The barbarians are back at the gates. Morgan Stanley and Goldman Sachs Group Inc. are confident that their most important clients are about to get active after a long spell on the sidelines and help goose the long-awaited revival in investment banking fees.

The private equity deal machine has been mostly jammed up for the past two years, leaving many investment bankers twiddling their thumbs while their bosses talked up green shoots that failed to flourish. There are plenty of potential road bumps ahead, but there’s reason to put more weight on the better outlook now even compared with just three months ago: The wave of debt refinancing that has led banks’ revenue recovery this year has also been helping to fix the prospects of many companies owned by private equity firms.

David Solomon, chief executive officer at Goldman Sachs, and Ted Pick, his counterpart at Morgan Stanley, both said this week that financial sponsors, another name for buyout funds, were under growing pressure to do more deals. Pick told investors on Tuesday’s second-quarter earnings call that private equity “needs to unglue” itself and sell companies so they can start investing again. “There is an enormous, multi-trillion-dollar stockpile between the two sides of [private equity] inventory that needs to be released and dry powder that's been raised,” he said. “I think you will see over the next number of quarters and really over the next number of years a resumption of more normalized M&A activity.”

The day before, Solomon told investors on Goldman Sachs’s earnings call that merger and acquisition volumes were about 20% below 10-year averages, largely as a result of private equity being gummed up. “You’re going to see over the next few quarters into 2025 kind of a reacceleration of that sponsor activity,” he said. “We’re seeing it in our dialogue with sponsors.”

Private equity has become hugely important to investment banking fortunes over the past 15 years as the industry sucked up assets and business into its highly leveraged ownership model while interest rates were pinned near zero. Sponsors came to account for up to 30% of investment banking revenue in many years.

Analysts might have rolled their eyes at hearing another round of upbeat outlooks from bankers after several quarters with no follow through. Pick acknowledged the disappointment at “delayed shoots,” but insisted that a nascent corporate finance recovery was visible, for example, in stronger convertible bond issuance, which typically precedes a pickup in initial public offerings and M&A.

