Fiscal conservatism has more or less vanished from America’s political landscape. Government borrowing, despite the strong economy, continues to push public debt to record levels – and the presidential contenders and their parties say scarcely a word about it. To the extent they discuss economic policy at all, their intentions on taxes and public spending would make the fiscal outlook even worse. The issue can be ignored for only so long. Sooner or later, it will kick the economy in the teeth.

That much should be obvious to anybody who glances at the most recent fiscal projections. In one way, though, the picture is even worse than the forecasts suggest. They disguise the rapidly escalating difficulty of solving the problem if the fixes keep getting postponed. “Yes it’s a problem and eventually we’ll get around to it” involves the fallacy that no matter how big the debt gets, it will submit to feasible remedial action. Not necessarily. A point is reached – and might not be far off – where the only feasible “remedy” is catastrophic.

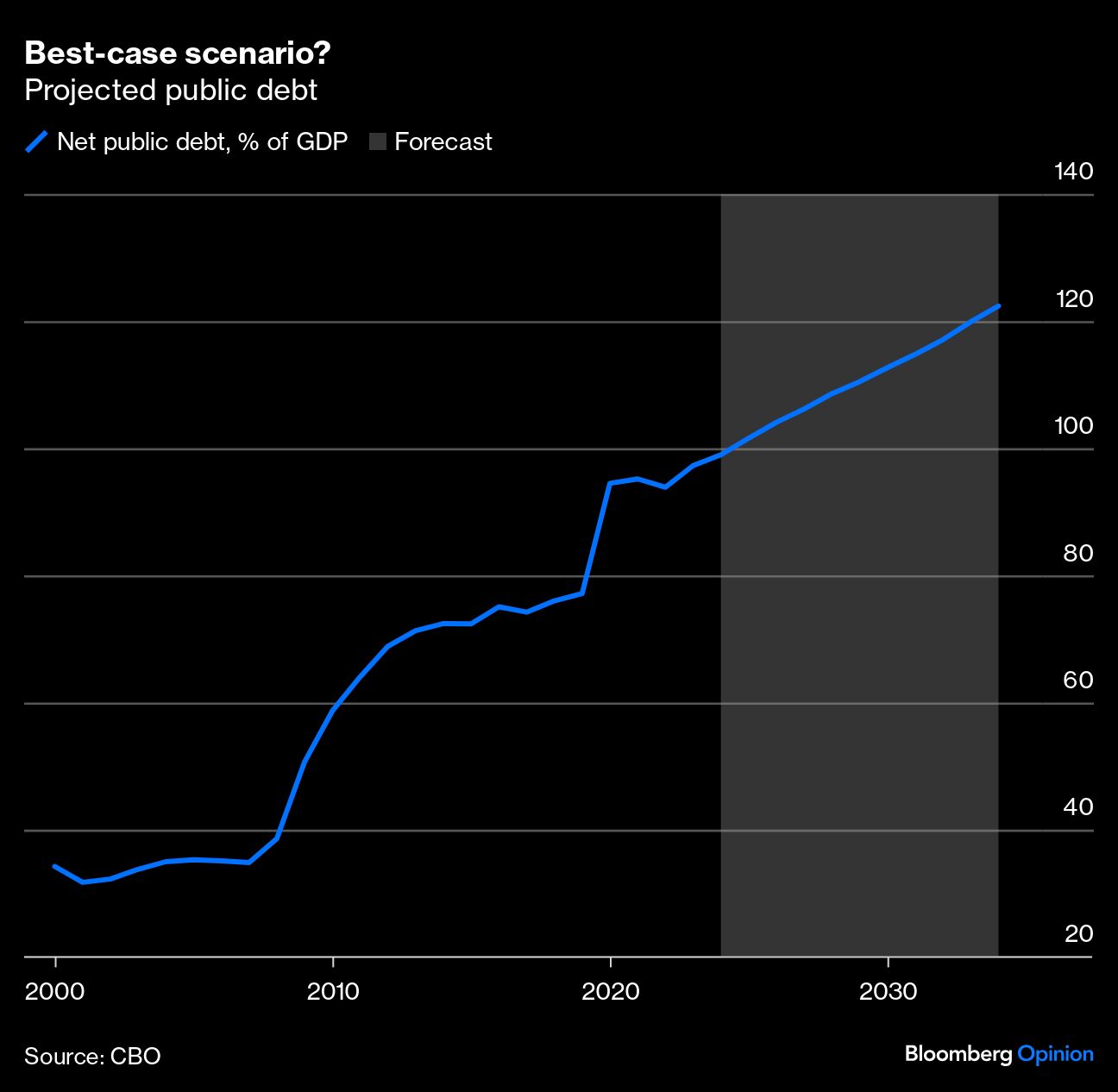

It's a matter of debt dynamics. The trajectory of public debt depends on two things – the budget balance excluding interest payments, or the so-called primary balance, and the difference between the cost of borrowing and the economy’s growth rate. Suppose the government pays for all its spending with taxes, so that the primary budget is balanced, and the long-term interest rate is roughly equal to the growth rate. Then the debt ratio would neither rise nor fall. Right now, the government is running a primary deficit of roughly 4% of gross domestic product with the inflation-adjusted interest rate about level with the growth rate. So the debt is growing quickly, from a little under 100% of GDP now to an expected 122% by 2034. As it does, it will put upward pressure on the cost of borrowing, which could put downward pressure on economic activity. In other words, the growth of debt is at risk of not merely persisting but accelerating.

The longer this cycle continues, the harder it becomes to interrupt. Already, the tax increases and/or spending cuts needed to eliminate the primary deficit are too big for politicians to contemplate – and, to repeat, depending on what happens to interest rates and growth, a balanced primary budget might not be enough to arrest the rise in debt. The longer action is delayed, the bigger the tax hikes, spending cuts and resulting primary surplus will need to be. At some point, an orderly resolution becomes politically impossible. That leaves default – either explicit or in the form of debt repudiation through inflation.

This prospect gets too little attention even among economists because many are still in thrall to the errors that were made after the recession of 2008. Back then, fiscal policy did too little to stimulate demand after it collapsed, and the subsequent recovery was too slow. “No more austerity” became the new watchword. It remains the prevailing view, even in the face of the opposite situation. Post-pandemic, the US piled fiscal stimulus on fiscal stimulus with the economy back at full employment. Hence the surge in actual and prospective debt. And regarding the outlook, remember that the standard forecasts assume that the Trump administration’s tax cuts of 2017 will be allowed to expire in full in 2026 and after (both parties say that won’t happen) and that there’ll be no recession in the next decade (let alone this year or next).

What about Japan, you might ask? Its gross debt has outstripped 100% of GDP for many years and now stands at more than 250%. So what’s the problem? Actually, on a consolidated net-liability basis, Japan’s debt ratio is about the same as the US’s. More of its debt is owed to other parts of the government, and the government has lots of assets. Also, Japan’s debt is much easier to service because its borrowing, mostly from domestic savers, is very cheap and its assets earn high returns. Forget Japan. The idea that the US doesn’t need to worry until its debt gets a lot higher is wrong.

Some new simulations underline how difficult fiscal stabilization would be even if it were attempted immediately. According to this exercise, a hefty spending cut equivalent to 1% of GDP would not, by itself, stabilize the debt ratio. Nor, by itself, would a substantial increase in taxes (such as letting the 2017 tax cuts expire). Faster-than-expected growth sustained for years also wouldn’t do it. And there’s no longer any politically feasible way to stabilize debt quickly – say by 2026. It will take much longer, with some combination of lower spending and higher taxes to get deficits under control, starting right now, with the effort sustained beyond the short term, and no recession in the meantime. A tall order? Not nearly as tall as it will be after another year of doing nothing.

A reasonable bet to place today is that the problem won’t in fact be solved. When financial markets come around to that way of thinking – causing long-term interest rates to rise and demand to shrink – it will be a self-fulfilling prophecy. And then we’ll see what “unsustainable” debt really means.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Clive Crook