The mortgage lock-in effect ended in the Levin household shortly before my in-laws arrived from Mexico to celebrate my daughter’s birthday at our home in the Miami area. As usual, my wife and I had no place to put them, and they had to get a room at a Courtyard Marriott. Chatting in the kitchen, we fantasized about a bigger house where the whole family could gather for birthdays and holidays. As inopportune as the interest rate backdrop seemed, we knew that it was time to make the move that we’d been considering off and on for years to the more spacious and affordable South Florida suburbs.

Elsewhere in America, hundreds of thousands of families are having similar conversations. The lock-in effect has stopped many of them from selling their homes and moving — even when they really wanted or needed to — because of a reluctance to give up ultra-low mortgage rates.

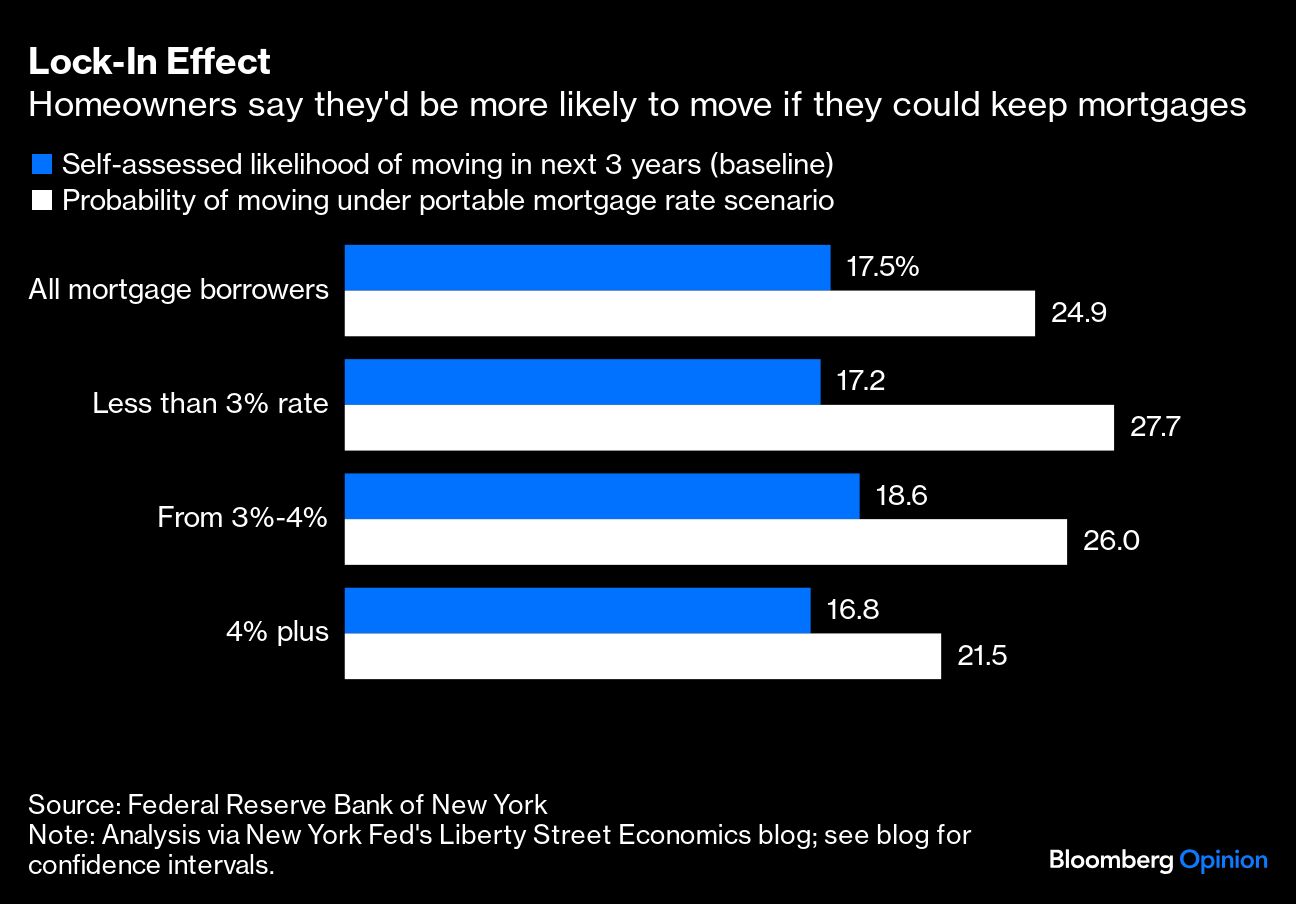

The inventory of existing homes for sale is still down by around a third from 2019, and many homeowners in a Federal Reserve Bank of New York survey suggest they’re staying put precisely because of interest rates. The average respondent in the 2023-2024 New York Fed study assessed their odds of moving in the next three years at just 17.5%, but they said the probability jumped to 24.9% in a hypothetical scenario in which they could take their existing mortgage rates with them. Among homeowners with sub-3% mortgages, the self-assessed odds of moving shot to 27.7% from 17.2% under the hypothetical scenario. I was in this group until recently, with my 2.625% pandemic-era mortgage.

The lock-in could only have happened under the extraordinarily unique circumstances of the past five years. We experienced a historic pandemic that led to near-zero interest-rate policies and once-in-a-lifetime refinancing opportunities. Then, we immediately transitioned into a high-inflation environment marked by 5.25 percentage points in Federal Reserve policy rate increases in the space of just 16 months. As a result, younger homeowners (I’m technically an “elder millennial”) delayed the purchase of their “move-up” homes and many empty nesters delayed the purchase of their “downsizing” homes because they didn’t want to blow their retirement nest eggs on extra interest payments. At first, many of us underestimated how long rates would stay elevated, and even fooled ourselves into thinking we could mitigate our need for wholesale change with light remodeling projects. In our case, we redid our kitchen, but it wasn’t enough.

Rates still haven’t dropped much, but my family got tired of waiting. In addition to our desire for more suitable guest quarters, my two daughters — who shared a room with bunk beds — were getting older and accumulating more clothes, and we wanted them to have spaces of their own. And, yes, sue me, we wanted a pool.

For some, this is how the lock-in was always going to end. Homes may be Americans’ biggest individual investments, but they’re also places that we live first and foremost. Real estate professionals often talk about the “Ds” that drive transaction activity: divorce, diamonds (marriage), diapers (growing families), downsizing (retirement) and death. Some people also throw other slightly more-financial “Ds” into the mix (like debt and default), but you get the point: In the medium to long run, the residential property market is mostly about people’s lives, not the vagaries of monetary policy. We seem to be getting back to that now.

What will the gradual sunsetting of the lock-in mean for the market?

That depends on your perspective. It’s clearly a net positive for new homebuyers stuck on the sidelines. It’s not going to make housing more affordable all of a sudden, but it at least means that listing variety should continue to improve, and that the typical buyer may have a bit more negotiating power. For the longest time, desirable listings were in such low supply that sellers wielded all the leverage in the deal-making process, even after mortgage rates shot above 7%. Sellers held extremely scarce assets. Going forward, that won’t be the case to the same degree.

As for existing homeowners like me, those of us that can make the numbers work, between locking in a good sale price and moving to cheaper suburbs, will probably find that the impact is mixed. If most sellers turn around and buy again, supply will rise roughly as much as demand. Yet as we all finally move onto higher mortgage rates, households that felt invincible against tight monetary policy will realize we’re mere balance-sheet mortals, and that may be a hard pill to swallow. In the short run, I thought it was worth the tradeoff for the guestroom and the pool. But ask me again how I feel about it in 2026 or 2027 (especially if interest rates stay high and I don’t get a chance to refinance). If there’s risk involved for a financially lucky guy like me, then there are certainly some perils ahead for the median household.

To be clear, it’s hard to know whether my experience is the “tip of the iceberg” or an exception to the rule — and the truth is probably somewhere in between. If you squint at the National Association of Realtors data for existing homes, you’ll see that May 2024 marked the highest month for inventory since August 2022, but just barely. We’re still a long way from normal. In the absence of a meaningful drop in interest rates, my best guess is that inventory will continue to rebound, albeit at an excruciatingly slow pace. But for me personally, I’m glad that the lock-in is over and we can finally move on with the rest of our lives and our new pool. I suspect that many other families will land on the same decision over the coming month and years.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin