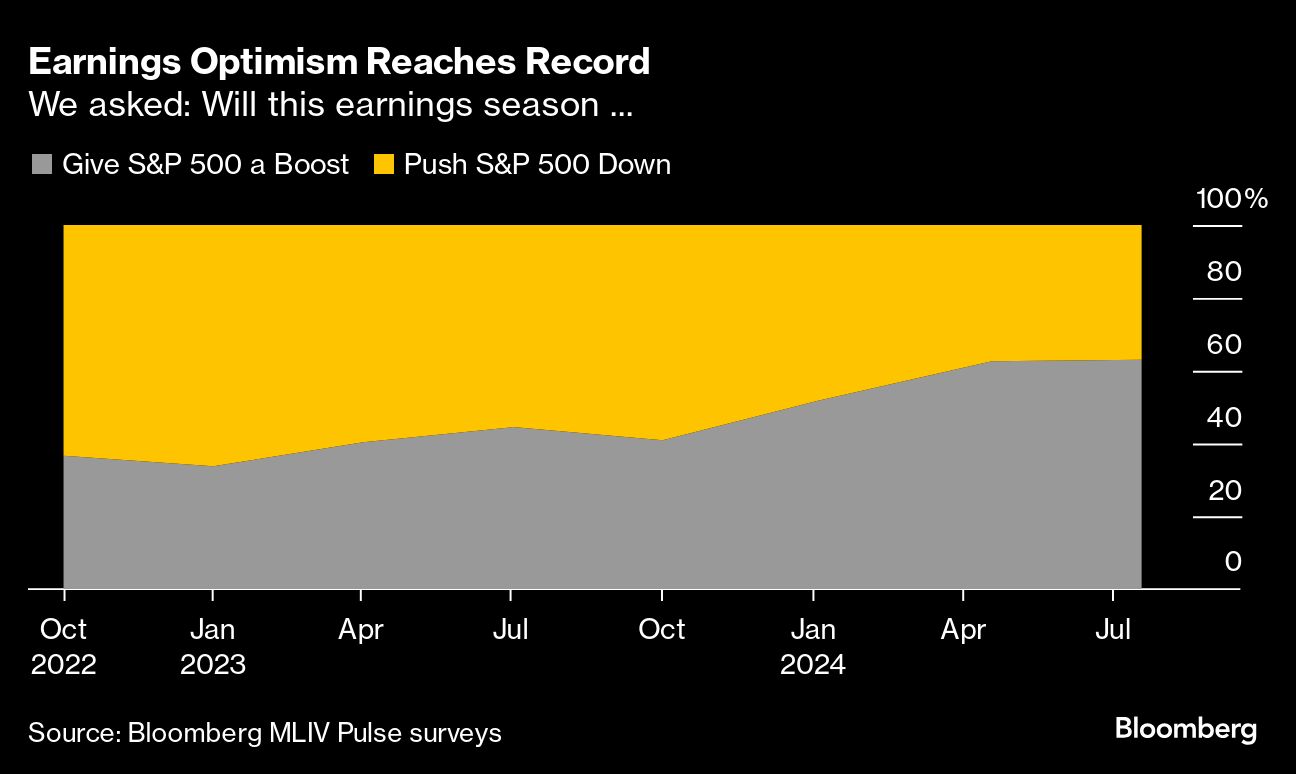

Despite the recent stock market slump that has some Wall Street pros bracing for a summer correction, respondents to Bloomberg’s Markets Live Pulse survey expect the latest round of corporate earnings to reinvigorate the S&P 500 Index.

As the reporting season ramps up, with results from headliners like Tesla Inc. and Google-parent Alphabet Inc. on deck in the coming days, nearly two-thirds of the 463 respondents to the questionnaire expect earnings to boost the US equities benchmark. About half of the participants predict that Corporate America’s scorecard will be better in the coming months than it was in the first half of the year.

At JPMorgan Chase & Co.’s trading desk, US Market Intelligence head Andrew Tyler expects positive earnings catalysts to lift the S&P 500 from its slough, particularly with analyst estimates for the so-called Magnificent Seven technology stocks — Nvidia Corp., Apple Inc., Amazon.com Inc., Meta Platforms Inc., Microsoft Corp., Tesla and Alphabet — signaling “another monster quarter,” he wrote in a note to clients. The cohort is expected to post earnings growth of roughly 30% for the second quarter from the year-ago period.

Upbeat results would be a much-needed driver for US equities, with the S&P 500 starting to go sideways after a roaring first half of the year. The stock market is facing pressure heading into a seasonally weaker period, with volatility likely to be heightened by uncertainty surrounding the US presidential election.

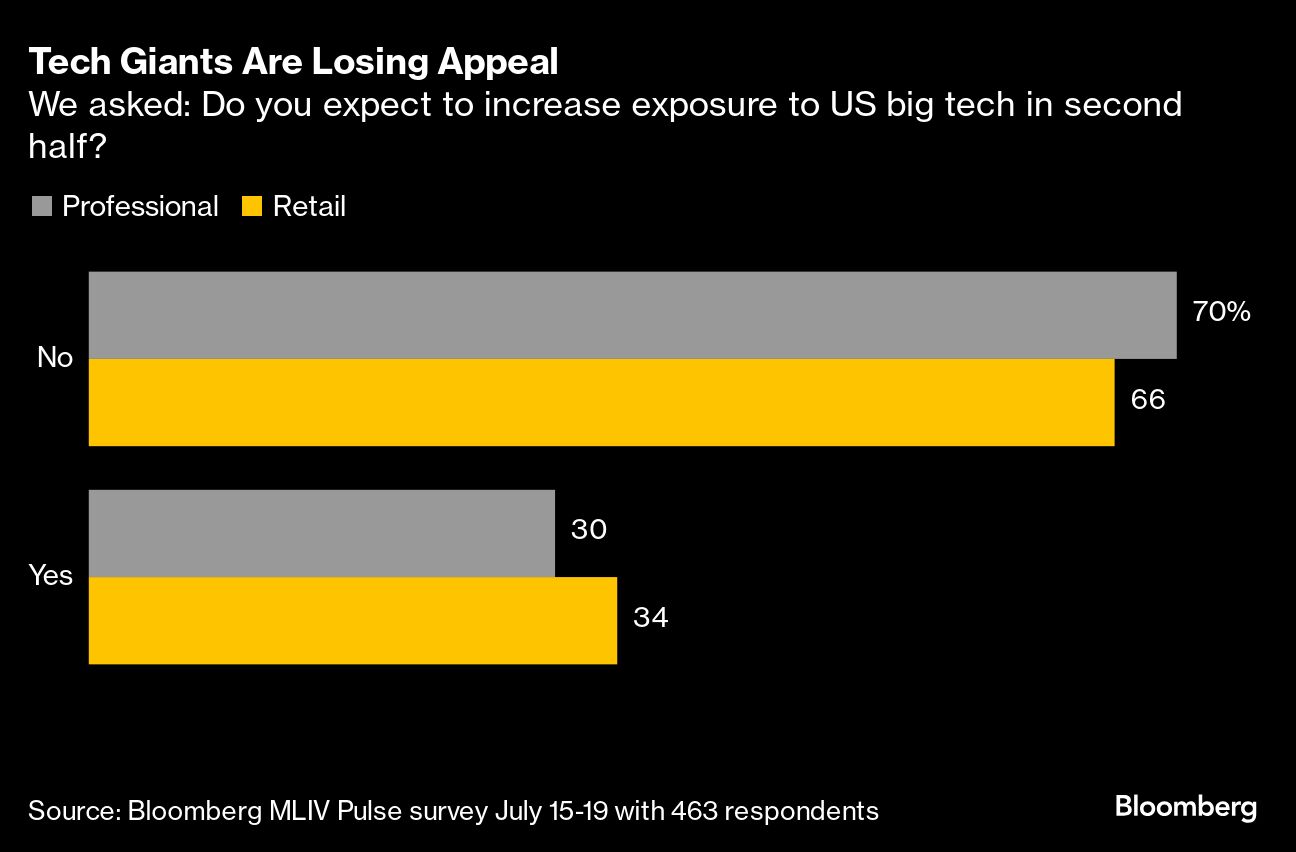

Stretched valuations, particularly among technology shares, have also worried investors. With that in mind, about 70% of survey respondents say they have no plans to increase their exposure to US big tech in the second half of the year.

The recent declines in American equities indexes have been more of a “change” than a “slump,” according to Michael Sansoterra, chief investment officer at Silvant Capital Management. In his view, companies in the artificial intelligence space are still spending, giving the generative AI story legs to keep powering tech stocks higher. Sansoterra has held Nvidia since 2019 in at least one of the firm’s funds.

“We expect earnings to actually go well,” Sansoterra said. “We expect the quarter to look more like the previous quarter, same types of companies beating for the same kinds of reasons.”

Stocks in the technology sector were pummeled last week as concerns over trade restrictions triggered a selloff in semiconductor shares and investors rotated out of large-capitalization equities into small caps. Goldman Sachs Group Inc. tactical strategist Scott Rubner deemed the moves the start of a summer correction, spurred by weak seasonality, stretched positioning and all the good news already being priced in.

Earnings can “help stabilize things, but I’m not sure it will be an epic catalyst,” said Kevin Gordon, senior investment strategist at Charles Schwab & Co. “The zone of earnings growth we’re moving into is historically consistent with more tepid gains for the S&P 500.”

“Nothing terrible, but it makes sense when you consider the fact that the strongest gains tend to happen as earnings are emerging from their recession,” he added. “That already happened, so now with the earnings cycle maturing, the market is already looking through that.”

The bar will be highest for tech, said Dave Mazza, chief executive officer at Roundhill Investments. He remains constructive on markets broadly, but says “unless we see results that are truly spectacular, I don’t think it will be enough to offset this correction in the very short term.”

While headlines about the US presidential election are intensifying as Vice President Kamala Harris is likely to take President Joe Biden’s place as the Democratic Party’s nominee, the lion’s share of survey participants said their equity positioning is not reliant on the outcome of the campaign.

The second half of election years have historically supported the S&P 500, according to Bloomberg Intelligence strategists Gina Martin Adams and Michael Casper. Since 1928, the benchmark stock index has gained an average 5.2% in the third quarter of election years, and returns were positive 62.5% of the time, according to their data.

The MLIV Pulse survey was conducted from July 15 to July 19 among Bloomberg News terminal and online readers worldwide who chose to engage with the survey, and included portfolio managers, economists and retail investors. This week, the survey asks whether a potential return of Donald Trump to the White House would strengthen or weaken the dollar.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of ourwebcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.