After languishing for three decades, Japan is on the cusp of a once-in-a-lifetime opportunity to revitalize its economy through tech innovation and entrepreneurship.

A tight labor market has emboldened young workers to ditch the stereotypical salaryman mold of lifelong employment at big firms and empowered them to take risks. The economic pain wrought by the so-called lost decades is easing and the nation’s soft power is attracting global talent. Investors spooked by uncertainty in China’s tech sector see stability in its neighbor, while geopolitical tensions are driving closer ties between the US and Japan.

Factors are ripe for lasting change. The government seems aware of this critical moment and has been attempting to invigorate economic growth by encouraging startups — although in its own bureaucratic way. But for Japan to succeed in creating the type of companies that can have global impact, policymakers need to be much bolder and the companies they support more ambitious. The country also needs to forge its own path to success instead of copying strategies that worked elsewhere.

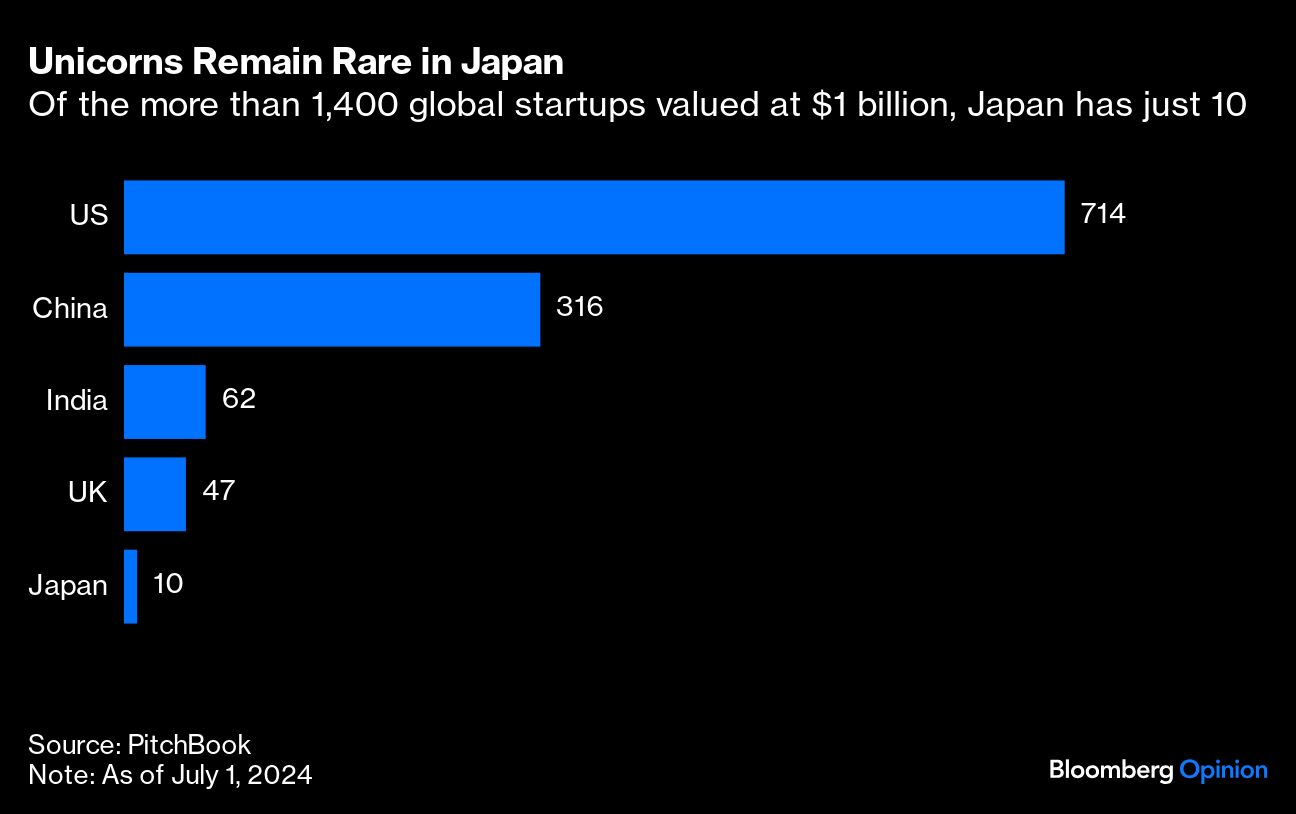

We’re now approaching the halfway point in Prime Minister Fumio Kishida’s five-year development plan that has the goal, in part, of creating 100,000 startups and increasing the number of unicorns by more than 10-fold to 100 by 2027. It’s not going well.

As of this month, Japan had just 10 unicorns, according to Pitchbook data, compared to 714 in the US, 316 in China and 62 in India. The country’s recent ambition comes amid a global pullback in unicorn-minting exuberance from investors.

Japan’s approach of trying to create tens of thousands of startups and hoping at least one will turn into a miracle company also doesn’t make sense for its market, which is a fraction of the size of the US or China. Separately, domestic conditions have historically led to tech startups going public at a much earlier stage than US companies might — often after just a couple of funding rounds, according to research published by Initial. After an IPO, companies face greater pressure to focus more on immediate profits for shareholders instead of ambitious tech projects or riskier growth efforts that can have greater impact.

The government could start by boosting its research and development funding toward small and medium-sized enterprises. Because most support for R&D comes in the form of tax credits, only profitable companies can tap into this. As a result, 92% of support for R&D goes to large companies, according to Richard Katz’s 2024 book The Contest for Japan’s Economic Future: Entrepreneurs vs Corporate Giants. Katz argues that Japan should allow startups to use tax credits once they become profitable. Kishida’s administration has also rolled out an angel tax break for individuals to invest in startups, but requires this go toward a single company, which carries far higher risk. Japan could instead follow France’s model that allows taxpayers to invest in angel funds, which tend to be more profitable and less risky, while unlocking far more funding for the startups.

Policymakers should also concentrate resources on ambitious ideas. In a blogpost last month, Takaaki Umada of the University of Tokyo warned “the beginning of the end” of Japan’s startup boom could already be afoot. Japan can keep creating new firms by imitating American playbooks and bringing them to its market. But this will most likely result in companies that are one-tenth the size of those in the US, even if they do end up being more profitable in the short run. Umada argues Japan needs to increase support for the kind of startups that can go global from day one and spawn entire industries.

This may seem riskier, even un-Japanese. But this way of thinking spurred some of the most legendary Japanese companies, like Sony Group Corp., that still drive its economy to this day. Once a 20-person company founded soon after World War II, Sony’s founders chose to create new technologies and “do what has never been done before” rather than imitate competitors, resulting in storied products like the Walkman and bleeding-edge innovation that was the envy of the world.

Protectionist industrial policies that benefit a single firm typically fail, but R&D subsidies can work when they are allocated by scientists and engineers free from political interference. And the most successful policies have been ones that promote competition. So stakeholders should focus resources on so-called “deep tech” initiatives that are developing new and revolutionary technologies that no one else can yet do.

Economists like to say that governments cannot pick winners, but losers can pick governments. The success of Sony owes more to the leadership of its founders than any state-backed policies. But now that Japan is trying to nurture startups, it should encourage competition and give pride of place to entrepreneurs rather than bureaucrats. After lagging Silicon Valley throughout the internet and software era, this will give its best chance to come back on top.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Catherine Thorbecke