Economists Stephen Miran and Nouriel Roubini are making waves by suggesting in a paper published last week that the Treasury Department has actively engineered easier financial conditions by increasing the issuance of short-term bills and, consequently, reducing the share of longer-term notes and bonds, thereby keeping yields lower than they would otherwise be. The paper suggests that this amounts to a form of “stealth quantitative easing,” working at cross-purposes with the Federal Reserve’s inflation-fighting efforts and supporting the economy in an election year.

Got that?

If you buy that reasoning, you’ll probably love the thesis even more after the latest developments. In its quarterly statement on Wednesday, the US Treasury said it was leaving its issuance of longer-term debt unchanged. It also said that it wouldn’t increase the issuance of notes and bonds for “several quarters,” despite concerns of an uptick in longer-dated securities to help finance the yawning federal budget deficit, as Bloomberg News’s Liz Capo McCormick reported. That fresh forward guidance lifted a veil of uncertainty in the market, and yields on 10-year Treasury notes touched the lowest since March, and a host of important borrowing costs — for mortgages and corporate bonds — looked poised to follow suit. (It should be noted that the Federal Reserve’s hints of rate cuts later this year also helped bond performance Wednesday.)

But is this really manipulation for political purposes, or “Activist Treasury Issuance,” as Miran and Roubini dub it in their paper? Or is the increase in bill issuance part and parcel of Treasury’s long-running goal of financing the government at the “lowest cost to the taxpayer over time”? Treasury Secretary Janet Yellen has already shot back in an interview with Bloomberg News, saying that Treasury wasn’t trying to ease financial conditions. “I can assure you 100% that there is no such strategy. We have never, ever discussed anything of the sort,” she said.

I’m with Yellen on this one.

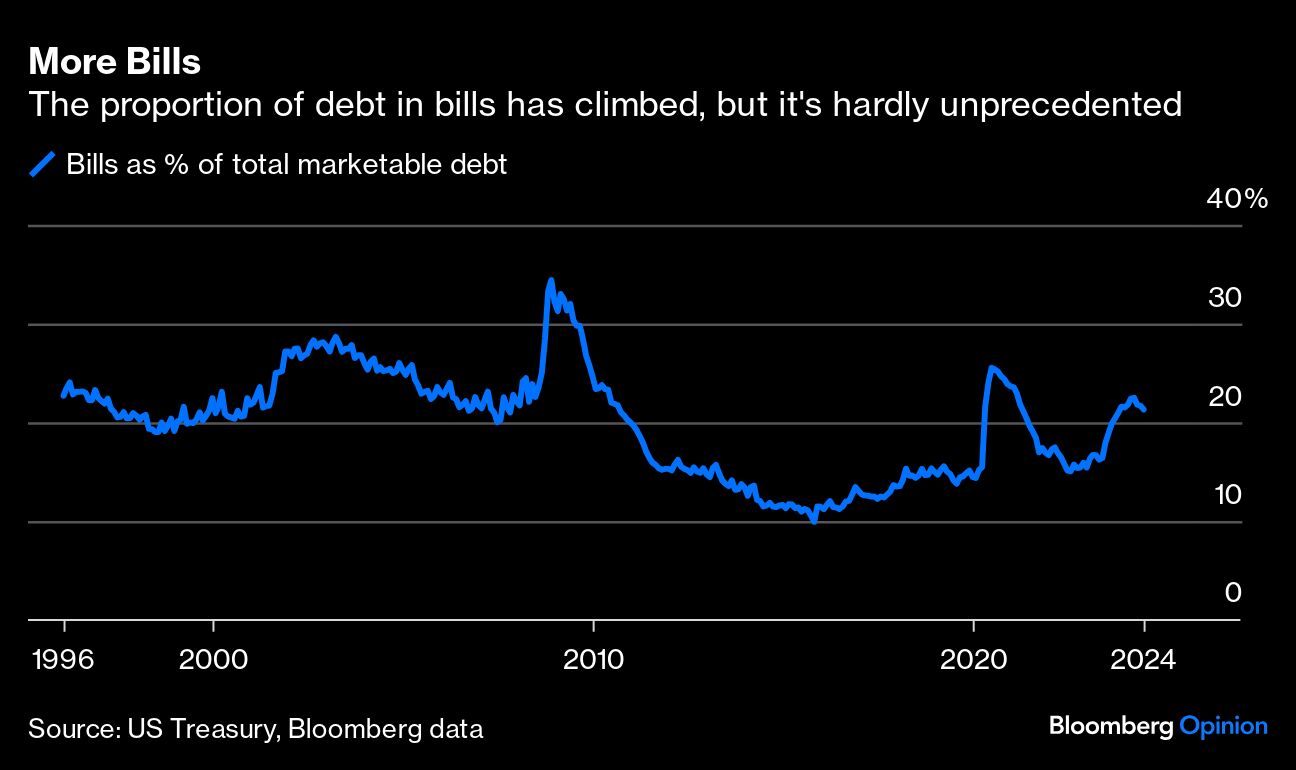

In some ways, the US government is just like any other borrower. When rates go up, borrowers pull back to wait for them to come back down. That’s effectively what’s happened since 2022 across corporate bonds and mortgages. If entities must borrow, they prefer to do so on a short-term basis rather than lock in high rates for years or decades. That’s just good financial sense, and it often pays off. At the government level, this has caused the bill share of marketable Treasuries to drift higher, but it’s hardly unprecedented even in relatively recent times.

The government isn’t entirely like a household, of course, in that its borrowing decisions reverberate throughout the market and can have a significant influence on the cost of borrowing at various maturities. It aims to be “regular and predictable” in its issuance because policymakers know that uncertainty and volatility can lead investors to demand higher risk premia over the medium and long run.

Still, it makes total sense that Treasury would wait to lock in borrowing costs when policy rates are high and widely expected to fall in the near future, so long as they act within the scope of what markets expect. The prospect of falling rates isn’t some wild speculative assumption either; it’s the consensus thinking among market economists and many of the people who give advice to the Treasury from the Treasury Borrowing Advisory Committee, a collection of banks, broker-dealers, asset managers and other advisers that meets with the government quarterly.

In the Federal Reserve Bank of New York’s survey of primary dealers, the median respondent expects the fed funds rate to average 3.38% over the next decade. By contrast, the fed funds target range sits at a two-decade high of 5.25%-5.5%, and the 10-year yield has averaged 4.32% over the past year.

I’ve been thinking about this issue since Strategas’s head of fixed income Tom Tzitzouris made a similar argument as Miran and Roubini during a recent Bloomberg Opinion broadcast. I disagreed with the implied conspiracy theory then as I do now. But ultimately, our debate seemed to come down to a difference of opinion on the path of inflation. If you believe (as Tom did at the time), that inflation remained a serious longer-term threat, you might believe that Treasury had been reckless in waiting to take its medicine by delaying the issuance of longer-term maturities. If you believe (as I do) that inflation is close to being licked, then the rationale for waiting is obvious.

There’s room for reasonable people to debate the ultimate consequences of the policy on this basis. The Miran-Roubini paper makes a relatively undeniable case that the amount of bill issuance is relatively unique in history; that it has a market and economic impact; and that its reverberations will continue to be felt. But I can’t get behind the suggestion of malicious intent where there’s no evidence of it.

Ernie Tedeschi, former chief economist at the White House Council of Economic Advisers and current director of economics at the Yale Budget Lab, put it well: “This is neither malicious nor unprecedented in magnitude,” he wrote on X. “This is exactly the strategy a fiscal agent might take to save taxpayers some money if they expected interest rates to fall soon.”

Nevertheless, I’m still paying attention to the debate and you should, too. It’s reasonable to assume that this period of proportionally low note and bond issuance will have to be followed, at some point, by a period of proportionally higher issuance, even if by some miracle the government gets the deficit under control. When that happens, the term premia may increase, putting a floor under longer-term bond yields, even in an environment of benign inflation and falling policy rates.

You might say that all of this falls under the “long and variable lags” of monetary policy described by Milton Friedman, and it’s important to keep that on our collective radars whether we’re trading government securities or financing a household. What’s clear to me, however, is that none of this is fundamentally political. Conspiracy theories that suggest otherwise won’t help anyone navigate the complicated economic and market dynamics that lie ahead.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin