When the Federal Reserve signals the likely path of monetary policy to investors this week, including an anticipated start to interest rate cuts in September, it can no longer be complacent about the labor market.

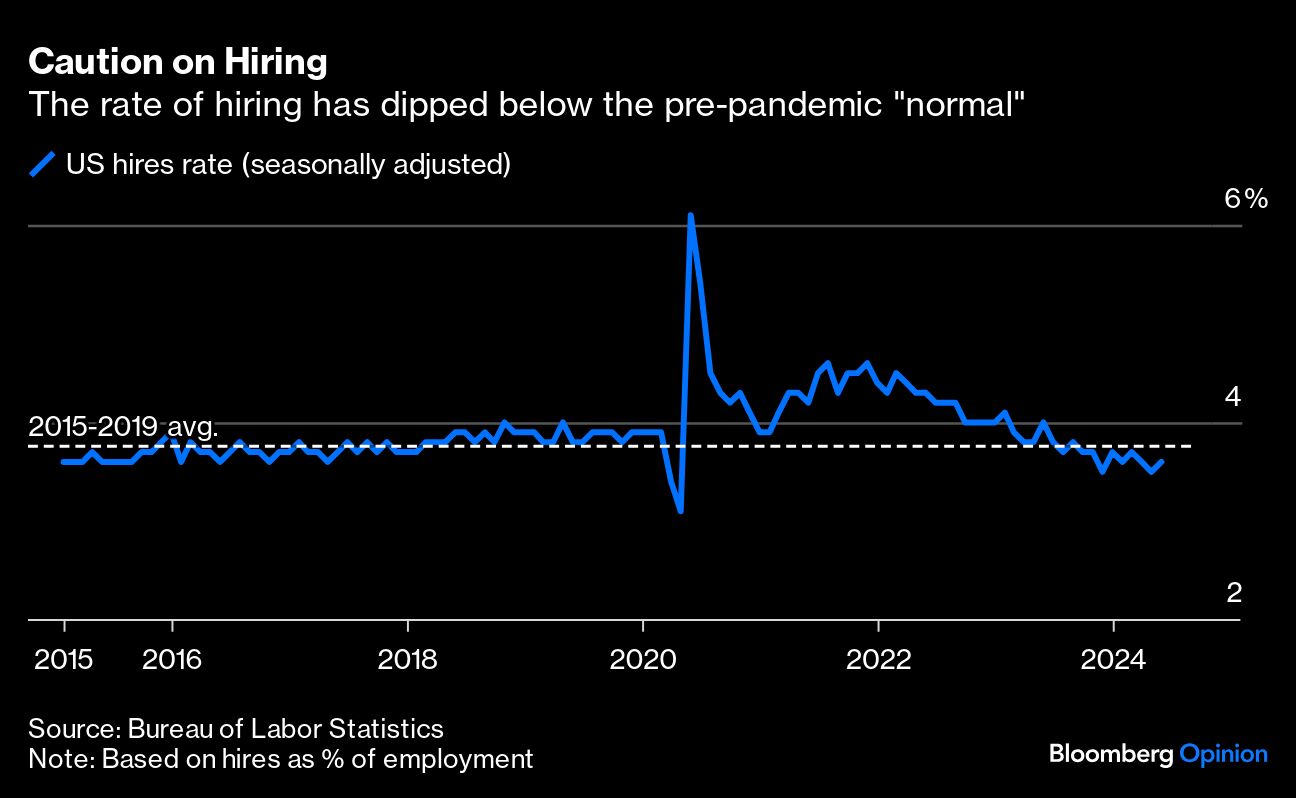

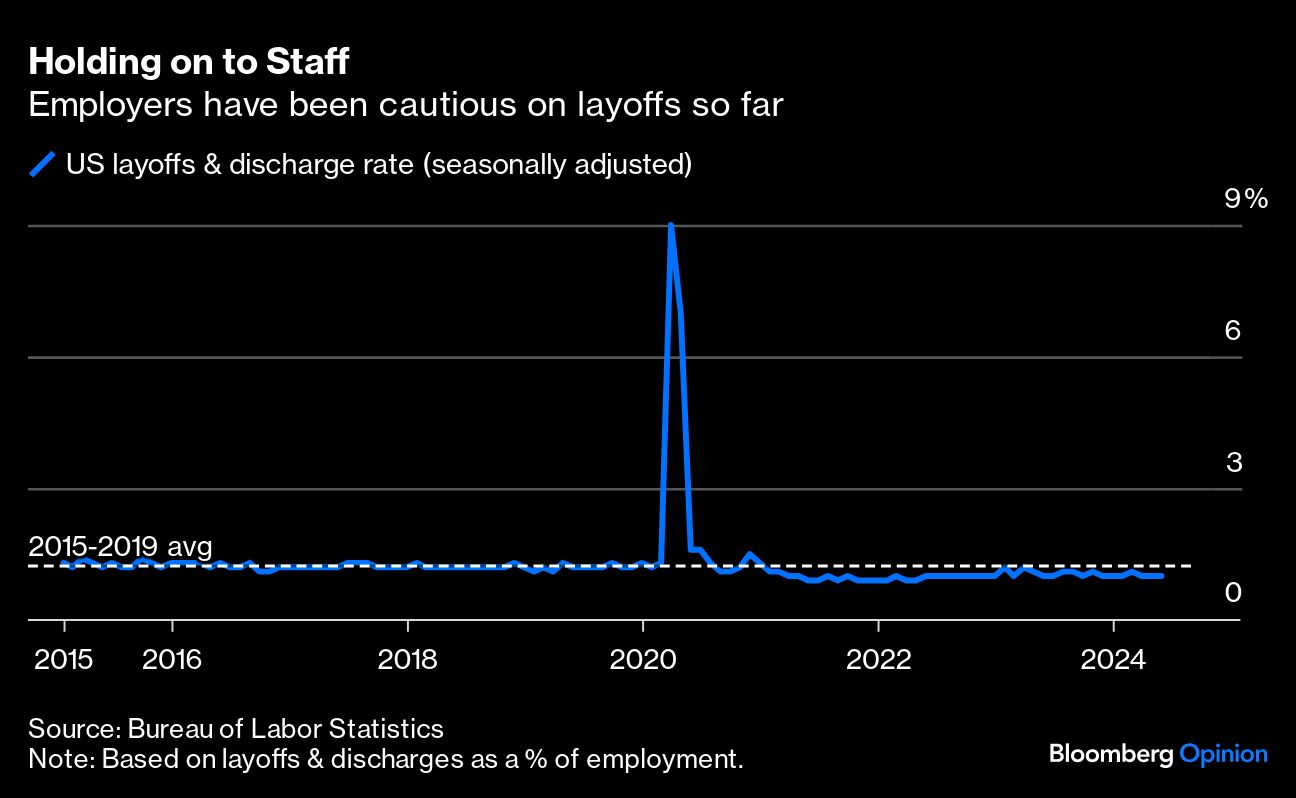

Policymakers have for months pointed to the resilience of employment data as evidence that there’s no urgency to lower rates. But the message from rate-sensitive parts of corporate America this earnings season has been clear: demand is sagging and the main thing keeping layoffs at bay is confidence that rate cuts will begin soon and usher in a brighter outlook for 2025. The Fed now needs to deliver not just one but a series of reductions to maintain business confidence and ensure there’s no further deterioration in the labor market.

About a third of the way through second-quarter earnings season, the proportion of companies beating revenue expectations is the lowest since 2019, according to Bloomberg Intelligence. The slowdown is particularly apparent in parts of the economy tied to household borrowing and consumer credit. Squeezed budgets have resulted in a miserable quarter for the automobile industry where rising inventories have put downward pressure on prices, crimping profit margins. Similarly, existing home sales in June were back near the lowest levels in a decade, bad news for companies that depend on housing turnover such as Maytag owner Whirlpool Corp., which said that the recovery they expected in 2024 isn’t going to happen.

The dynamics in these consumer-facing industries have contributed to a sustained rise in the unemployment rate, which last month reached its highest point in more than two years. In general, that’s the kind of environment that could quickly get out of hand, even if headline real gross domestic product numbers still look solid. In the fourth quarter of 2007, for instance, real GDP grew 2.5% right before the economy tipped into recession.

Commentary from many hard-hit companies, however, shows why we won’t repeat the downward spiral that the labor market experienced during the financial crisis — if the Fed acts quickly. Whirlpool said during its earnings call that it would stand to benefit once interest rate reductions ease pressure in the housing market. Brunswick Corp., the maker of recreational marine products, noted rate cuts beginning in September would provide a tailwind next year. (Yes, we’re now at the point where boat makers are tracking Fed expectations as closely as banks!) And Pool Corp., a distributor of swimming pool supplies, said that orders haven’t picked up yet, but increased inbound calls show customers are just waiting for confirmation on lower borrowing costs before making a decision.

Ultimately, companies make staffing plans based on their expectations for the future. We saw an extreme version of this in late 2020, when concert organizers and other businesses had to quickly anticipate what the approval of Covid-19 vaccines that November would mean for their 2021 plans.

For companies that believe they’ll benefit from Fed easing, a slower-than-expected 2024 is disappointing, but it would be foolish to cut staff now if rehiring will be difficult once a rebound in confidence arrives. Better to keep your current workforce and manage costs as well as you can until economic activity accelerates next year.

It would be a mistake for the Fed to take comfort in the relative stability of layoffs and delay the start of rate cuts — those layoffs haven’t happened because companies believe policy easing that will benefit them is around the corner. They are making plans based on those expectations just as the Fed is making policy based on what the economic data is doing.

Once the Fed cuts, and especially if it embarks on a halting cycle, the benefits will flow to the real economy with a lag that varies by industry. Mortgage refinance activity, for example, has been more sensitive to declines in home loan rates than mortgage purchase applications — refinance has climbed 40%, year over year, while purchase activity remains down. The equipment rental company Herc Holdings Inc. said last week that, once the Fed has signaled a cut, it takes about six months for shovel-ready projects to begin moving dirt, suggesting that a September reduction will benefit construction activity next spring.

Fortunately, the economy still appears to be in a position for the Fed to prevent the kinds of negative economic outcomes that policymakers want to avoid. But they shouldn’t mistake the seeming resilience of the economic data. Companies are increasingly counting on lower borrowing costs to hold the line on layoffs. The Fed needs to signal this week that it’s ready to come to the rescue.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Conor Sen