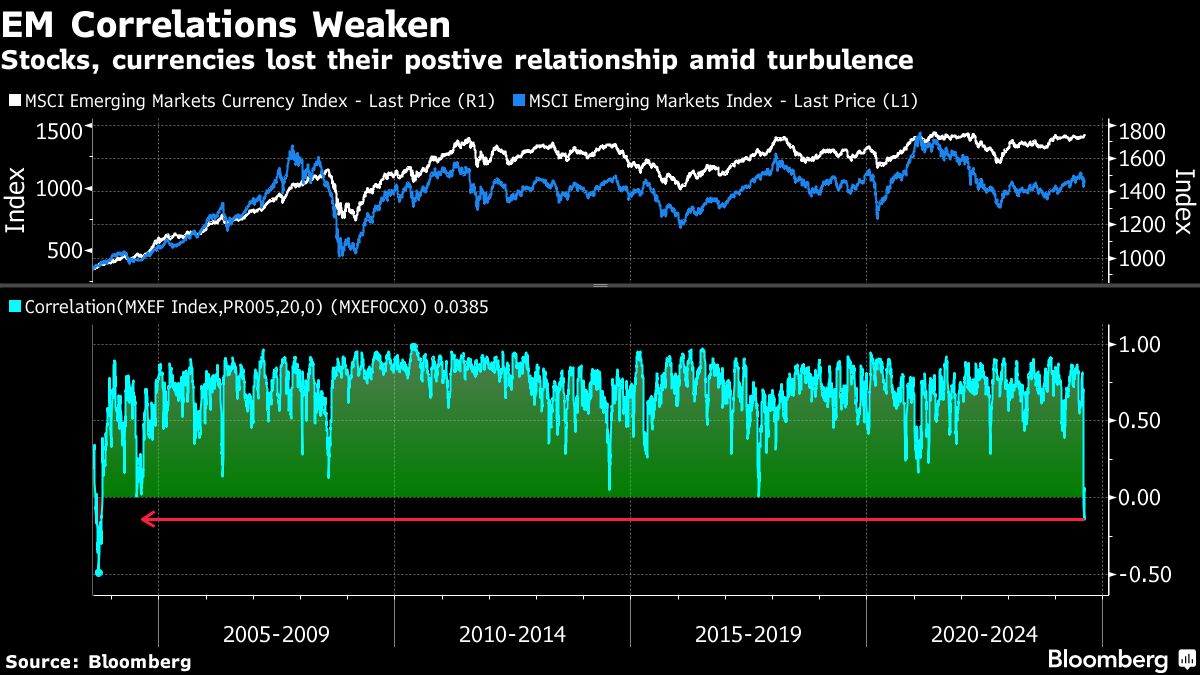

The benchmark indexes for emerging-market equities and currencies, respectively, moved in opposite directions Monday, deepening a trend that emerged last week, when their short-term correlation was interrupted for the first time in 21 years.

The MSCI Emerging Markets Index for stocks rose for the fourth time in five days, while its currency counterpart fell from a 28-month high as of 9:10 a.m. in London. The 20-day correlation between them hovered near zero after turning negative for the first time since 2003 on Thursday. A longer-term measure of their relationship, the 120-day correlation, was near the lowest level since early 2018.

Weakening correlations suggest investors see differing outlooks for emerging-market stocks and currencies. With the Federal Reserve seen starting its monetary easing next month, money managers are weighing the capacity of EM central banks to cut interest rates to boost growth, though EM currencies may gain from a higher rates spread with the US. EM stocks could benefit from increased risk appetite that lower US borrowing costs often bring, but conversely may also struggle with lower economic growth.

Last week’s unwinding of the yen carry trade led to a weaker dollar index, “but an overall weakening eqiuty market selloff,” said Rajat Agarwal, Asia equity strategist at Societe Generale SA. “Now, we are starting to see some strength in the dollar coming back but stock markets are stabilizing faster given the sharp selloff.” He said he expected the traditional correlation to return “when re revert to more normal market conditions.”

The EM stocks index rose 0.4% on Monday, led by Taiwan Semiconductor Manufacturing Co. and Tencent Holdings Ltd., as Asian technology shares extended a recovery. Chinese mainland stocks were little changed, but overseas investors turned net sellers of Chinese stocks for the year after they shed 7.8 billion yuan ($1.1 billion) worth of shares on Friday. If the trend continues, China could see its first annual outflow since at least 2016.

Meanwhile, Chinese shares connected to Covid drugmakers and test makers rallied amid a report that the Guangdong province has witnessed a rise in new infections.

But the bigger markets action in China was in 10-year yuan bonds, with the benchmark yield heading for the biggest increase since February. The securities had extended recent declines as the central bank warned about potential risks arising from the relentless rally in debt markets.

In the local-currency bond market, most securities from developing countries fell on Monday, with Chinese as well as Polish 10-year yields rising about 5 basis points. Hungary’s yield rose for a fifth successive day, its longest streak since July 2, continuing a selloff amid inflation that spiked above the central bank’s tolerance range.

In the currency markets, Israel’s shekel led EM peers lower after an escalation of violence raised doubts about the prospects of a cease-fire. The country’s 10-year breakeven inflation rate advanced to a one-week high.

With markets moving in tight ranges on Monday, investors are awaiting US inflation reports this week to gauge the health of the US economy as well as the pace of Fed easing. Meanwhile, currency volatility remained high, with a JPMorgan Chase & Co. measure of options-implied swings in EM exchange rates hovering near a one-year high.

“If there is a big theme, it’s the extent of over-positioning in US assets that’s held globally,” said Geoffrey Yu, a senior strategist at BNY. “Generally, as the driver of risk-off has been fears over the US economy, and many EM investors, especially in APAC, have been buying USD assets, then the unwinding process would likely help these currencies versus the dollar.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Srinivasan Sivabalan, Colleen Goko