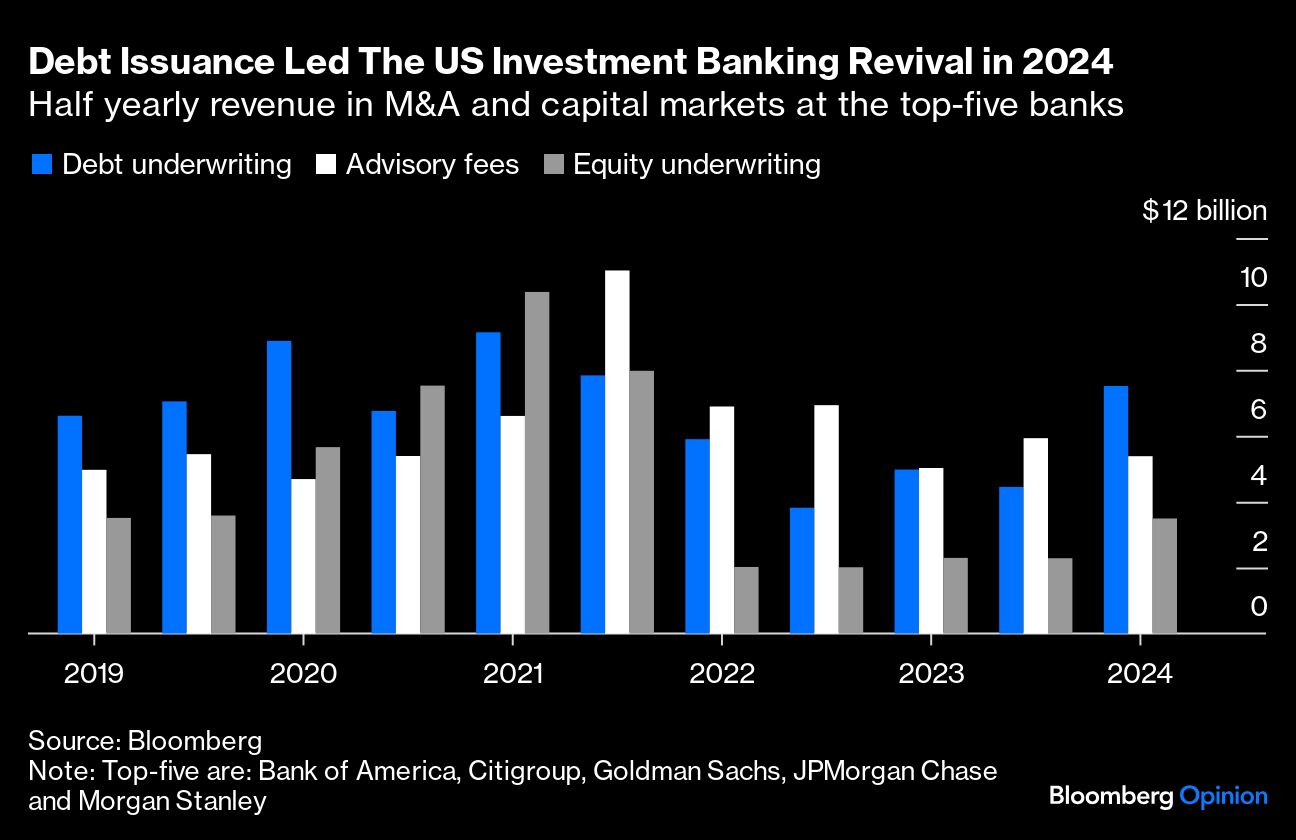

For private equity though, the more pertinent debt trend has been the huge wave of high-yield loan refinancing and repricing that drove the rebound in debt capital market fees this year. The five leading US investment banks each saw second-quarter DCM fees rise by between about 50% and 90% over the same period last year and all name checked leveraged finance as the main source. For all five combined, total first-half revenue hit its highest six-month total since 2021 and was ahead of pre-Covid levels and has far outstripped the weaker gains in advisory work and equity underwriting.

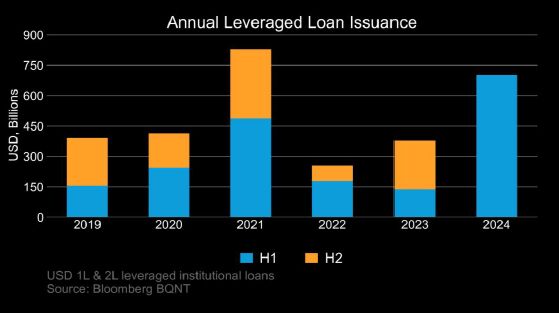

US leveraged-loan issuance this year of nearly $670 billion is already more than double the volume in all of 2023 and not far off the near-$800 billion full-year total for 2021, which was by far the busiest year of the past five, according to Bloomberg BQNT data. More than 90% of these loans, which mainly fund private equity buyouts, were made to refinance more expensive debt, some of which had come from private credit.

Interestingly, a major source of money behind these new, cheaper loans is banks themselves, which have been piling back into special investment vehicles known as collateralized loan obligations since the start of the year. US CLO issuance in the first half of 2024 has also hit the highest levels in at least five years, according to Bloomberg BQNT data.

The flood of cheaper loans will help improve the earnings outlooks for private equity-owned businesses and thus lift their valuations. This is great news for sponsors, who have held on to companies longer than normal in the past couple of years because they didn’t want to post losses on their portfolios caused by sharply higher interest rates and debt costs.

With interest rate cuts on the horizon, too, the gap between the value at which sponsors want to sell a company and what buyers are willing to pay should be closing. As it does, the pressure on private equity to return cash to their investors, or limited partners, will only grow. Last year saw the lowest ratio of cash returns to money invested for private equity investors since the middle of the Covid-19 pandemic or the great financial crisis of 2008.

Goldman, Morgan Stanley and their more diversified peers all need investment banking fees to pick up. The first half has been better than the last two years, but deal advice and underwriting share sales remain close to the weakest levels of the past five years. The US election could still throw a major spanner into the works, but the stubborn blockage in the private equity pipeline does look as if it’s beginning to clear.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies