Warren Buffett has been selling a lot of stock, and that revelation is inducing his many admirers to follow suit. His Omaha, Nebraska-based conglomerate, Berkshire Hathaway Inc., reported Saturday that it reduced several positions and slashed its stake in top-holding Apple Inc., a sign to some in markets that the “Oracle of Omaha” was bracing for deep stock-market declines. The intended message wasn’t actually as clear-cut as meets the eye, but that nuance might not matter given the speed of the sentiment tailspin in markets.

At the time of writing, the S&P 500 Index had plummeted around 3%. I have no idea what proportion of that reflects Buffett, but it’s fair to say that his unfortunately timed disclosure was part of the sentiment stew.

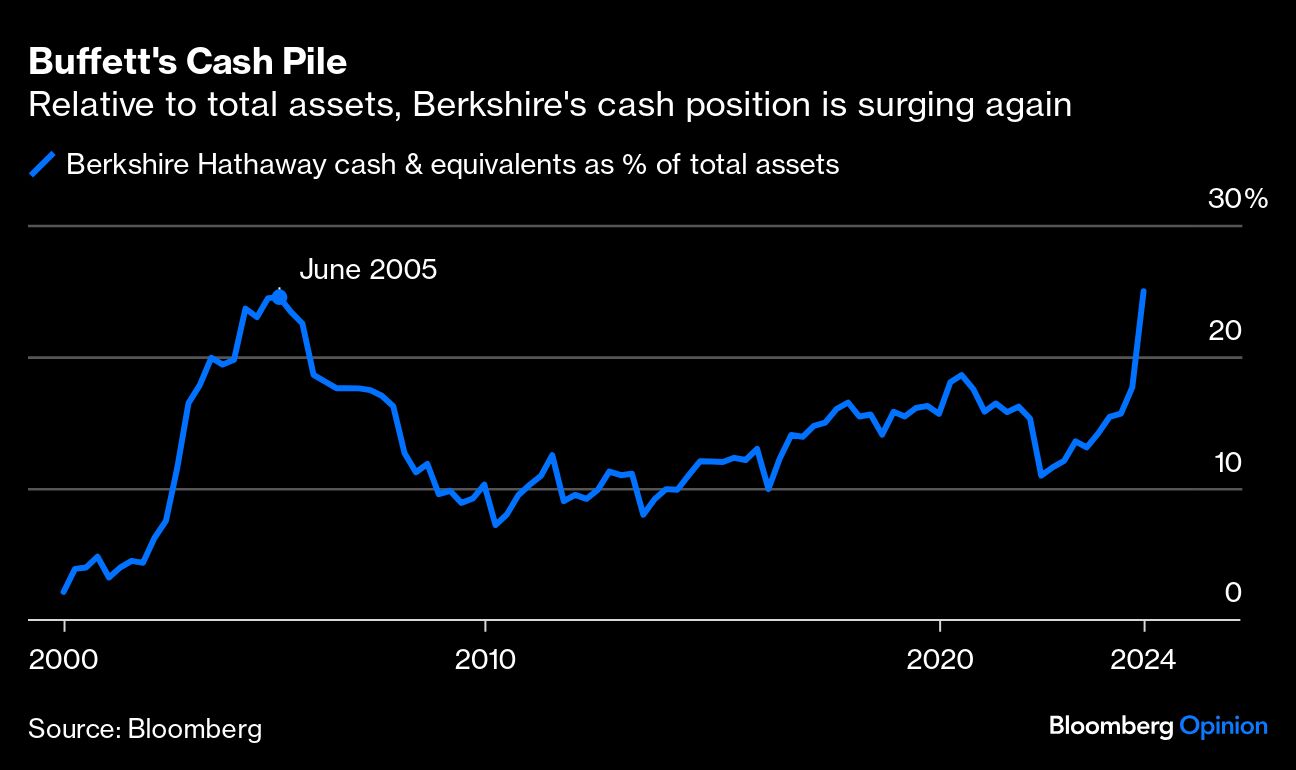

As a proportion of total assets, Berkshire’s cash and equivalents of a record $276.9 billion are now officially back to their highs from the mid-aughts, before the financial crisis when a cash-rich Buffett famously scooped up iconic investments at bargain prices. On an absolute basis, Buffett’s cash hoard has hit records for several quarters, but I brushed it off until now because cash levels weren’t that high relative to other measures of the firm’s size. That excuse is no longer valid.

The Berkshire news comes at a point of particular vulnerability in markets and the economy. Together with excess savings and low unemployment, high asset prices — sustained in part by elevated US large-cap valuations — have been one of the three pillars of US consumption in recent years. Excess savings have been dwindling for some time, but personal wealth and the labor market seemed to be holding up well until last week. Now, suddenly, the consumption story feels unstable. Two days after the Federal Reserve forwent an opportunity to cut policy rates, a Bureau of Labor Statistics report Friday showed that the unemployment rate rose to a nearly three-year high, starting the selloff that Buffett helped continue.

Even if we assume that wealth trends have a proportionally small effect on consumption, the increase in stock portfolios and home equity has been so extraordinary — until now — that they must have had some impact. Household net worth surged by about $41.5 trillion from the end of 2019 to early 2024. The abrupt about-face in stock prices also comes at a time when the housing market seemed to be struggling and excess savings left over from the pandemic are drying up.

But what was Buffett really thinking anyway?

First, Buffett already told us to expect some stock sales, at least partially for tax reasons. At the Berkshire Hathaway annual meeting in May, he shared his very understandable concern that the yawning federal budget deficit may lead to higher capital gains taxes down the line. “I don’t mind at all, under current conditions, building the cash position,” Buffett said at the time. “When I look at the alternative of what’s available in the equity markets and I look at the composition of what’s going on in the world, we find it quite attractive.” For all the stock’s medium-term prospects, the Apple sale seemed to reinforce the view that technology and communications shares have gotten too rich. Berkshire also reduced its Bank of America Corp. holding, apparently favoring government securities yielding over 5%.

Second, Buffett has always bristled at the notion that he can somehow forecast the future or time markets. He made his name as a long-term investor who finds good companies at reasonable prices and rides them for years or decades. If his moves around the financial crisis count as market timing, it’s worth recognizing that they weren’t as precise as legend would suggest.

Berkshire dramatically built up its cash hoard from 2002-2005 and then kept it around record levels until the end of 2007. What we remember now is how smart Buffett and his late-sidekick Charlie Munger looked during the crisis when they used their spare cash to scoop up investments involving Goldman Sachs Group Inc., General Electric Co. and Dow Chemical Co. But we often forget how stubborn they looked before the crash: Berkshire significantly underperformed the S&P 500 from the end of 2002 to mid-2007. In hindsight, perhaps that was a sensible risk-reward tradeoff, but history shows that the economy doesn’t immediately melt down just because Buffett has gone to cash.

Finally, Buffett still owns a lot of stock and, in particular, about $84 billion in Apple. Apple stock has returned around 30% a year since Buffett first disclosed his position in 2016. In one interpretation, it’s actually a sign of confidence when you see an investment go up by that much and only take about half your chips off the table.

All in all, I’d normally be cautious reading too much into the Buffett news in and of itself, much as I thought the handwringing about the latest jobs data was a bit overblown. An Institute for Supply Management report published shortly after the start of trading showed that its index remained in expansionary territory, a glimmer of hope that led to an intraday reprieve from the market panic. Perhaps some more news like that — including some benign initial jobless claims numbers — can still stem the tide. But for now, I remain worried we’re in the midst of a negative vibes maelstrom that could be hard to stop. Declining asset values may just make a wobbly labor market even wobblier, and consumption could struggle as a result. That may not have been the Oracle’s intended outcome, but his role in it is impossible to ignore.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin