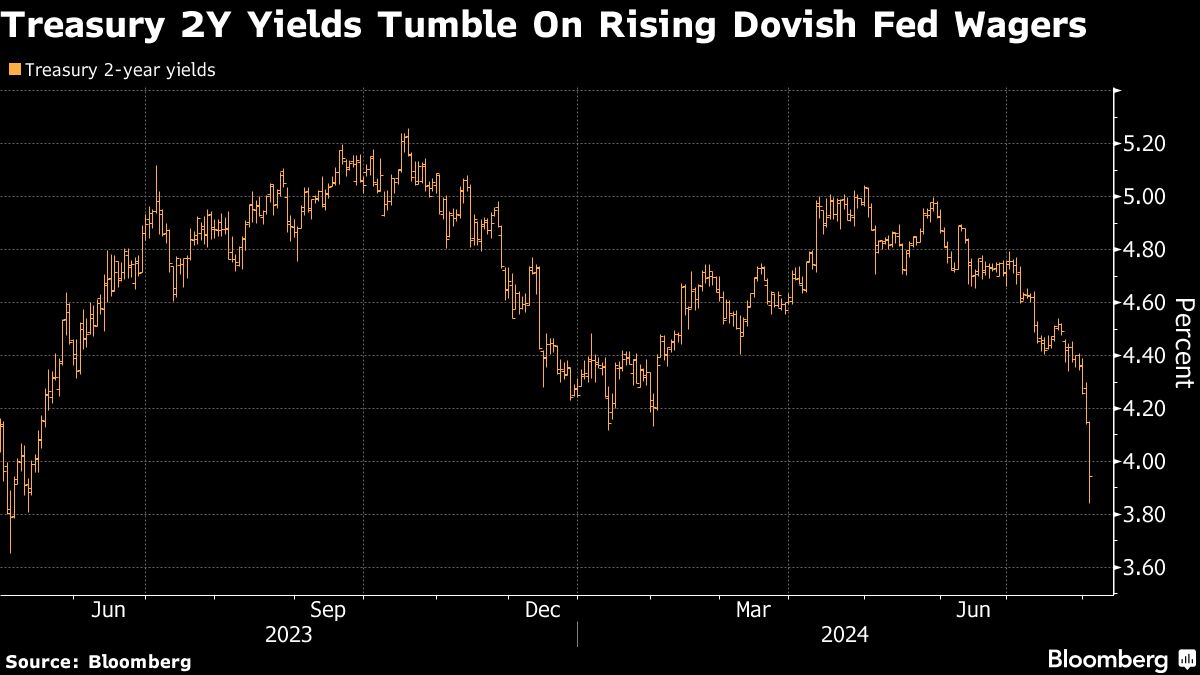

The bond-market rally escalated Friday after a report showed that job growth slowed sharply last month, further stoking speculation that the Federal Reserve will start aggressively cutting interest rates to keep the economy from stalling.

The policy-sensitive two-year Treasury yield tumbled as much as 31 basis points to 3.84%, the lowest since May 2023, before paring the drop. Rates on Treasuries of all maturities declined, with the benchmark 10-year yield sliding to about 3.86%.

The employment figures — which showed job growth slowed to 114,000, nearly half what it was a month earlier — kindled concerns that the US economy is at risk of a moving toward a recession.

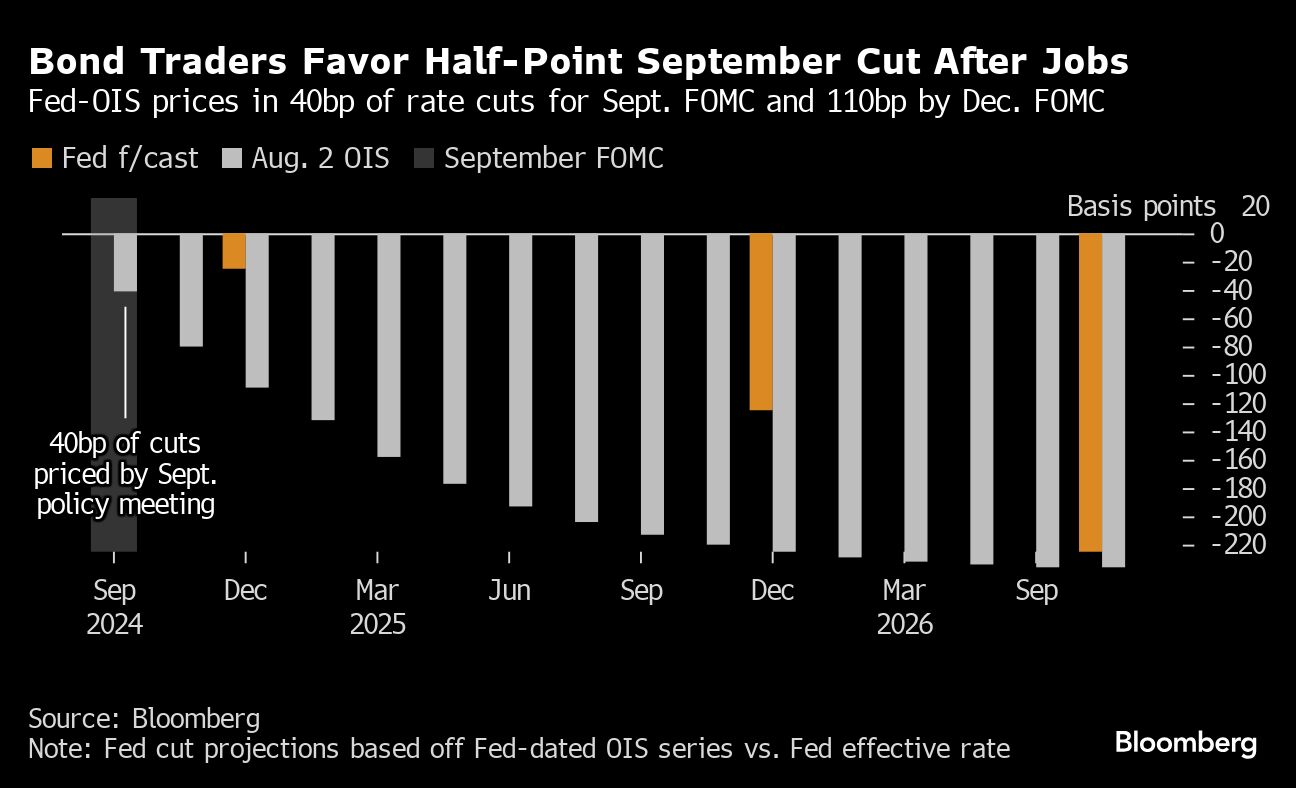

That drove futures traders to price in expectations that the US central bank will cut its benchmark rate by a full percentage point by the end of the year. With just three meetings left, that shows anticipation that the Fed would make an unusually large half-point move at one of the gatherings or act between its scheduled meetings — signaling that policymakers will start moving rapidly to bolster growth.

“The market is starting to think the Fed is too late in cutting rates,” said Tony Farren, managing director in rates sales and trading at Mischler Financial Group.

The sharp recalibration came after the Fed kept its rate at a more than two-decade high at its meeting this week. While Fed Chair Jerome Powell telegraphed that the central bank may ease policy at its next meeting, a rise in unemployment claims, weak manufacturing data and now the jobs data are spooking investors by sowing concern it has waited too long.

The shift in pricing “reflects investors’ growing concern that the FOMC might need to cut rates more quickly than the 25-basis-point quarterly cadence as economic headwinds continue to mount,” said Ian Lyngen, head of US rates strategy at BMO Capital Markets.

Powell repeated on Wednesday that the Fed is relying on the incoming data when setting policy and emphasized that policymakers are mindful of the risks of waiting too long.

“The soft landing narrative is now shifting to worries about a hard landing, and the market is increasing the odds that the Fed will have to make a 50 basis point cut in September,” said Lara Castleton, head of US portfolio construction and strategy at Janus Henderson Investors.

Ahead of the meeting, former New York Fed President William Dudley and Mohamed El-Erian warned that the Fed was at risk of erring by holding rates too high for too long. Both were writing as Bloomberg Opinion columnists.

That view has since started to take hold. A $12 million wager in options linked to the Secured Overnight Financing Rate, which closely tracks Fed policy expectations, is targeting some 225 basis points of easing by the middle of 2025.

What Bloomberg strategists say...

“It looks like the market is jumping the gun on a recession that, if it does occur, is more likely to happen next year at the earliest.

The Sahm Rule has been triggered, no doubt fueling some recession angst. But as noted earlier, not only does it lag recessions and miss most of the equity downturn, it is neither a necessary nor sufficient condition for a recession. Moreover, today’s rise in unemployment was mainly driven by a rise in the participation rate.

— Simon White, rates strategist. Read more on MLIV.

Bond traders have repeatedly jumped the gun when it comes to pricing in rate cuts from the Fed, however, only to be caught offsides when the economy continued to exhibit surprising strength. That happened late last year, when traders expected rate cuts to start early this year.

“The reaction here is probably the right reaction,” Jeffrey Rosenberg, portfolio manager at BlackRock Inc. said on Bloomberg Television with regard to the fall in yields. “Maybe it’s a bit of an overreaction but you are going to push on changing the trajectory from maintenance cuts to calibration cuts to policy need to move a bit faster. The market wants to push for for the fifty” basis point Fed rate cut.

Inflation-protected bonds lagged the broader Treasury market, reflecting eroded expectations for inflation. For the five-year tenor, the gap between the inflation-protected yields and typical Treasuries shrank to less than 2% for the first time since 2020. The gap represents the average expected inflation rate over the next five years.

Fixed-income markets elsewhere were caught up in the frenzy, as money markets wagered on further interest-rate cuts from the European Central Bank and Bank of England.

German two-year yields — among the most sensitive to changes in monetary policy — tumbled, extending the streak of declines to the longest in three years. In the UK, the bond curve continued to steepen, with 10-year yields exceeding their two-year peers by the most since 2022. They ended a more than year-long inversion last month.

“Worries are definitely building that the Fed would have to take a faster calibration path to lower rates,” said Eugene Leow, a Singapore-based senior rates strategist at DBS Group Holdings.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liz Capo McCormick