Investor complacency is often blamed when rising stock markets ignore potentially unsettling data for weeks and then viciously sell off. But this very human-sounding characteristic mostly isn’t in the minds of traders: It’s baked into the structure of modern investment strategies.

The forces at work played a big role in Monday's market mayhem, shocking investors and sparking worries about a US recession and calls for an emergency rate cut. But these technical influences that have become a more regular occurrence after long benign spells helped turn a down day into a rout. The good news is they can burn out quickly — the bad news is that investors are still getting caught out and that can have repercussions beyond stock prices alone.

US stocks looked calmer first thing Tuesday. However, there is still plenty of selling pressure that could be unleashed by a wrong move in equities, and the high levels of volatility right now means that few of the investors that might typically buy a dip are likely to return quickly, according to Charlie McElligott, a strategist at Nomura Holdings Inc. in New York, who tracks the mechanics at play.

What’s behind all this is an often underappreciated set of structured products, quantitative funds and even individuals playing in stock options that all help to suppress market volatility when things are going well. But this builds a growing vulnerability that can cause a sudden earthquake. That fault line comes partly from the strategies themselves and partly from the hedging activity of dealers that take the other side of these bets.

For long spells, the strategies and hedging interact in a way that keeps stock markets in a virtuous circle of calm, steady rises. But when something triggers a fall in prices, that process can swing into reverse and create a vicious spiral of stock sales into falling markets that pushes volatility sharply higher and provokes further sales.

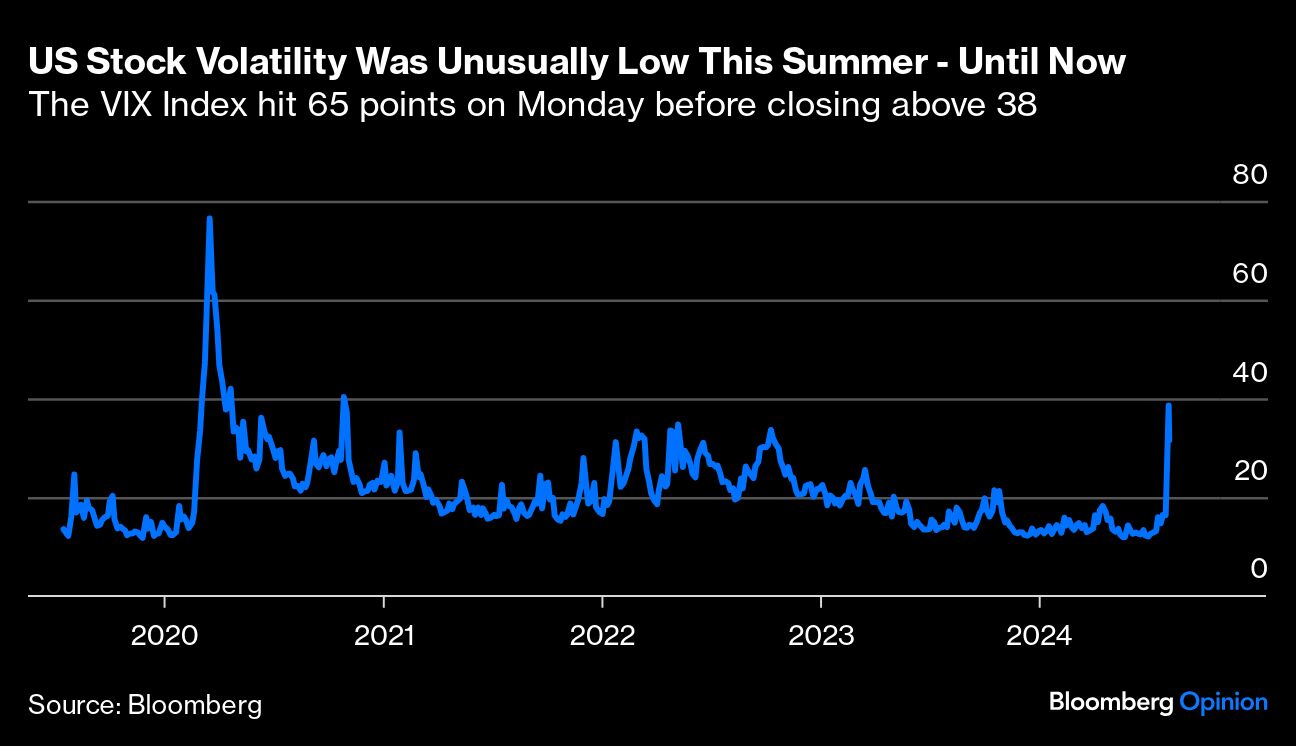

The growing vulnerability has been visible in the VIX Index, often called Wall Street’s fear gauge. It has been unusually low this year, but particularly between the middle of May and the middle of July. Strategists at JPMorgan Chase & Co. warned at the end of June that low US stock volatility was disconnected from high interest rates and economic news, leaving it vulnerable to a spike. “As long as the benign market environment persists, this virtuous cycle is likely to remain intact and keep volatility low,” the strategy team wrote. “However, in our view this is not a permanent feature and the volatility cycle will turn, perhaps rapidly – but it is difficult to predict when.”

The factors suppressing volatility that they highlighted included large volumes of activity from option-based ETFs, short-dated options (which are popular among retail investors) and risk-premia strategies, which involve trading options to exploit the different yields available from market inefficiencies. There are also so-called dispersion trades, which bet on the difference between single-stock options and index options.

These all lead to the kind of dealer hedging activity that helps to damp volatility for long spells, but can suddenly reverse and push volatility sharply higher. To get technical, options dealers are exposed not only to the changes in price of a related stock, but also to the change in the value of the options, which is known by the Greek letter “gamma.”

When the dealers’ gamma exposure is positive, they hedge their books by buying a stock as it falls in value and selling as it rises, thus balancing out other market flows. But when their exposure turns negative, which happens below certain stock-price levels, they end up selling into a falling market. You don’t need to be a rocket scientist to understand that isn’t good.

There are also systematic and quantitative funds that use volatility as an input to help calculate how heavily to bet on stocks, or other assets. When volatility is low and declining, it gives these funds a signal to increase their leverage – either borrowing more to juice their investments or using more derivatives.

The volatility suppression from options dealers’ hedging leads these funds into increasingly aggressive bets – and when the dealer activity goes into reverse, these funds also have to rapidly delever, adding to the wave of stock selling that hammers markets.

Such systematic equity strategies and trend-following funds known as CTAs were still overweight stocks compared with average levels at the end of last week, according to data from strategists at Deutsche Bank AG in New York, and would likely have been dragged into Monday’s selling.

At the end of Monday, the S&P 500 closed at 5186, which was mercifully above levels where dealers’ gamma exposure would have flipped to negative and led to another wave of selling, according to McElligott of Nomura. Avoiding those acceleration points – first at 5150 and next at 5000 – could help to keep markets calmer in coming days, but the trigger levels are constantly moving targets, he told me via email Tuesday morning. Also, still-high volatility is likely to stop investors that would typically “buy-the-dip” from coming back in: Many were positioned to do just that on Monday morning, but got burned when Japanese stocks provoked the wider market rout, McElligott added.

These dynamics have become a regular feature of benign markets in recent years as options trading has become more widely used by institutional and retail traders to speculate and boost income. Investors everywhere need to get better at recognizing the inherent vulnerability as it builds up — that way they are less likely to be shocked or caught out by the fuel that this all throws onto the fire when markets turn.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies