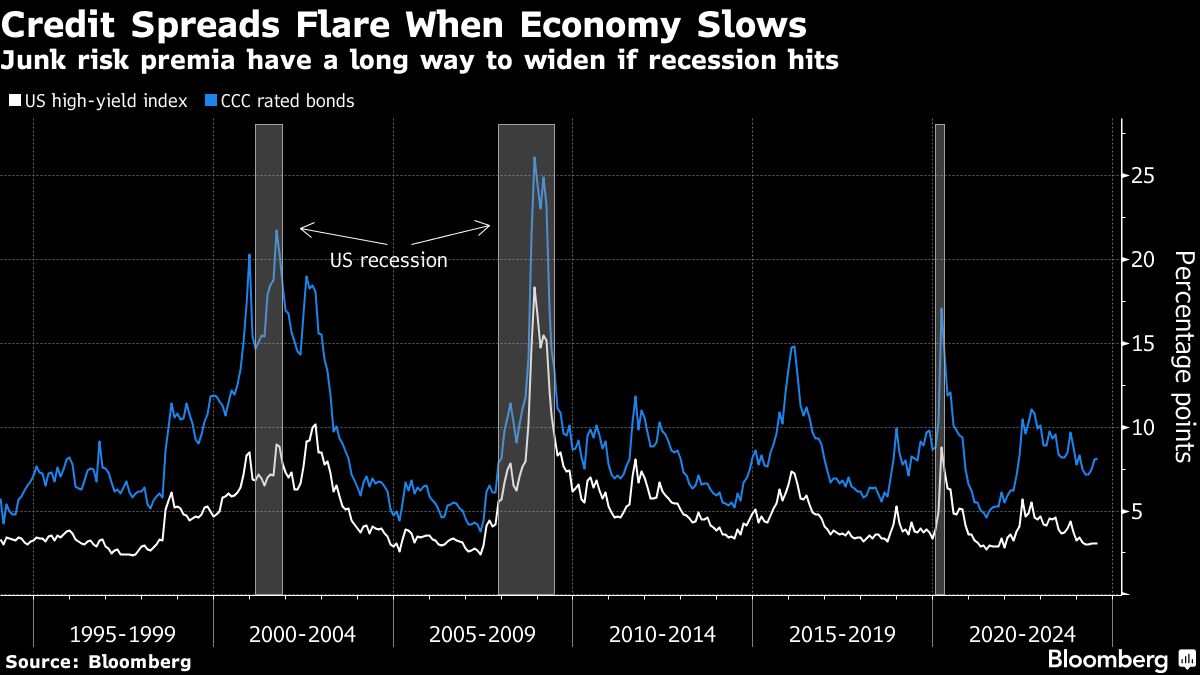

Credit markets are breathing a sigh of relief after inflation data showed price pressures are cooling broadly, but a weakening economy poses fresh risks to corporate debt.

A perceived gauge of risk in the high-yield credit market eased to the lowest since March following cooler-than-expected inflation in June. But the optimism may be masking risks that would materialize if the Federal Reserve doesn’t manage to pull off a soft landing and the economy cools too much, potentially pushing credit downgrade and default rates higher.

“For the first time in this post-Covid cycle we are seeing concurrent softness across a bunch of different variables,” Vishwas Patkar, a strategist at Morgan Stanley, said in a phone interview. “We don’t want to see the economy slow too much further from here. If growth is too weak, you start to worry about fundamentals, defaults and downgrades.”

For those bearish on the economy, there’s been a slew of signals that point to emerging weakness. Hiring and wage growth eased in June, the jobless rate rose to the highest since late 2021 and services activity contracted at the fastest pace in four years. The consensus among economic forecasters is that there’s a 30% chance of a recession in the next 12 months.

“Inflation is no longer the only risk we face,” said EY Chief Economist Gregory Daco. “Maintaining excessively restrictive monetary policy when the labor market appears to be fully back in balance could lead to an undesired weakening of employment growth and the economy.”

Credit investors are, so far, brushing off the risks, instead piling into a deluge of debt sales to capture some of the highest yields in a decade. Risk premiums in both the high-yield and investment-grade bond markets are tight as demand continues to outpace supply. Money managers are also moving up the risk curve, according to data compiled by LSEG Lipper, pulling money from blue chip funds and adding $675.5 million to junk ones.

Still, “correlations between equities and credit are breaking down because higher-for-longer interest rates has been a negative for a large number of equities but supportive of credit in general because of yield-seeking investors,” Priya Misra, a portfolio manager at JPMorgan Asset Management, said by phone.

Morgan Stanley remains constructive on credit and a more severe US downturn is not its base case, though it is a downside risk, Patkar said. Other investors are rotating out of the US after credit’s strong run this year. Amundi SA, for example, prefers Europe at the moment on valuations, according to a note from the asset manager on Friday.

For some investors, the recent string of US data offers a welcome refocus on the growth outlook.

“Major milestones for the Fed are all behind us,” said Jeff Klingelhofer, co-head of investments at Thornburg Investment Management following the most recent labor and inflation data. “We can finally move on from incessant chatter about the Fed and return our focus to what really matters: the underlying economy.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Olivia Raimonde