The assumptions that have driven this year’s global financial markets are being rapidly rethought.

In bond and currency markets, investors are racing to redeploy money amid mounting doubt over the outlook for the US economy, which has led to speculation that the Federal Reserve may need to cut interest rates faster or deeper than planned. Helping to drive the shift: A weakening American consumer, which is showing up in a rash of disappointing corporate earnings.

At the same time, stockholders have suddenly grown skeptical that technology companies’ massive investments in artificial intelligence will pay off any time soon. As a result, investors have been frantically dumping shares of big winners such as Nvidia Corp. and Broadcom Inc.

Copper and other industrial metals are also reversing a recent run-up, with China’s slowdown playing a role in their decline along with the worries over the US and tech.

“It does seem that an unwinding has begun of popular trades that brought valuations to stupid levels,” Louis-Vincent Gave, chief executive officer of Gavekal Research, wrote in a note to clients Thursday.

At Apollo Global Management, chief economist Torsten Slok told clients on Thursday that “if the economy starts slowing down, the speed of the slowdown becomes essential. A faster slowdown would have negative implications for earnings and increase the probability of a selloff in stock markets and credit markets.”

Here’s a look at some of the notable market moves and the underlying assumptions that have changed:

Government Bonds

In the bond market, this bleaker global growth outlook is bolstering wagers on rate cuts. Investors are snapping up short-dated securities amid concern monetary policy is proving too tight, acting before borrowing costs come down.

At one point on Thursday, the yield on the two-year US Treasury note traded just 12 basis points above the 10-year — the closest the market has come to ending an inversion in place since the middle of 2022, and a far cry from a spread of more than 50 basis points a month ago.

While the chances of rate cut by the Fed at next week’s meeting look very slim, the market is now pricing in deeper cuts later this year.

The repricing is also bolstering the yen, one of the biggest victims of tighter monetary policy in the US over the past two years. The Japanese currency has rallied around 6% from a low touched earlier this month, by far the biggest advance across the Group-of-10 peers.

Investors have liked to borrow in the low-yielding yen to fund investments in higher yielders such as Mexico’s peso or the Australian and New Zealand dollars, but now reckon change is underway with the gap between the Bank of Japan’s benchmark and its counterparts set to narrow.

Stock markets

US and European equity markets have been driven this year by a consensus that inflation was coming under control, allowing the Fed to ease monetary policy later in the year and thus avoid a recession.

By mid-May, the Stoxx Europe 600 Index was sitting at a record, giving investors a 12% return to date in 2024. The S&P 500 set a record as recently as July 16, with tech leading the charge.

Now many investors are taking the view that the Fed is falling behind the curve — not only is inflation quieting, but the economy is weakening too much. China is already easing monetary policy amid a slump in the world’s Number 2 economy.

Hence the predictions from some market watchers that the Fed could indeed act as soon as next week to lower borrowing costs or be forced to do more later if policymakers wait.

Almost a third of S&P 500 companies have reported second-quarter results so far, and the spotlight is increasingly on the sales figures, where the slowdown in economic growth is starting to become visible. Only 43% of companies have managed to beat revenue expectations, which would be the lowest reading in five years, according to data compiled by Bloomberg Intelligence.

And that AI frenzy no longer looks so positive. Investors were taken aback this week how much Google parent Alphabet Inc. is spending on the technology, with little to show for it yet in terms of revenue.

The Nasdaq 100 Index has sunk almost 8% from its July 10 record, wiping $2.3 trillion off the market value of companies in the benchmark. The index is still up 13% this year, and an investor survey by Bank of America Corp. this month showed that positioning in the so-called Magnificent Seven was the most crowded trade since exposure to growth stocks in October 2020.

“Valuations of mega-cap tech were increasingly impossible to justify with anything but the most heroic forecast for future growth, earnings and monetary policy,” said James Athey, portfolio manager at Marlborough Group. “It’s inevitable that these kinds of extremes cannot persist.”

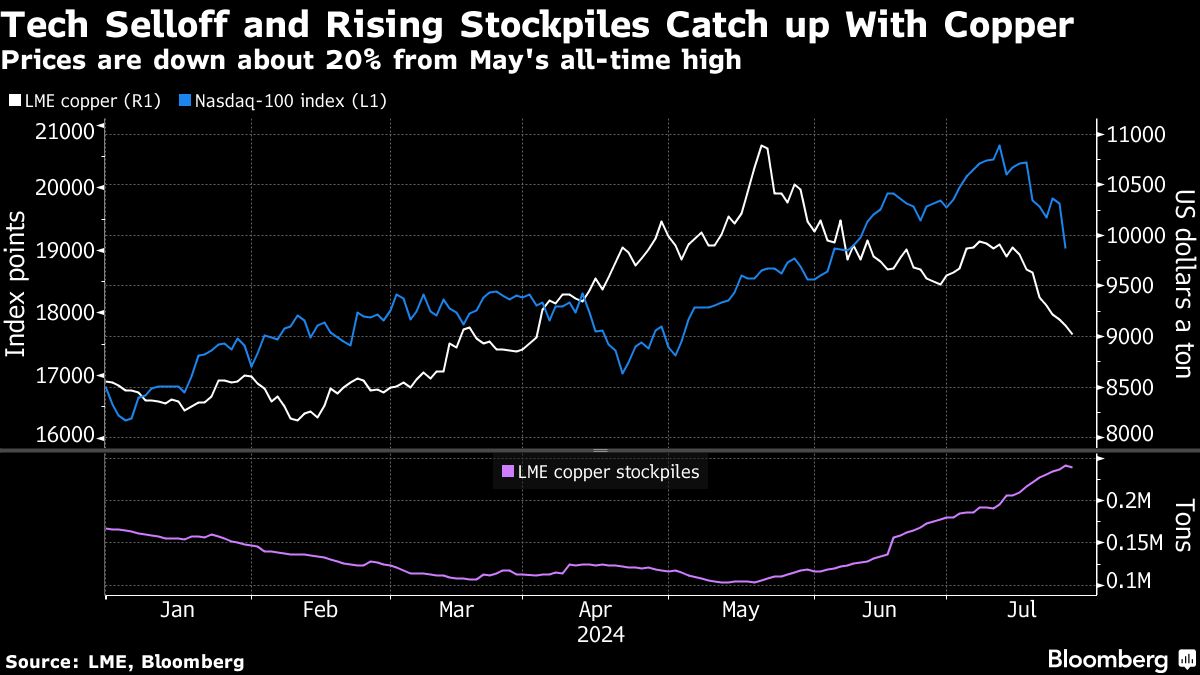

Metals

Mounting pessimism about demand and the tech industry is also infecting the metals market.

Copper fell below the $9,000-a-ton threshold for the first time since early April and is down by about a fifth since reaching a record in mid-May.

What’s changed there is investors who previously bought the metal on concerns of tightening supply and higher usage in data centers and other areas are shifting to fretting about rising inventories and weak conditions in the Chinese spot market.

Tin and Aluminum have also fallen.

What Bloomberg’s Strategists are Saying...

“In the perennial tussle between fear and greed, the former has seized the upper hand as a raft of consensus positions have suffered losses this week. It all represents a collective trip to the pain cave, one of those periodic episodes when positioning is just about the only fundamental that matters as investment risk gets reduced across the board.”

— Cameron Crise, macro strategist

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out ourpodcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.