US Plans to Hold Note, Bond Sales Steady for ‘Several Quarters’

The US Treasury left its quarterly issuance of longer-term debt unchanged for the second straight time, and maintained its guidance that it doesn’t expect to need increasing issuance of notes and bonds for “several quarters.”

The Treasury Department said in a statement Wednesday it will sell $125 billion of securities at its so-called quarterly refunding auctions next week, which span 3-, 10- and 30-year maturities. Dealers had widely predicted that outcome, seeing the department as able to make up any funding shortfalls over the period via more bill sales.

A number of market participants had seen some risk that the Treasury would revise its guidance to incorporate the potential for increasing issuance of longer-dated securities, given the outsize federal budget deficit. But the department reiterated its May language.

“Based on current projected borrowing needs, Treasury does not anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters,” the statement said. FRNs are floating-rate notes.

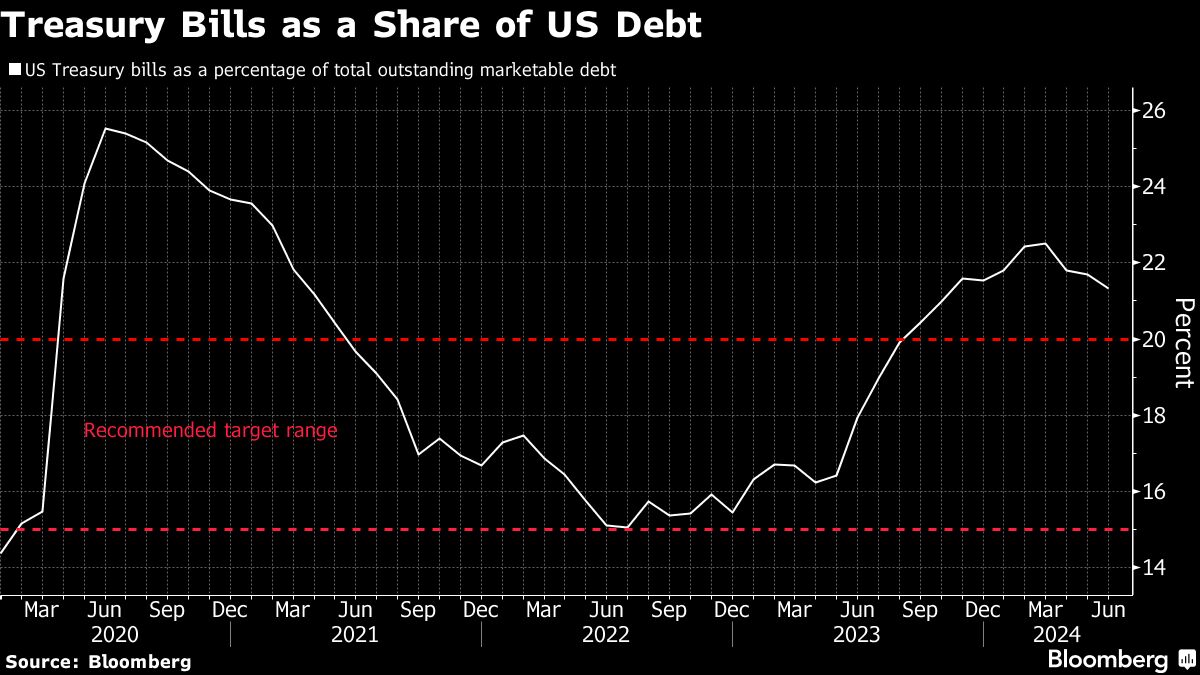

Separately, officials asked the Treasury Borrowing Advisory Committee — an outside panel of dealers and other market participants that counsels the department — to take another look at the recommended share of bills, which mature in up to a year, as a total of marketable debt. TBAC had previously recommended a 15% to 20% range.

“Most” TBAC members this time indicated that averaging around 20% over time was a good tradeoff between interest-rate costs, volatility in financing and the risk of rolling over a major amount of debt at one time, the panel said in a separate report.

With the Federal Reserve now having reduced the amount of Treasuries it’s letting mature each month without replacement, that has in turn eased the burden on the Treasury to sell more debt to the public to fund the fiscal deficit.

Later Wednesday, the Fed is widely expected to signal it will start lowering interest rates, offering further relief for the Treasury by reducing the government’s debt-servicing bill. The pace of so-called quantitative tightening — the amount the central bank is shrinking its balance sheet, is seen staying at the current amount of up to $25 billion a month for Treasuries.

The Fed’s decision is due at 2 p.m. in Washington.

As for next week’s refunding auctions, the $125 billion will be made up of the following:

- $58 billion of 3-year notes on Aug. 6

- $42 billion of 10-year notes on Aug. 7

- $25 billion of 30-year bonds on Aug. 8

The refunding will raise new cash of about $14 billion.

Many dealers have said over recent weeks that the Treasury will eventually have to bump note and bond sales higher again given the fiscal outlook. The US is on track to run its largest federal deficit outside of crisis times. Marketable Treasury debt outstanding has already grown to $27 trillion from about $12 trillion a decade ago.