“If something cannot go on forever, it will stop.” – attributed to Herbert Stein

Is the world facing a public-debt crisis, or is too much debt just another headache we will muddle through? How can

investors distinguish between countries that are likely to default or otherwise injure debtholders, such as through

high inflation, and those that will resolve their debt problems and emerge stronger? How can countries deal

with high and rising levels of debt and return their finances to a sound footing?

In a recent article, “Dealing with Debt,”1 the husband-and-wife economic team of Carmen and

Vincent Reinhart, along with Kenneth Rogoff, carefully studied the dynamics of high levels of public debt, and how

governments have acted to reduce it. (Rogoff and Carmen Reinhart, who wrote the controversial and tremendously

valuable book This Time is Different, are Harvard professors, and Vincent Reinhart works at the American

Enterprise Institute.2)

Earlier, Stephen Sexauer, then at Allianz Global Investors, and Bart Van Ark of the Conference Board studied

strategies by which countries can reduce their debt levels through economic growth.3

This article summarizes the findings of both of these teams and concludes with suggestions for investors.

Don’t we owe the debt to ourselves?

First, a word of caution: debt is not harmless, even if it’s all domestic (“we owe it to ourselves”).

The U.S. has a lot of domestic debt, meaning that some Americans owe a lot of money to other Americans. The first

group is taxpayers and the second group is bondholders – savers, pension beneficiaries, and so forth. Some

people are in both groups but almost all are either net creditors (they are owed money) or net debtors (they have to

pay). If there is a debt default or a burst of inflation that amounts to a default, the creditors become losers and

the debtors become winners. These wins and losses affect wealth, spending, and investment in ways that slow growth

and often lead to a worse crisis.

You cannot ignore domestic debt!

If some of the debt is owed to foreign lenders (bondholders), the situation is made a little more complicated, but

not much. A default would increase domestic spending and decrease foreign spending, at least in the immediate run;

longer-run consequences are harder to assess. But debt owed to foreigners is not economically all that different

from debt owed to domestic bondholders.

Private debt is not harmless either. I worry less about private debt than about public debt because private

agents – households and corporations – are subject to market discipline and have to weigh the cost of

taking on debt against the benefit of holding the assets they use the debt to buy. (The 2008 mortgage fiasco shows

that this mechanism does not work perfectly, to say the least.)

Governments, in contrast, can use debt proceeds to buy votes, a process that does not instill confidence in the

quality of the decision to take on another unit of debt. But households have to service both piles of debt! They

have to pay their taxes and their private debts. So one must add private to public debt when calculating the overall

burden of debt in the economy.

When do governments increase their indebtedness? When do they reduce it, and how?

Reinhart, Reinhart, and Rogoff (henceforth “R3”) begin by observing that governments, at least in

advanced countries, do not typically tolerate high levels of debt (more than 90% or 100% of GDP) for

long.4 They run up debts during a war or depression and take steps to reduce the debt burden once the

crisis is resolved. The R3 data are extensive and meticulously assembled, but the authors offer no economic theory

as to why 90% or 100% is the cutoff. These levels have been suggested as a rule of thumb indicating the debt burden

is so high that steps need to be taken, sometimes rapidly, to avoid a collapse and some form of default, but the

real danger point depends on the specifics of each case.

R3 classify the steps taken to reduce debt into “orthodox” and “heterodox” categories.

Orthodox steps include the “Boy Scout” method of raising economic growth rates above nominal interest

rates, so that the debt burden reduces on its own. Of course, governments don’t fully control the growth rate,

or we would all be rich. Limits to growth are set by the speed of innovation, the cost of inputs and competition

from other countries. Governments can, however, maintain control of their own outlays such that the nominal growth

rates are positive but below those of GDP and tax revenue. Sexauer and Van Ark show that this always works,

mathematically, to decrease the debt-to-GDP ratio. Other orthodox methods are “austerity” (reductions in

government spending) and selling government assets; this approach has a mixed track record (think

Greece).5

“Heterodox” ways of reducing debt

Heterodox methods include defaulting on or restructuring the debt, creating unexpected inflation, taxing wealth

and “financial repression” (negative real interest rates, amounting to a tax on savers). R3 find that,

in past recoveries from high debt levels, governments have used these unpleasant methods more often than one might

think.

For example, the massive World War II debt of the U.S. and U.K. was paid off in dollars and pounds that were

radically devalued (through inflation), to the point that U.S. Treasury bonds, so beloved by investors today, were

called “certificates of confiscation” not that long ago. The wealth destruction in the U.K. in the

1970s, caused by unexpected inflation, negative real interest rates and collapsing stock prices, was worse in that

country than in the Great Depression. While the 1970s are quite a while after the war, many economists trace the

Great Inflation of that era to the U.S. and U.K. governments’ need to pay back the war debts of a generation

earlier in cheaper dollars and pounds.

Financial repression: Today’s preferred debt reduction approach

Bondholders (savers) don’t like their wealth decimated by inflation, and they vote.6 Moreover,

inflation hurts a lot of people, not just savers. So governments recently have sought another, more palatable

solution. If you can’t get away with not paying principal (in real terms), don’t pay interest!

Today’s rock-bottom interest rates are a wealth transfer from U.S. saving depositors to debtors at the rate of

hundreds of billions of dollars every year. These low rates are tolerated partly because inflation is low, but

savers who are invested in money-market funds and other cash instruments are losing between 1% and 3% of their real

wealth every year. That’s quite a wealth tax. Economists, following McKinnon (1973) and Shaw (1973), call a

policy of persistently and intentionally negative real interest rates “financial repression,” and that

feels right.7

Principal and interest are, at least conceptually, interchangeable. A perpetual bond that never pays any interest is

just as worthless as one that defaults (fails to pay principal). This is, of course, just an illustrative example.

Today’s long-term bonds do pay a little interest. But it’s still financial repression.

The Boy Scout way: Work off the debt

Borrowing money and not paying it back, explicitly or through a subterfuge, is a neat trick if you only care about

enriching the government. But governments are supposed to serve the people, meaning taxpayers and savers as well as

the beneficiaries of government spending. (Often, they’re the same people; everyone benefits in some way from

government spending, while almost everyone becomes a saver at some point in his or her life.)

Taking this view as a starting point, Sexauer and Van Ark show how governments can “work off” their

debts, paying them down without relying on the heterodox strategies documented by R3. This Boy Scout, good guy

approach preserves the government’s legitimacy and its ability to borrow again at favorable rates in case of

another crisis.

The authors recognize the basic math of public finance: Public debt as a percentage of GDP will not grow if nominal

GDP growth in dollars exceeds interest payments on government debt plus any budget deficit. When these conditions

are violated, debt-to-GDP and interest rates can increase rapidly.

They offer three key insights for resolving the unfolding crisis: (1) What matters most is the power of the

compounding relative growth rates where government still grows, but grows less than GDP (and tax revenues); (2) a

powerful policy rule is to increase government spending at the growth rate of population plus inflation –

a “no one worse off” policy; and (3), of all the policies a government can pursue – from default

to austerity to inflation – it is productivity-enhancing policies that have the biggest payoff. These policies

will take time to work, but the evidence is that once the market sees productivity-led growth accelerate and

government spending increase less than revenues, the bond markets will continue to offer low rates and the crisis

will gradually disappear.

Sexauer and Van Ark note that, once the difficult first steps are undertaken, debt repayment tends to accelerate,

like a mortgage that is hard to pay down at first but later becomes easy as one’s income rises and principal

becomes an ever-increasing part of the mortgage payment. They write:

[O]n average, no absolute cuts in government spending per person are required, although reallocations and

redistributions remain important policy choices. The annual flow of productivity-driven GDP above the combined

growth of population and inflation can be allocated to debt and tax reduction or more investment in

productivity-enhancing measures that strengthen a “virtuous” feedback loop. The bond markets will

see this and will stay open at reasonable interest rates.

The authors make the case that, to reduce the debt-to-GDP ratio, nominal government spending does not have to be

cut; it just has to grow more slowly than the economy grows in nominal terms. This is good news because cutting

nominal government spending is almost impossible, but cuts in its rate of growth have been achieved in many

different countries and circumstances. Still, some government spending is frankly wasteful or creates disincentives

to produce.8 These kinds of spending can be cut, and may only be able to be cut in a crisis. “Don’t

let a good crisis go to waste.”9

During long periods of fiscal adjustment, it is also good news that much of productivity growth comes from policies

that change incentives and do not require large government outlays. For example, in 1980, the Staggers Act

deregulated U.S. air, rail and ground transportation and unleashed a 35-year run of productivity-led growth and

environmental improvements. U.S. freight railroads are now the most productive in the world and have attracted such

astute investors as Warren Buffett (Burlington Northern Santa Fe). The gain in efficiency has also been very green:

energy use per freight mile is down 65%, saving 6 billion gallons of fuel per year.10

A lesson learned from Canada and Sweden

A scheme for paying off the public debt without cutting spending, then, is attractive indeed – but is it

realistic?

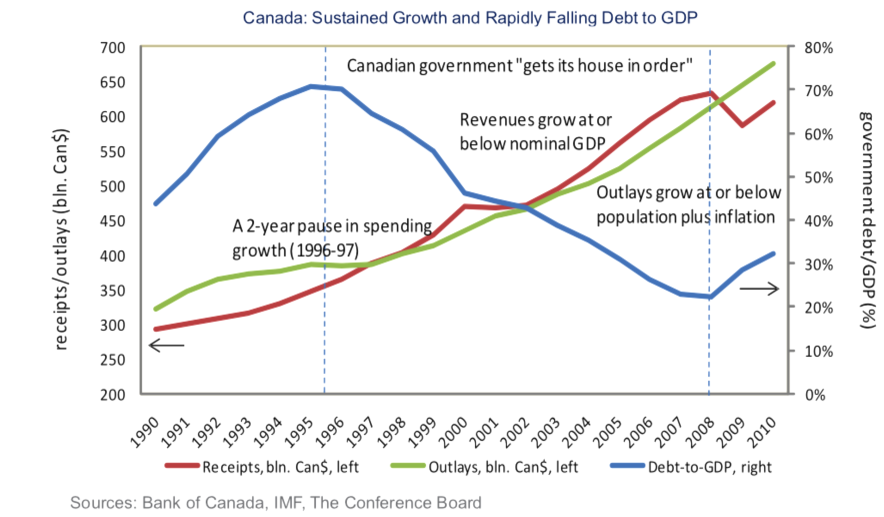

Sexauer and Van Ark argue that it is, with Canada and Sweden having achieved just that in the recent past and the

U.S. and the U.K. in the more distant past. Exhibit 1 shows the Canadian example. In the mid-1990s, Canadian public

debt reached 70% of GDP, a shocking number for a prosperous peacetime economy with no financial crisis. The first

crisis management step was the most important one: The Canadian government resolved to first get its fiscal house in

order. There was a two-year pause in the growth of nominal government spending, something that has also been

achieved in the U.S. recently (over 2011-2015). The second step was a determination to grow government spending at

or below the growth rate of population plus inflation (that is, to keep real per capita spending flat or

declining), and to do so with the goal of fairness.

The Canadian results were spectacular. The debt-to-GDP ratio fell from 70% to just over 20% in 13 years! Such is the

power of compounding small differentials in growth rates. As a result, when the 2008 recession hit, there was more

than enough borrowing capacity. Debt-to-GDP falls quickly under these circumstances because GDP is rising while debt

is falling; the ratio is hammered from both ends.

Applying the Canadian lesson to the U.S.

OK, why not here? Some readers may argue that Canada is a special case, a small country with not much of an

underclass to support and with mammoth energy reserves. But the U.S. has some advantages that Canada does not: a

diversified economy with particular strength in technology, a reserve currency and a higher education system that

attracts the world’s young elite (if we can keep them). Moreover, the U.S. debt-to-GDP ratio also fell during

the late 1990s boom years, although less dramatically than Canada; the U.S. trimmed its ratio by about 10 percentage

points.

In fact, this trend is underway in the U.S. We have already experienced a sequestration-driven pause in the growth

of (not cuts in) government outlays, and tax revenues are growing faster than expenditures.

The lesson of the Sexauer-Van Ark study is that economic growth covers a lot of sins. We do not know, for certain,

how to stimulate rapid growth through policy. The best policies create incentives to invest and innovate, increase

our working population (this includes our long history of accepting immigrants of all talents) and grow the money

supply at a relatively constant rate. In addition, it’s important to keep taxes simple and at a practical

minimum, and to encourage free trade.11

Implications for investors

This, too, shall pass. The resolution of the current public-debt crisis will in all likelihood be just like the

prior crises. There will be various forms of restructuring with big winners, big losers and many muddle-through

companies. Then growth will return. All the rules of smart investing will still hold: indexing, value investing,

buying and holding for the long run. This time is not different.

Will there be a prolonged 25-year Japan-like stupor? Japan’s lost decades occurred because it never got its

fiscal house in order and its productivity growth fell to an anemic 1% per year. The odds of this kind of stupor

unfolding globally are low, especially in the U.S., much of the rest of the West and many of the emerging markets.

The evidence is that the future will bring, not stagnation, but more reform and more growth (see my Advisor

Perspectives article, Two Top

Experts Debate the Outlook for Growth). Billions of smartphone users can now see how others live. They will

not stay idle or docile.

What good are low interest rates?

Managed interest rates, or financial repression, create winners and losers on a global scale. They also increase the

chances for the next crisis as the imbalances grow year after year.

Investors should be wary of any central-bank strategy that depends on a Phillips curve, the purported relation

between inflation and unemployment. The Phillips curve holds that an increase in inflation is stimulative. If this

relation works at all, it is only in the short run; in the longer run, the extra inflation causes lenders to demand

higher interest rates, restraining economic activity instead of stimulating it. In The Tooth Fairy Economics of Jeff

Madrick, I showed that the Phillips curve is radically unstable over time; policymakers cannot possibly rely

on it.

Yet that is what central banks seem to be doing – although they won’t acknowledge it. The regime of

rock-bottom interest rates is said to be good for us because low lending rates stimulate the economy, although it’s

hard to see how they do so unless (1) the low rates lead to unexpected inflation and (2) the inflation is

stimulative through the agency of a Phillips curve, an unlikely outcome.12

Meanwhile, low interest rates hurt the economy by lowering the income of savers. It is as though the lost income and

spending of savers doesn’t count. It’s not clear which is stronger, the stimulating effect of low

borrowing costs or the chilling effect of a large and covert tax on savers. Beyond a point that we have almost

certainly passed, the stimulating effect of low borrowing costs will peter out (as all profitable projects become

funded) and the chilling effect becomes dominant.

So, low rates are mostly helpful to governments, by minimizing their borrowing and debt-refinancing costs through a

savings tax. Investors should favor countries where low rates are actually being used to reduce debt, rather than to

take on more of it. Someday there will be another crisis, and countries with low debt will be tremendously

advantaged.

Bonds

In normal times, investors seek out bond markets where interest rates are expected to move from high to low,

producing capital gains; if the rates don’t decline, at least you get a high current yield. Countries that are

getting out of debt are favored in this strategy. In today’s world, however, we have extremely low rates even

in highly indebted countries, unless the country is really a basket case (Greece, Argentina); even Spanish and

Italian interest rates are below those of the U.S., despite having more public debt.13 In this

environment it probably pays to wait until rates normalize somewhat,14 and then to invest in countries

with less debt, because the bonds are safer and the economies have more headroom for growth; the U.S. is

the best example.

Stocks

There isn’t much of a correlation between the finances of a country’s government and the performance of

the stocks headquartered in that country. As a general rule (with many exceptions), companies are already domiciled

where they think they’ll be regulated and taxed fairly, and where their target markets are located. A

sovereign debt restructuring, including default, distributes the losses between the government, its lenders and the

bailout agent. Such an action is typically followed by higher growth, so except for companies tightly linked to

domestic spending, look for companies with strong global growth prospects and attractive valuations, even if they’re

located in countries with stressed public finances. Governments know they are competing for corporate tax dollars,

so taxation of mobile, shareholder-focused companies tends not to get out of hand.

To sum up, most countries have not passed any sort of tipping point where an ever-increasing debt-to-GDP ratio

becomes a self-fulfilling prophecy. A high level of public debt can be reduced through fiscal prudence and

pro-growth economic policies.

Read more articles by Laurence Siegel