Wall Street Economists See Compelling Case for Fed to Cut Now

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA growing number of Wall Street economists are cautioning the Federal Reserve is waiting too long to reverse course after raising interest rates to a two-decade high.

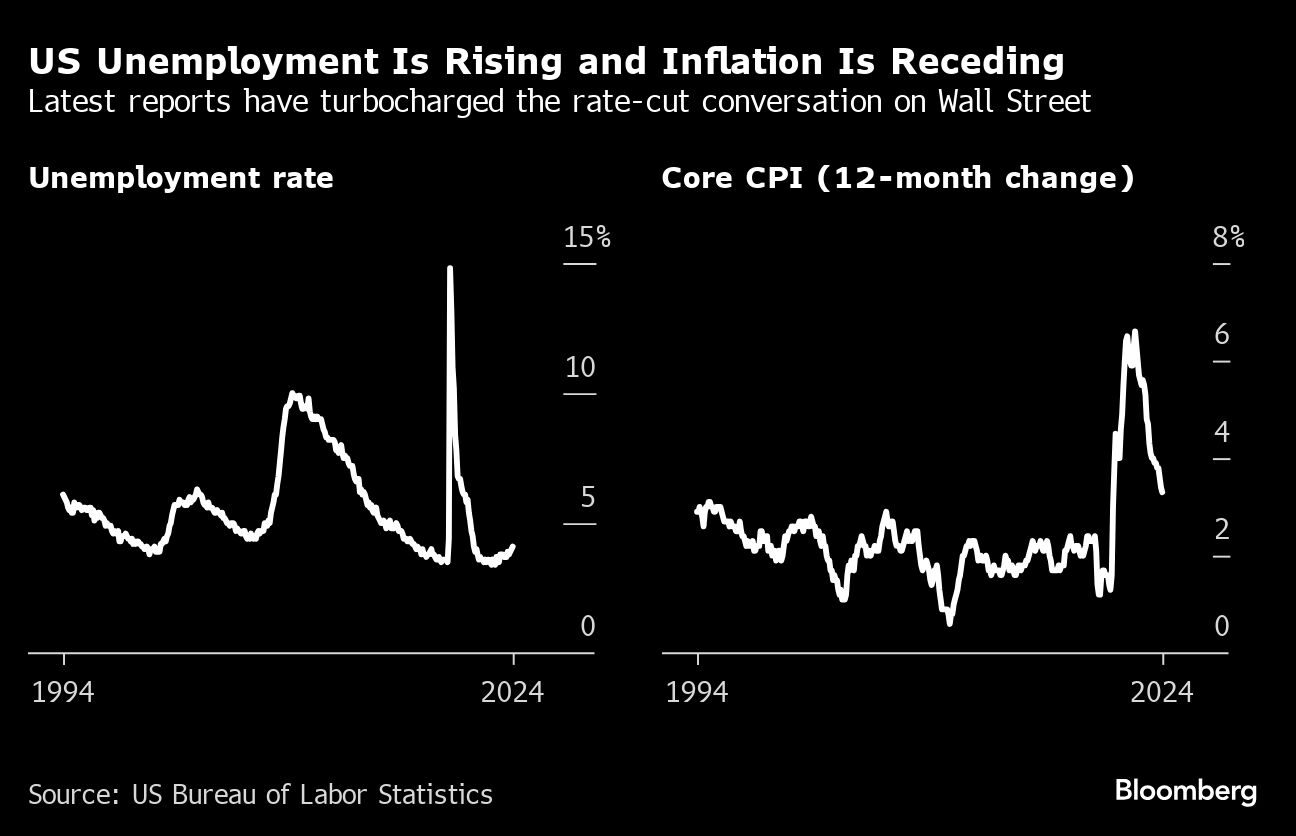

Tame inflation data in each of the last three months, combined with slowing US economic growth and a rising unemployment rate, are leading to calls for the central bank to cut rates at its upcoming policy meeting two weeks from now.

Such a move seems highly unlikely. Fed Chair Jerome Powell, at an event Monday in Washington, said he wasn’t going to give any guidance on timing for rate cuts, and most of his colleagues on the policy-setting Federal Open Market Committee still seem unconvinced of the need for urgency.

But the risks of waiting are growing, according to a number of prominent voices including Goldman Sachs Chief Economist Jan Hatzius, Queens’ College President Mohamed El-Erian and Renaissance Macro Research’s Neil Dutta.

“We see a solid rationale for cutting as early as the July 30-31 meeting,” Hatzius said in a report published Monday. “If the case for a cut is clear, why wait another seven weeks before delivering it?”

The FOMC is widely expected to hold its benchmark rate steady in July for an eighth straight meeting, marking a year since it first reached the current 5.25%-to-5.5% target range. Investors are betting on at least two cuts before the end of 2024, starting in September, according to futures.

Powell on Monday said recent inflation readings “do add somewhat to confidence” that it is heading down to the central bank’s 2% goal, and policymakers are now focused on both of the Fed’s mandates of full employment and price stability. But he also signaled a need for more evidence before getting started.

The case for easing now is based on the idea that adjustments to rates take time — perhaps a year or more — to have an impact on the economy, so policymakers need to be preemptive to avoid a downturn. Monetary policy guidelines like the widely-followed Taylor Rule would suggest the current rate should already be roughly 4%, or more than a point lower than it is now, Hatzius said.

Calls for a July rate cut have picked up steam over the last week and a half with the release of two key monthly reports on employment and inflation. While the unemployment rate remains relatively low at 4.1%, it has now edged higher in each of the last three months. It’s up from a low of 3.4% in early 2023, raising concerns about a recession risk.

Inflation, meanwhile, was muted in the second quarter after an unexpected pop in the first three months of 2024. The so-called core consumer price index — which excludes food and energy costs — rose just 0.1% in June, marking the smallest monthly advance since August 2021. Rental inflation in particular showed a long-awaited moderation, a trend that’s expected to continue from here.

“Waiting too long risks a higher peak in unemployment for little additional reward on the inflation front,” said Drew Matus, the chief market strategist at MetLife Investment Management.

Since the release of the latest inflation numbers on July 11, two policymakers — Chicago Fed President Austan Goolsbee and San Francisco’s Mary Daly — have highlighted that the Fed is near the confidence it needs to cut rates.

But others have been wary of moving too soon. When they last met in June, officials published projections showing four thought there should be no rate cuts this year, while seven expected one cut and eight saw two cuts.

“Cutting in July is just more of a lurch than the FOMC tends to make,” said Julia Coronado, the founder of MacroPolicy Perspectives LLC. Waiting one more meeting to move “is much more about committee management and getting a little bit more data under your belt.”

Instead, the FOMC in July could tweak its statement to highlight improved inflation data and Powell could use his speech at the Kansas City Fed’s conference in Jackson Hole, Wyoming, in late August to deliver a message signaling a September move.

The case for waiting is that inflation’s descent has been bumpy, as evidenced by the first-quarter readings. The hawks on the committee are worried that any resurgence could spark a rise in inflation expectations, making it more difficult to reach the 2% target.

“There have been multiple instances of people declaring victory on this battle prematurely,” said Wells Fargo & Co. Senior Economist Michael Pugliese. “There’s a strong case here to wait until the September meeting.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All