Friday’s weaker-than-expected jobs report has sparked a robust debate about whether the economy is sliding into recession or whether the rise in the unemployment rate in July was due to a continuing post-pandemic normalization of the labor market. Whichever camp you’re in, the right move for the Federal Reserve is to act with urgency, cutting its policy rate a percentage point to 4.25%-4.5% by the end of the year in the name of risk management.

It’s a level of easing that the Fed is likely to undertake even if the rise in unemployment ends up being somewhat benign since we no longer need such restrictive rates to tame inflation. It makes sense to frontload those rate cuts rather than run the risk of being too slow to act to forestall worse economic outcomes.

If we really are heading into recession, there’s not much disagreement on what the Fed should do: Cut interest rates a lot and fast. That’s where market pricing has shifted after a rocky week of economic data. Interest rate futures suggest the Fed will cut its policy rate by over 200 basis points by the end of 2025, taking the fed funds rate down near 3%. This seems reasonable based on what we’ve seen in prior recessions.

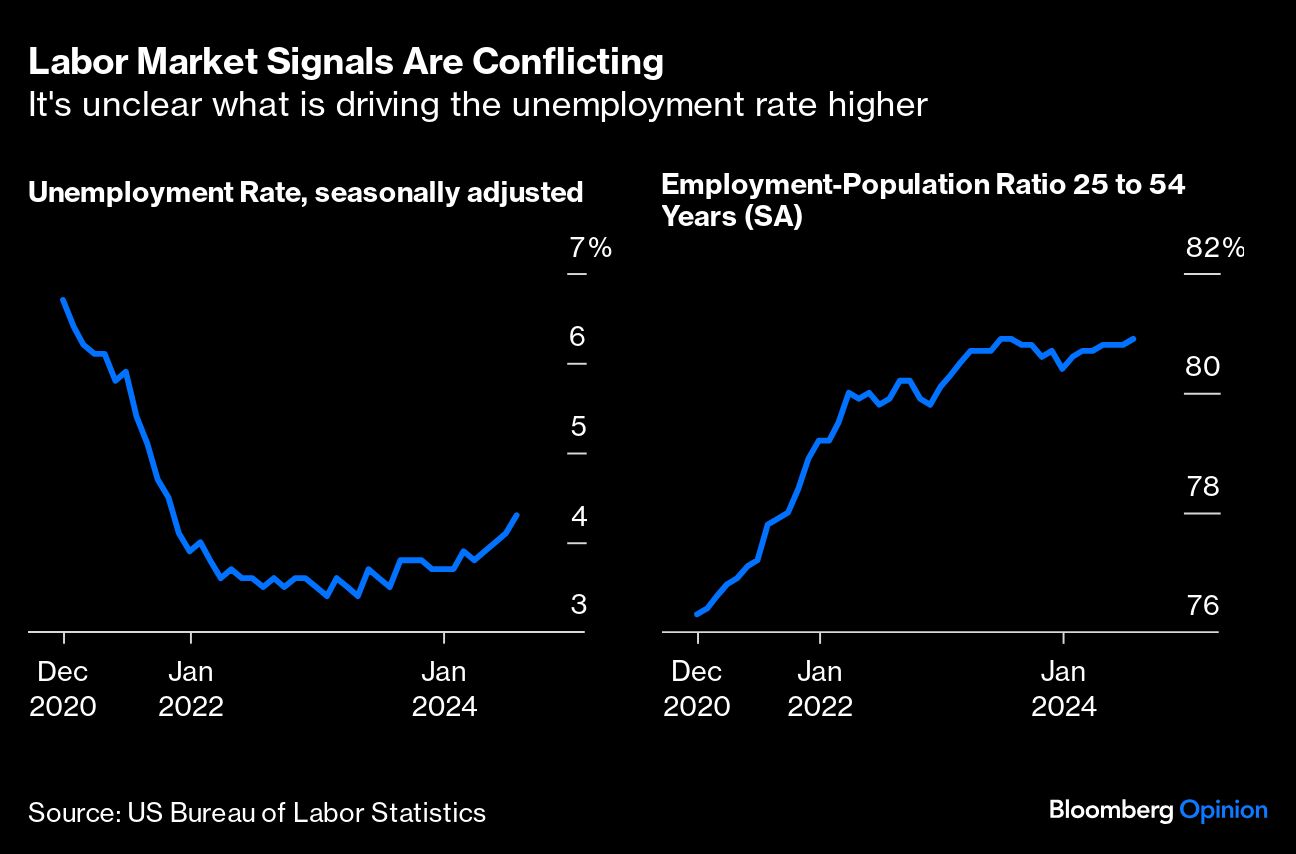

It’s the second scenario that is more challenging. The jobless rate has climbed this year from 3.7% to 4.3%, but the percentage of people between the ages of 25 and 54 who are employed has also risen, from 80.4% to 80.9%. That’s an unusual dynamic with the unemployment rate reflecting, in part, rising labor force participation.

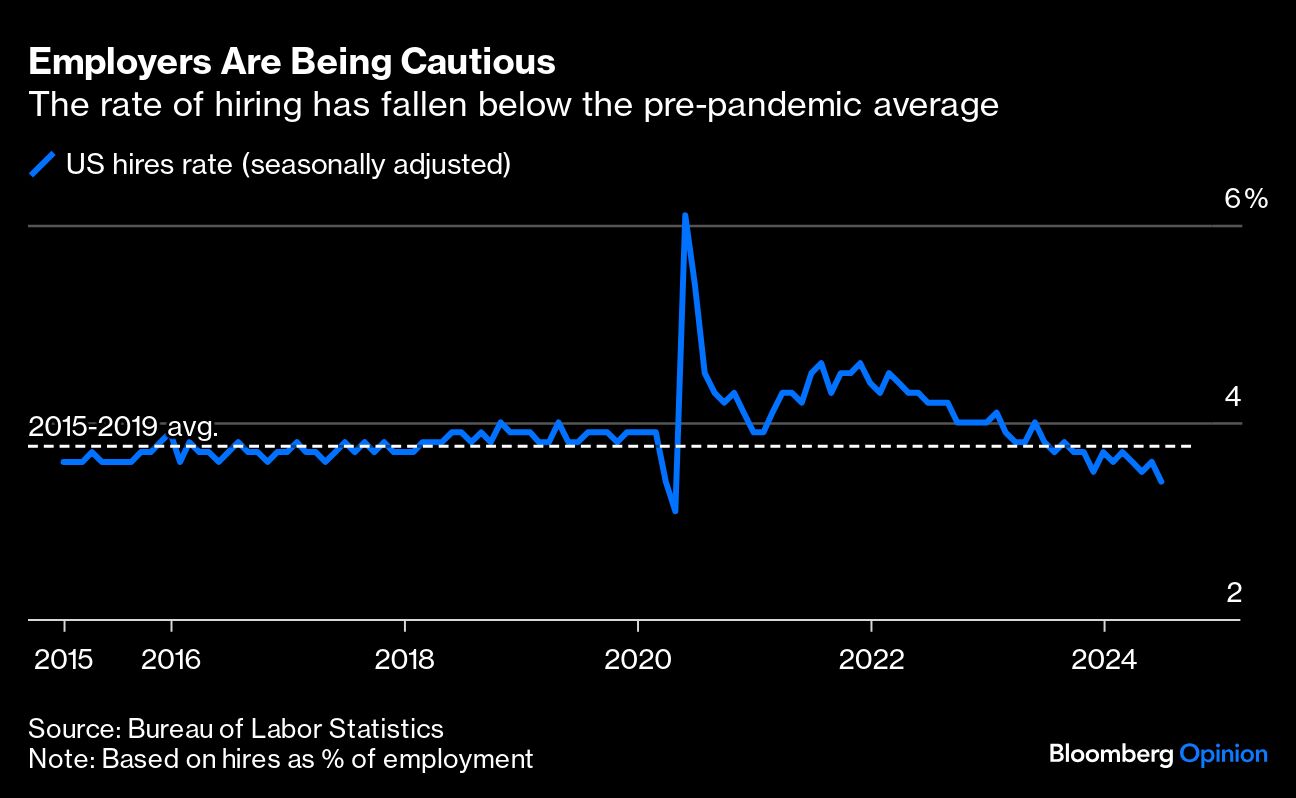

It’s possible that the explanation of a gradual normalization is the correct one, that there’s little risk of a rapid increase in unemployment, and that the Fed has time to be patient. But putting all of one’s eggs in that basket is risky. The rate of layoffs is currently low, but waiting for job cuts to increase means waiting until it’s too late to avoid a recession. During the financial crisis, for instance, layoffs didn’t start to spike until the middle of 2008 once a recession was well underway. The hiring rate has already slumped to levels that suggest employers feel no compulsion to add to their payrolls.

In general, it’s best not to overthink the unemployment rate. Inflection points in the economy are messy and uncertain by nature, and leaning too much into optimistic scenarios can cause severe policy errors. Former Fed Chair Ben Bernanke gave his “subprime is contained” speech in May 2007 when the housing market was already in the process of collapsing.

The central bank’s job is risk management. It’s why policymakers continued to increase interest rates in the first half of 2023 well over a year after their preferred measure of inflation had peaked and begun to decline. In June, the Fed’s “dot plot” — an anonymous collection of policymakers’ rate expectations — showed a median projection for a 25-basis-point cut in 2024 followed by four more reductions in 2025, or 1.25 percentage points of easing overall. Both the labor market and inflation data have weakened since then. A revised dot plot today would likely show more aggressive cuts, and we know from Chair Jerome Powell’s comments on Wednesday that policymakers are prepared to lower rates in September.

So why wait? Inflation risks have moderated sufficiently, so the main argument against cutting more aggressively than they’ve previously signaled would be the risk that markets are alarmed by what that says about the economic outlook. Fortunately, Powell can use his upcoming speech at the Kansas City Fed’s conference in Jackson Hole, Wyoming, to shape the narrative.

Swift rate cuts would relieve pressure for Americans struggling to make payments on floating-rate credit card debt or to get financing for a new car. It would help the millions of homeowners who bought when mortgage rates were high, with refinancing at lower rates freeing up household budgets for other types of consumption. The main headwind for the economy right now is high borrowing costs.

Foot dragging among policymakers harkens back to the economic situation and Fed debate from early 2022. At the time, the dispute was over whether inflation was transitory, and whether raising interest rates by 25 basis points once a quarter would be too fast. Ultimately, the inflation situation got worse, and the Fed had to respond aggressively. Many economists now believe the delay in raising rates was a mistake.

Now, we’re in the opposite situation with a cooling labor market. The Fed has already signaled a likelihood of cutting rates at the September meeting. Policymakers lose little and have much to gain by moving quickly.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen