In markets and economics, you sometimes have to hold two thoughts in your head simultaneously — an important lesson on a day in which the US unemployment rate unexpectedly surged to its highest in nearly three years.

First, the labor market probably isn’t quite as imperiled as the main figure suggests. Second, the speed at which it’s cooling ratchets up the risks, and Federal Reserve policymakers should at least entertain the possibility that they’ll need to cut rates by 0.5 percentage point when they meet next in September.

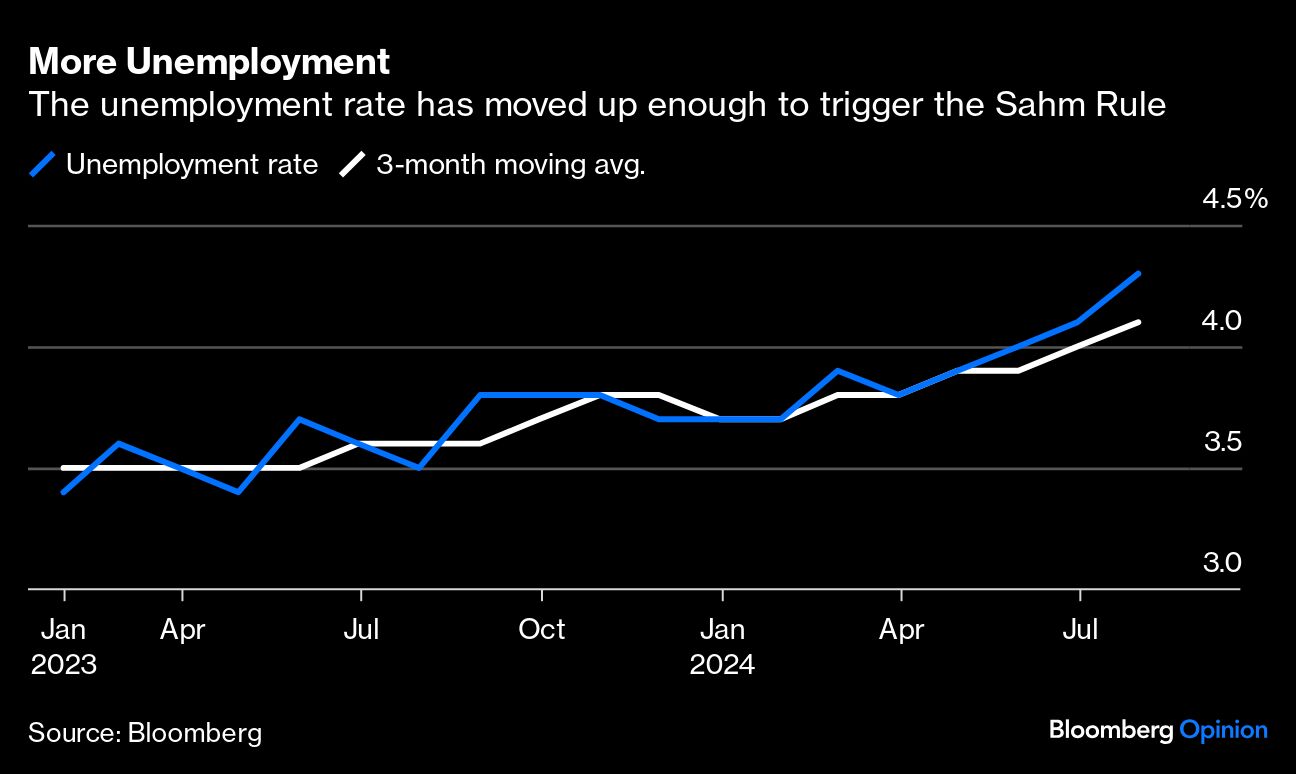

A report Friday showed that the unemployment rate rose to 4.3% in July from 4.1% the previous month, exceeding all 69 estimates from economists surveyed by Bloomberg. That’s still relatively low, but what’s obviously concerning is the speed with which it has risen in the past four months. A rule developed by my Bloomberg Opinion colleague Claudia Sahm shows that historically, the economy is already in a recession once the three-month average of the unemployment rate rises at least a half percentage point above its low in the past 12 months. That’s now happened.

The labor market cooldown is occurring at a pace that has to leave policymakers — who meet to decide on monetary policy only eight times a year — uncertain as to where things will stand when they convene again September 17-18, after they decided to forgo an opportunity to cut interest rates earlier this week. Nonfarm payrolls still rose by 114,000 last month, but jobs need to grow by a modest amount just to keep pace with population and labor force growth. The payrolls figure was down from a revised 179,000 a month earlier and only one of the 74 prognosticators surveyed by Bloomberg expected the pace to step down that swiftly.

In a world in which labor market weakness tends to snowball, Fed policymakers surely must be on high alert after Friday’s statistics. Even modest upticks in unemployment can lead to reduced consumption, which can lead to weakness elsewhere in the economy. That’s in part the intuition of the Sahm Rule, and it demands that policymakers always act in a forward-looking manner.

Having said all that, there’s probably some overreaction in the market following the report. The S&P 500 Index was down 2.5% at the time of writing, and the yield on 10-year Treasury notes dropped 16 basis points to 3.82% and earlier touched the lowest level since December 2023. Those are pre-recessionary market dynamics, and there’s nothing in Friday’s numbers that would come close to confirming a downturn. After all, let’s keep things in context: Gross domestic product grew at a fantastic annualized pace of 2.8% in the second quarter.

Additionally, there are — as always — plenty of conflicting narratives and sources of potential noise under the surface in the labor market data itself.

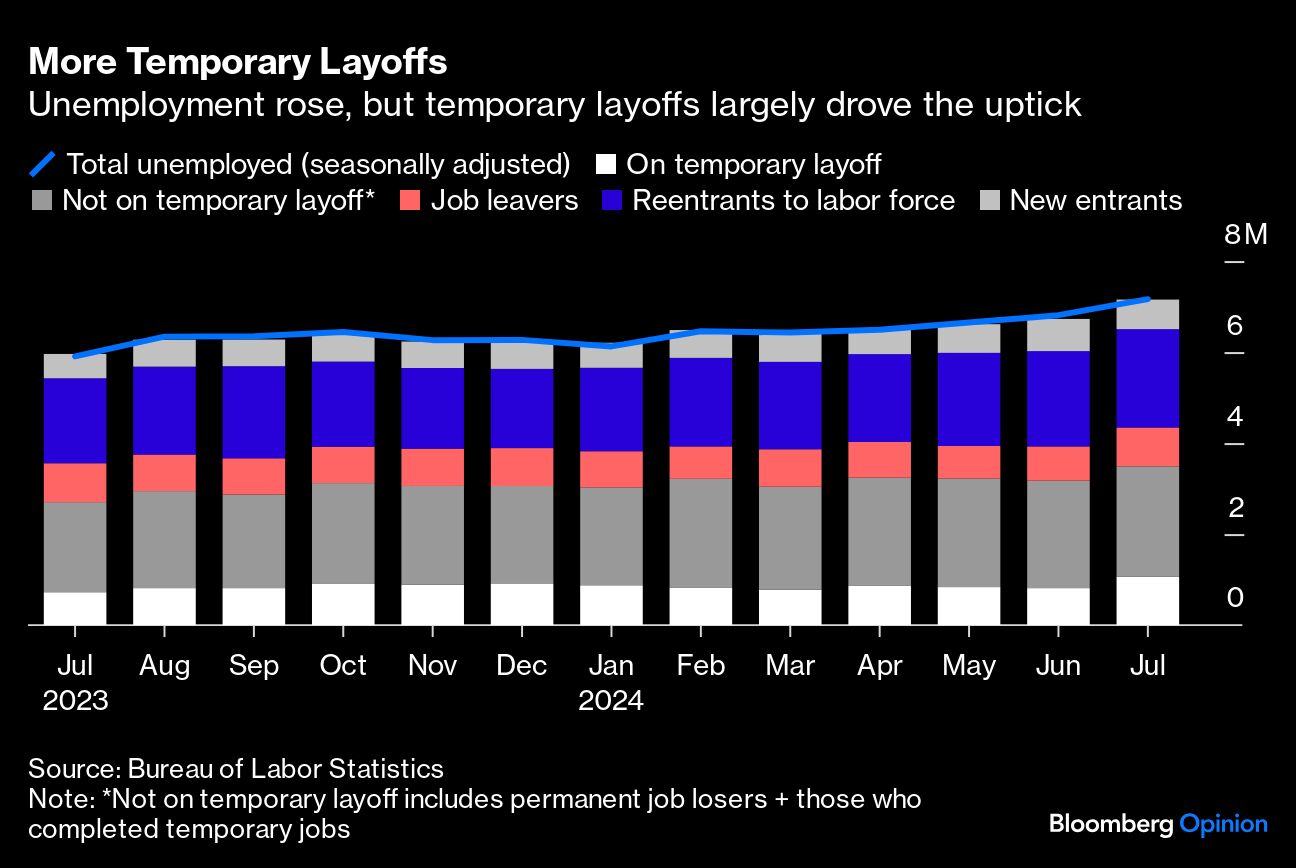

The weak data comes at a time when Hurricane Beryl struck Texas during the reference period. In its report, the Bureau of Labor Statistics wrote that it had “no discernible effect” on the data, but there was a large increase in the number of people reporting that they didn’t work due to bad weather, as Bloomberg News’s Augusta Saraiva reported. There was also a large increase in temporary layoffs but less movement in permanent layoffs, as Burning Glass Institute Director of Economic Research Guy Berger pointed out on X. Given the hurricane impact, that seems like an important point. In previous months, the uptick in unemployment had come from an increase in labor supply (labor market entrants and reentrants increase the denominator of the unemployment rate.)

As for the Sahm Rule, even Claudia herself has repeatedly emphasized that it’s not a law of nature and that this time could be different. “That comes off of historical experience; that doesn’t necessarily tell us where we are right at this moment,” she told Bloomberg Radio’s Tom Keene and Damian Sassower on Friday. Still, she was concerned about “way too much momentum in the unemployment rate.”

Personally, I had been pounding the table (here and here) for a rate cut earlier this week, much like my Bloomberg Opinion colleague Bill Dudley, the president of the Federal Reserve Bank of New York from 2009 to 2018. Even though I didn’t see an imminent downturn, I simply thought it was the better risk-management move. Having missed that opportunity, policymakers may have to hurry to ease rates when they meet again in September if further data confirms the recent trend.

Despite their inaction this week, policymakers are clearly aware of the risks and just needed a bit more convincing. In his press conference, Fed Chair Jerome Powell was asked explicitly, by Jean Yung of MNI Market News, about the possibility of a 50-basis-point cut. Although he reflexively pushed back at the notion, he wisely edited himself in real time to leave the door open. “I don’t want to be really specific about what we’re going to do, but that’s not something we’re thinking about right now,” he said, before adding: “Of course, we haven’t made any decisions at all as of today.”

Nor is it likely that they have made any decisions after Friday’s jobs report. But fortunately, they have a lot of monetary policy firepower at their disposal with rates at a two-decade high of 5.25%-5.5%. They should be prepared to use it.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin