A Straight Man and a Funnyman Explain the World Economy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTo get a mental picture of The New World Economy in 5 Trends, imagine an architectural folly, a structure that’s sturdy at its base but with turrets, parapets, gables, and gargoyles on top. Now, instead of a building, think about a book that has two authors but that is not co-authored in the usual way – instead, the two take turns writing chapters so that the book is a straight man/funnyman show, with the straight man providing mostly sound, conventional analysis and the funnyman interviewing dead economists and Fed chairmen not yet born.

You now have a pretty good idea of what Koen De Leus and Philippe Gijsels’ unconventional new book is like. 5 Trends is confusing, full of errors, and almost unreadable because of its wacky structure.

You now have a pretty good idea of what Koen De Leus and Philippe Gijsels’ unconventional new book is like. 5 Trends is confusing, full of errors, and almost unreadable because of its wacky structure.

But it is not worthless. There are good ideas in it. The authors correctly identify five of today’s most important economic trends and discuss them at length. I do not recommend the book, but after unburdening myself with a list of complaints about it, I will comment on some of the valuable material hidden within.

And, to be fair to the funnyman, he is also a dreamer and futurist who provides some interesting insights, although occasionally they’re flat-out wrong. (“Chicago is on the rise.” No, it’s not.)

What are the five trends?

De Leus and Gijsels, both originating in the world of institutional brokerage,1 identify the five principal trends affecting investments in the near future as:

- Innovation and productivity – we’re going to have a boom, not a bust;

- Climate – whether you’re a hawk or dove, a lot of change will take place and a lot of money will be in motion;

- Debt – it’s a serious problem;

- Aging – it will weigh heavily on the economy, but tech-driven growth will overpower it; and

- Multiglobalization – we are not going to have a deglobalization depression.

Casting a shadow over these developments, the authors emphasize, is an economic megatrend: the 40-year era of declining interest rates is over. Interest rates will rise, affecting each of the other trends in profound ways.

The most interesting idea in the book is one they call “multiglobalization.” I will devote a little extra space to that issue at the end.

First, let’s fire all the proofreaders

First, let’s fire all the proofreaders

First, let’s fire all the proofreaders

First, let’s fire all the proofreaders

Before commenting on the five trends (and the overarching theme of rising interest rates), I want to vent my frustration with the publisher. The book contains a blizzard of typos and outright errors that a competent publisher would correct. Einstein never said that the eighth wonder of the world is compound interest, and he certainly didn’t expand on that thought as the authors say he did.

The authors also misquote Hemingway, butcher philosopher-businessman Nassim Taleb’s name (“Nicolas Thaleb”), call developing countries developed and vice versa, and get both the name and location of a Viennese hotel wrong. Malcolm Gladwell is “Malcom”, Marc Faber is “Mark”, Mark Carney is “Marc”, JCPenney (the company) is “JCPenny,” and George W. Bush is “George Bush Jr.” in one place and “George W. Bush, Jr.” in another. (Mr. Bush isn’t a “junior” at all.)

More damagingly, the authors say that “quantum computing will provide almost free energy.” No, it won’t. “Free energy” is a term from theoretical physics that is sometimes used in connection with quantum computing, but it does not mean “free of cost.” The sentence is wrong and misleading. If the authors make mistakes that are this serious, we have to wonder: how accurately have they portrayed concepts that we can’t as easily fact-check?

All right, I’ve vented enough.

“One Trend to Rule Them All”

In an homage to J. R. R. Tolkien, the introductory chapter is called “One Trend to Rule Them All.” What is this king of trends? After rambling through Assyrian philosophy, a truly bizarre interlude called “And Eternally Pounding Elephants,” a hat tip to Edward Chancellor’s wonderful book The Price of Time (which I reviewed here), and a decade-by-decade review of market leadership, the authors identify the super-trend: the interest-rate cycle is more important to equity markets than the economic cycle.

This is correct. The interest-rate cycle is the trend that rules the others because markets discount many future economic events, near and distant, to arrive at a price. Thus, short- and medium-term economic fluctuations have limited impact. However, the interest rate – or more properly the yield curve – is the rate the market uses to discount all these future events and thus “rules them all.”2

We were in an interest-rate bull supercycle for almost 40 years, from the peak 10-year Treasury bond yield of 15.82 percent in 1981 to the trough of 0.32 percent in 2020. This sea change massively boosted equity valuations. Sidney Homer and Richard Sylla’s 5,000-year study of interest rates showed that nothing like this had ever happened before,3 so we shouldn’t expect it to happen again (and it can’t unless interest rates, God forbid, rise back to almost 16 percent).

Most of the people who were active in financial markets in 1981 have retired, left the business, or died, so there’s very little institutional memory of the previous era of rising rates and endlessly stagnating markets. The authors are wise to caution us about the dampening effects of rising interest rates on both asset prices and various aspects of economic activity.

Innovation and productivity

The global outlook for innovation and productivity is good. Innovators cluster together geographically, and the more they cluster, the more prosperity they generate. Traditional high-tech capitals – the U.S. east and west coasts, the UK, and Germany – have been supplemented by new ones in China, Taiwan, Israel, and India.

But high tech is not the only source of innovation. What the scholars Dan Breznitz and Peter Cowhey call “incremental product and process innovation” is just as important.4 It's the reason your car has intermittent windshield wipers and why LED lightbulbs last 50,000 hours. Such medium-tech innovation is distributed much more widely than high tech, and the innovators are often tinkerers or line workers, not PhDs in research labs.

Given these favorable conditions, the authors expect productivity (output per hour worked) to double in “the long run.” But is this good or bad news? It depends on what “the long run” means.

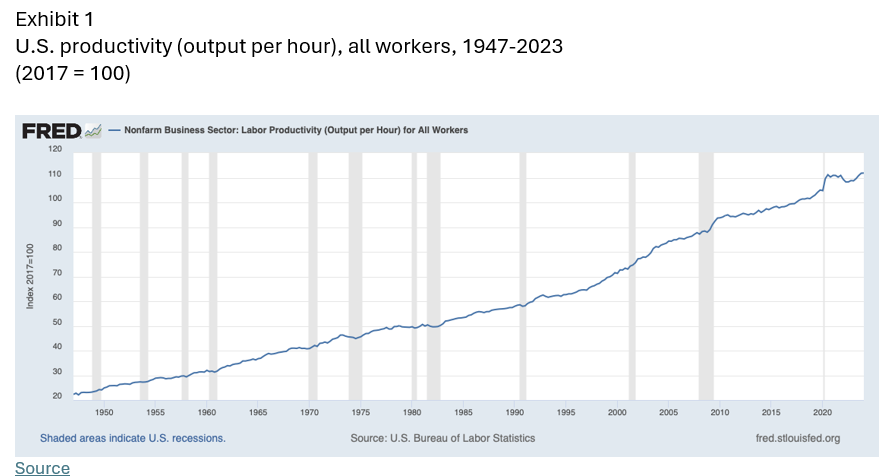

Exhibit 1 shows the historical rate of productivity growth in the U.S., 1.8 percent per year compounded over 1947-2023. At that rate, productivity has doubled about every 40 years.

If you go back farther, to the beginning of the Second Industrial Revolution around 1870,5 productivity doubled about every 40 years over that period too. So merely maintaining that rate of growth is roughly what we should expect from a modern, dynamic economy.

Compared to the near-zero growth that prevailed over most of human history, a 1.8 percent annual growth rate, were it to continue for a long time in the future, would be fantastic. Growth at that rate catapulted the economies of the industrialized world from poverty to affluence in the last century and a half, and its continuance would be a big success.

However, under current conditions it’s not quite enough. To boost the standard of living in developing countries to middle-class levels over a reasonable time frame – and to do that in the face of extraordinary adjustment costs caused by the threat of climate change – we’d hope for even faster growth.

Where will the growth come from? The authors expect technology to deliver a near-miracle. Looking back from 2042, in one of their imagined newspaper clippings from the future, they write, “Rosy scenario for productivity confirmed – Quantum computing changes everything.” They also include AI, energy, biology, and 3-D printing as “exponential technologies,” which they define as those that improve at a 10 percent or greater annual rate for long periods. While both the numbers and the tone seem too exuberant to me, I’d also call materials science, agritech, and possibly space exploration “exponential.” We are in the middle of several technological revolutions at once, and the productivity numbers will eventually reflect that fact.

On the negative side, we find higher taxes and interest costs, political and national security troubles, and an aging population. But, on net, the authors expect productivity growth to accelerate, not stagnate.

Climate

De Leus and Gijsels are climate hawks, although they express their position guardedly:

...[T]he scientific probability that something is seriously wrong with the climate is more than strong enough to change our human behaviour on a global scale. Even if much alarmism turns out to be exaggerated, we would still do well to accelerate the process of treating our planet in a much more sustainable way... To do so, we need to ramp up our climate efforts very quickly.

Newborn has a personal carbon emissions budget for their lifetime that is one-eighth that of their grandparents.” That budget is unlikely ever to be adhered to. The average global newborn, if such a person exists, is in a middle-income country like Indonesia, and her grandparents used a trifling amount of carbon. So, while the authors sensibly ridicule “degrowth” as a path to ruin, what they’re proposing for our prototypical newborn is a particularly painful dose of degrowth, unless a truly miraculous new energy source emerges. The authors’ climate positions, then, are inconsistent and hard to take seriously.

To investors, however, what matters is not what should be done but what will be done. A massive amount of public and private money will be spent on the energy transition. Astute investors can earn superior returns if they have the skill to distinguish real from fake opportunities that arise from this spending. In addition, the money will have to come from somewhere, in large part the taxpayer, so stocks relying on consumer spending are likely to be under pressure.

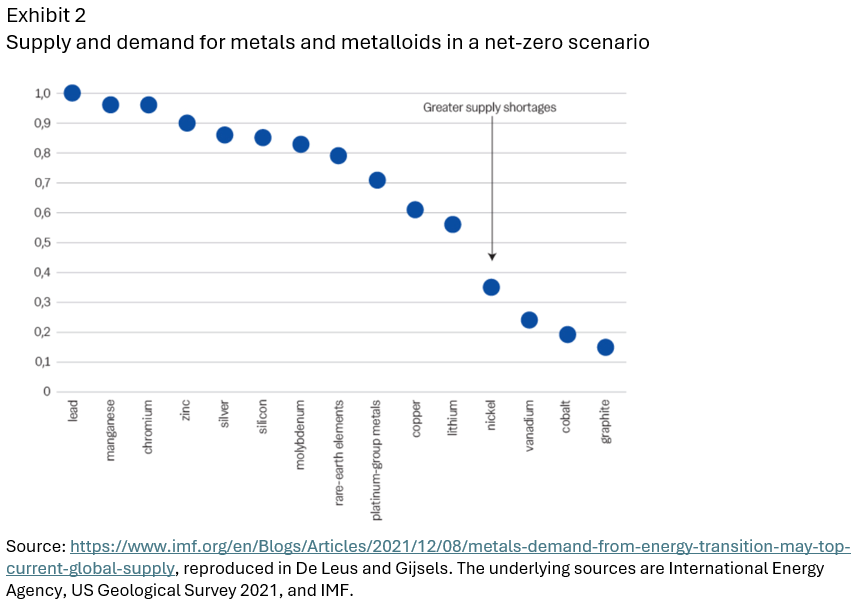

Finally, the authors expect a bull market in commodities, especially metals used in solar, wind, and nuclear energy installations.6 Even though the commodity prices most keenly felt by consumers, fuel and electricity, are currently high, the broader S&P GSCI Commodity Index first reached its current level 17 years ago7 and is a bargain if the authors’ supply-demand analysis for metals and metalloids, obtained from the IMF and shown in Exhibit 2, is correct. The y-axis is the ratio of the amount supplied at current production rates to the amount that the IMF expects to be demanded in a net-zero scenario. Of course, production rates will change in such a scenario, spurred by higher prices. And a true net-zero scenario is unlikely to unfold.

Inflation, interest rates, and debt

For decades I’ve been hearing that government debt, both in the U.S. and elsewhere, is a time bomb. But, in developed countries, it never seems to explode. That’s because governments own the “printing press,” an economist’s metaphor for the ability to increase the money supply by adding to the bank reserves of central banks. This creates inflation, making the government’s debt (principally Treasury bonds, held by savers) less valuable in real terms. In other words, savers defuse the bomb – pay off government debts in nominal although not real terms – by watching their purchasing power slowly disappear.

De Leus and Gijsels begin their chapter on debt with a news flash from 2052, in which “the UK government could no longer get rid of its sterling loans, even with interest rates close to 20%.” In this imagined crisis, the EU reluctantly had to bail out the UK.

Looking back from 2052, the authors add that “the United States...managed to avoid a financial crisis, notwithstanding a debt level comparable to that of the UK in the early 2030s, ...by introducing... artificially low interest rates and a 4% inflation target.”

How governments use financial repression to pay their debts

But the U.S. avoiding a debt crisis through low interest rates and not-so-low inflation isn’t futuristic speculation – it’s recent history. Because of the zero interest-rate policy that was only recently abandoned, a dollar invested in Treasury bills at the beginning of 2009 grew to only $1.06 by the end of 2021, a pitiable nominal rate of return. Meanwhile inflation caused goods and services that cost $1.00 in 2009 to rise in price to $1.26 by the end of 2021. Since 2021, the inflation rate has been even higher.

Put another way, over 2009-2021 the U.S. government confiscated 20 cents of each dollar originally invested in Treasury bills, and spent the money. If the government had not had this additional revenue, it would have had to borrow that much more to maintain its spending level. This is the sense in which savers pay a government’s debts. Economists call it “financial repression” and anyone who owned fixed-income investments through that period has every right to feel repressed. It’s a nasty hidden tax.

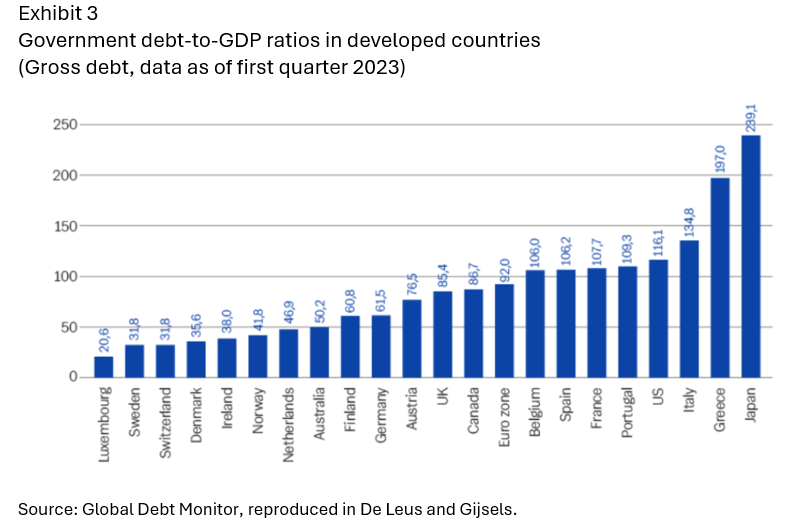

De Leus and Gijsels tell this story, with local variations, for the major countries of the world. They are not debt super-hawks. In support of governments using debt as a legitimate tool, they quote Barry Eichengreen, who said that a government failing to go into debt in an emergency is like a parent failing to borrow for their child’s cancer treatment. But, when you’re a politician spending other people’s money, it’s always an emergency. There’s no other way to explain the huge debt-to-GDP ratios shown in Exhibit 3 for the countries toward the right side of the graph. The U.S. is the fourth biggest debtor, relative to GDP, of the countries shown.

Consumers in the countries in the right half of Exhibit 3 can expect a lot of inflation between now and the 2052 date of the authors’ “news” item. And there may be a few government bond defaults, although not in the United States.

Growing our way out of the debt problem

There is, however, a formula, widely accepted in public finance circles and mathematically correct, for getting out of a debt trap. It is simple but not easy: government spending has to grow more slowly than the economy. If the economy, and thus tax receipts, grows faster than government expenditures, the debt/GDP rate goes down (by mathematical certainty) and, over a surprisingly short period, reaches sensible levels. This worked for Sweden between 1998 and the present, Canada prior to 2008, and the U.S. in the 1990s.8

But even if this process “works” and the debt/GDP ratio falls, it won’t be pretty. Interest and inflation rates will remain high and government services and benefits will decline.

Aging

Everybody knows that societies around the world are aging. It’s just as well. Since the resources of the Earth are not infinite, they cannot support an infinite number of people, so the population explosion had to end sometime and, in my view, better now than later.9 And, as birth rates fall, the average age of the population rises until a new equilibrium is reached.

Low birth rates are a sign of prosperity. When parents invest in the quality rather than the quantity of their children, it means that (1) they expect almost all of their children to survive to adulthood, something that is new in human history; and (2) the children will be more skilled, better educated, whatever your metric for child quality is.

But it is possible to overdo a good thing. At current birth rates, the native population of South Korea and Taiwan will fall in half each generation; do that a few times and the country basically disappears. Birth rates in Italy and Japan are not much better.

Is an aging society good or bad for investors? De Leus and Gijsels mostly emphasize the negative: “A declining population limits future growth potential and also challenges the financing of our social security model.” This is a valid concern, although the idea that older people are less productive comes from the pre-industrial and industrial eras when strength and endurance were the attributes a worker needed most. Today, even in many of the less developed parts of the world, “think work” dominates on a paycheck-weighted basis and, in some such places, is starting to dominate in absolute terms as it does in the U.S., Europe, and Japan. Older people actually think better.

Really? The psychologist Raymond Cattell distinguishes between fluid intelligence, “the ability to solve abstract reasoning problems,” and crystallized intelligence, “learned procedures and knowledge...[that] reflects the effects of experience and acculturation.”10 Fluid intelligence is said to decline after age 27 – that’s why so many mathematicians are young – but crystallized intelligence grows through middle age and only starts to decline around age 65. So, in a society where “think work” is the primary source of material success, an aging population is not all bad.

But it’s not all good either. The authors remind us that “oldtimers do not innovate.” They may think integratively, manage organizations, mentor the young, and provide institutional memory better than young people, but they don’t found startups. So there is an upside and a downside to an aging population.

What is multiglobalization?

As promised, I’ve saved the authors’ best idea for last. After reviewing the ups and downs of globalization, deglobalization, reglobalization, offshoring, onshoring, nearshoring, and friendshoring, the authors remind us that the U.S. is not the only country in the world that uses goods and services manufactured elsewhere. Everybody’s doing it. China desperately needs vegetables – Chile has them in abundance. An opportunity for vigorous trade lies therein.

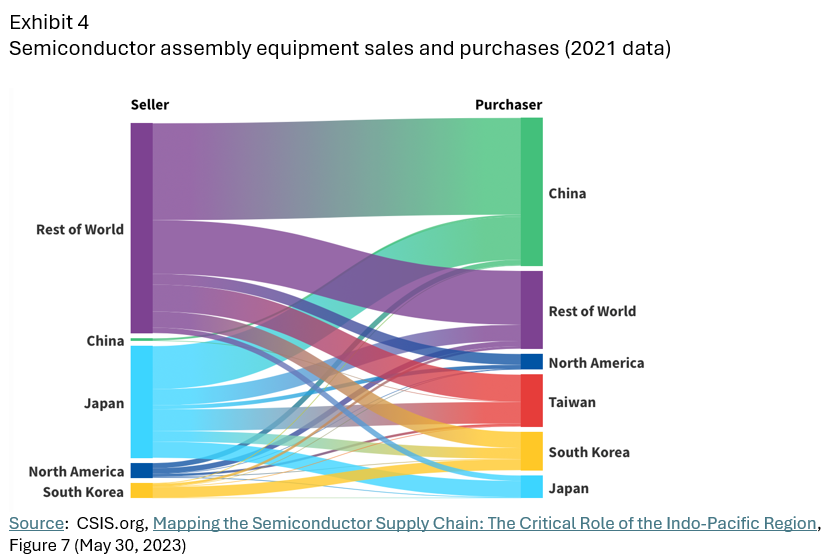

But that’s very simple interdependence of the kind that has existed for millennia. Chip manufacturing is multi-country interdependence at its wildest. The Sankey diagram in Exhibit 4 shows where the sellers and purchasers of one type of equipment used in semiconductor manufacturing are located..11

The diagram shows a lot of trade outside the U.S.-China axis: “rest of world” (dominated by Europe) trades heavily with China, Taiwan, and South Korea – and with other countries in the “rest of world.” This is a vivid example of what De Leus and Gijsels awkwardly call multiglobalization. The development economist Jan Nederveen Pieterse calls it multipolar globalization, which is wordier but clearer.12 Whatever you want to call it, it’s a good thing, enhancing profits and livelihoods.

The future of the global supply chain

The diagram in Exhibit 4 is about to get even more complicated. According to The New York Times (March 20, 2024), “The Biden administration is investing $39 billion to help companies build more factories in the United States to bring more of this supply chain back home.”

But it’s not coming home.

“Even after U.S. facilities are built,” the Times continues,

...[C]hip manufacturing will remain decidedly global. Inside [the American manufacturing firm] Onsemi’s New Hampshire plant, the process begins with a jet black powder of silicon and carbon from Norway, Germany, and Taiwan. The powder is added to graphite and gases that come from the United States, Germany, and Japan..., producing a crystal that... is sent to a factory in the Czech Republic to be sliced into thin wafers using special machinery from the United States, Germany, Italy and Japan.

The wafers are shipped to an ultraclean factory In South Korea, where mechanized pails carry them between complex machines from the Netherlands, the United States and Japan... The wafer is then cut into tiny chiplets, which travel to facilities in China, Malaysia, and Vietnam for finishing touches and testing....

Finally, the chips are sent [from global distribution centers in China and Singapore] to Hyundai, BMW and other automakers in Asia and Europe, which put them into power systems for electric vehicles. Other chips are sold to auto parts suppliers in Canada, China and the United States.

Got that?

The global supply chain is a near-miracle of inventiveness, cooperation, and cheap shipping. It is responsible for much of our prosperity. No one could design it from the top down – it just happened, the result of myriad businesses deciding what actions were best for its customers and shareholders. Disassembling this machine and reassembling it in a different form, to meet political or national-security goals, is a risky and expensive proposition. I hope we disrupt this system as little as possible.

Yet some deglobalization is inevitable. The whole system of global trade depends on the security of shipping lanes and air routes, currently guaranteed by the U.S. military. But the guarantee is not ironclad. Thus, a prudent approach is to have some redundancy in the system, so that, in some future scenario, if (say) chips cannot bounce around the world unencumbered as the Times article describes, we can manufacture some of them here.

And I hope you didn’t spend too much time memorizing the list of countries in the Times story, because it’s going to change. With U.S. help, Kenya is about to get into the act. And, if Kenya can become part of this blindingly complex gravy train, a lot of other less developed countries – what investment managers call “frontier market” economies – will try.

I happen to be bullish on Africa, because of low stock prices and an almost unlimited supply of labor that, if not yet possessed of the needed skills, can acquire them in the next couple of decades. De Leus and Gijsels are more inclined to invest in South America because of energy abundance. Wherever they’re located, frontier markets should be of interest to investors – even if one has to invest in them indirectly, through companies in developed and emerging markets that do business in the frontier countries.

Multiglobalization: A summary

Despite the current trend away from globalization, largely motivated by national security considerations, De Leus and Gijsels believe that globalization in its many dimensions is here to stay. The price of autarky (each country trading only with itself) is unimaginably high, and if we move too far in that direction, we’ll feel the pain and stop. Thus, the authors conclude, we are not going to have a deglobalization depression. Globalization is good, and multipolar globalization is better: everybody deserves a chance.

But security issues have already started to modify the system of global trade. As this trend proceeds, there will be winners and losers. Investors should become aware of these changes as – or, better yet, before – they occur.

Conclusion: Good material, badly presented

The New World Economy in 5 Trends is an encyclopedia printed on the walls of a funhouse. (Obviously, I am straining to find a metaphor that captures the frustration of seeing so much good material badly presented.) Investors who want to understand the dynamics of the global real economy should skip the book and go directly to the book’s sources, which are in the endnotes. Most of their sources are publicly available. The authors have done their homework. Because they’ve revealed their background reading, they’ve made it easier for you to do yours. There is no substitute for doing your own research.

❦

Laurence B. Siegel is the Gary P. Brinson Director of Research at the CFA Institute Research Foundation, economist and futurist at Vintage Quants LLC, the author of Fewer, Richer, Greener: Prospects for Humanity in an Age of Abundance, and an independent consultant and speaker. His latest book, Unknown Knowns: On Economics, Investing, Progress, and Folly, contains many articles previously distributed by AJO Vista and predecessor firms, and a second collection of articles is in the printing stage. He may be reached at [email protected]. His website is http://www.larrysiegel.org.

The author thanks Kevin Coldiron (University of California, Berkeley) for his kind assistance.

1 De Leus is chief economist and Gujsels is chief strategy officer at BNP Paribas Fortis in Kapelle-op-den-Bos, Belgium.

2 To be a little more precise, the discount rate for risky future cash flows is the riskless rate (Treasury yield curve) plus a risk premium. But fluctuations in the riskless rate are critical to determining the overall risky discount rate.

3 https://www.amazon.com/History-Interest-Rates-Fourth-Finance/dp/0471732834

4 See their “Reviving America’s Forgotten Innovation System” in https://rpc.cfainstitute.org/en/research/foundation/2019/the-productivity-puzzle, edited by David Adler and me.

5 The Second Industrial Revolution (roughly 1870-1930) is the one that brought us automobiles, airplanes, telephones, radio, abundant energy from fossil fuels, and near-universal electric lighting and appliances. It is the foundation of modern life. Economists distinguish this period from the First Industrial Revolution a century earlier, typified by the steam engine, railroad, and so forth.

6 See my article describing Mark Mills’ views on materials and energy at https://www.advisorperspectives.com/articles/2024/06/24/realist-assesses-energy-transition-laurence-siegel.

7 I use https://capital10x.com/capital-10x-growth-navigator-the-commodity-hedge/ for the historical price (spot index) levels and compare it to the July 22, 2024 GSCI spot price of 556.89.

8 My 2015 Advisor Perspectives article, based on work by Stephen C. Sexauer and Bart van Ark, describes this process. The debt situation is worse than it was in 2015, so the remedy will be more painful, but the same principles apply now that did then.

9 See my book, Fewer, Richer, Greener (Wiley, 2019).

10 https://en.wikipedia.org/wiki/Fluid_and_crystallized_intelligence, accessed on July 19, 2024.

11 The source, https://www.csis.org/analysis/mapping-semiconductor-supply-chain-critical-role-indo-pacific-region, shows Sankey diagrams for total semiconductor manufacturing equipment and its three major components: wafer fabrication equipment, assembly equipment, and test equipment. I chose the diagram for assembly equipment because it has the most interesting trade dynamics.

12 See his book, which bears that title, at https://www.amazon.com/Multipolar-Globalization-Rethinking-Development-Nederveen/dp/1138232289/.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All