Wall Street Sees End of Fed’s Balance-Sheet Runoff This Year

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe end of the Federal Reserve’s balance-sheet unwind is in sight, though its actual conclusion depends on the pace of interest-rate cuts and stresses in funding markets.

Many on Wall Street agree that an abrupt end to quantitative tightening, or QT, is unlikely, with policymakers signaling its rolloff of Treasury holdings will finish by year-end. But recent data suggesting an economic slowdown as well the risk of liquidity pressures — already evident in the financial system — call that outlook into question.

“If the Fed is cutting to stimulate the economy, then QT will likely stop,” Bank of America strategists Mark Cabana and Katie Craig wrote in a note to clients on Wednesday. “If the Fed is cutting to normalize policy, then QT can continue.”

Mounting signs that economic growth is faltering more quickly than expected just weeks ago sparked a massive rally in global bonds on Monday as traders bet the Fed and fellow central banks would turn more aggressive in cutting rates.

The global repricing was so sharp that at one point interest-rate swaps implied a 60% chance of an emergency rate cut by the Fed in the coming week — well before its next scheduled meeting in September. Current pricing suggests about 38 basis points of cuts for September.

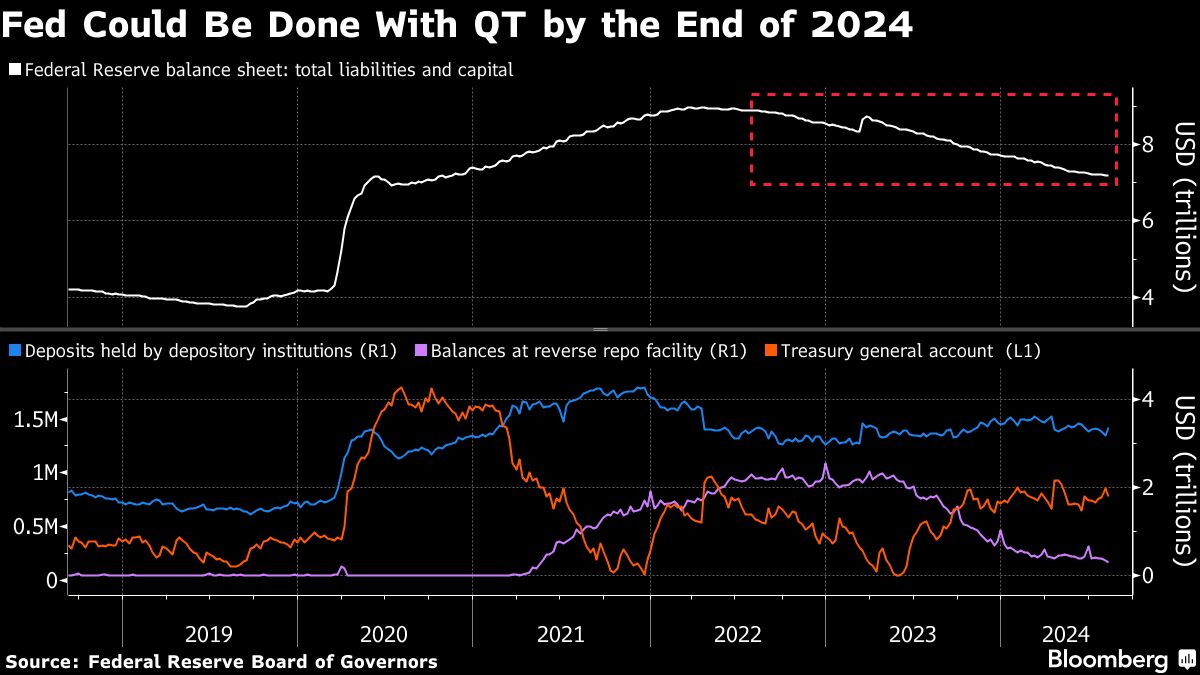

There’s also concerns over liquidity in the financial system and how much more can the Fed’s $7.2 trillion portfolio of assets shrink before worrisome cracks — similar to those seen five years ago ahead of an acute funding squeeze — start to appear.

In the past, policymakers have discussed the possibility that they may not have to stop QT when they begin cutting interest rates, as lowering borrowing costs works in the opposite direction of the policy seen as tightening monetary policy. But an abrupt downturn in the economy threatens a smooth transition.

While reserves currently at $3.37 trillion — the highest level in almost two months — are generally considered abundant, if the Fed lets the amount shrink too much it risks triggering volatility in overnight funding markets similar to what was seen in September 2019. The Fed, which has been unwinding its balance sheet since June 2022, recently slowed the pace in order to ease potential strains on money-market rates.

Still, signs of pressures are surfacing in funding markets. Rates on overnight repurchase agreements — loans collateralized by government debt — are rising amid elevated US government issuance and primary dealer holdings of Treasuries near an all-time high.

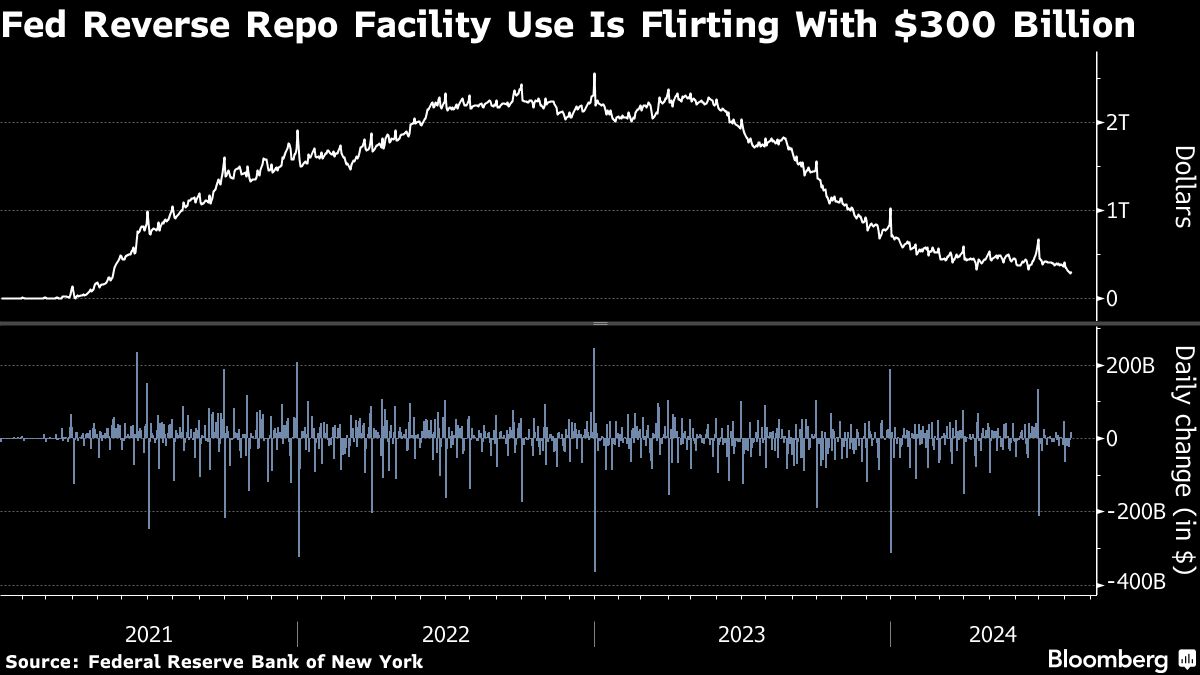

Meanwhile, balances at the Fed’s overnight reverse repo facility or RRP, considered a measure of excess liquidity in the financial system, until Thursday dropped in every session this month to $287 billion, the lowest in more than three years. They ticked higher to $303 billion on Thursday.

Even if funding pressures were to become more acute, backstops have been put in place to address potential strains, including sponsored repo, which provides relatively easy access to financing sources, and the Fed’s Standing Repo Facility, which lets eligible institutions borrow cash in exchange for Treasury and agency debt at a rate in line with the top of the Fed’s policy target range. Barclays Plc strategist Joseph Abate said repo rates are going to have to rise more before there’s active use of the tool.

“Two possible drivers could end the Fed’s QT program early: a drying up of liquidity in money markets, or a recession in the US,” Morgan Stanley’s Seth Carpenter, Matthew Hornbach and Martin Tobias wrote. “We see neither of these outcomes as likely.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All