There’s a lot of bubble talk around US stocks.

The market has been on fire in recent years. The S&P 500 Index has more than doubled in value since bottoming in March 2020 on Covid fears. It’s also up 14% a year since 2010, including dividends, nearly 5 percentage points a year better than its long-term annual return.

No wonder investors are throwing around the B word.

But is this a bubble? It’s hard to say objectively because the word means different things to different people. One way to size up this market is to compare it to an undeniable bubble, namely the dot-com craze of the late 1990s, which remains by many measures the most expensive US stock market on record.

By that standard, the good news is that this market isn’t as frothy. The bad news is that it’s uncomfortably close, which is likely to be a drag on stock returns in the coming years.

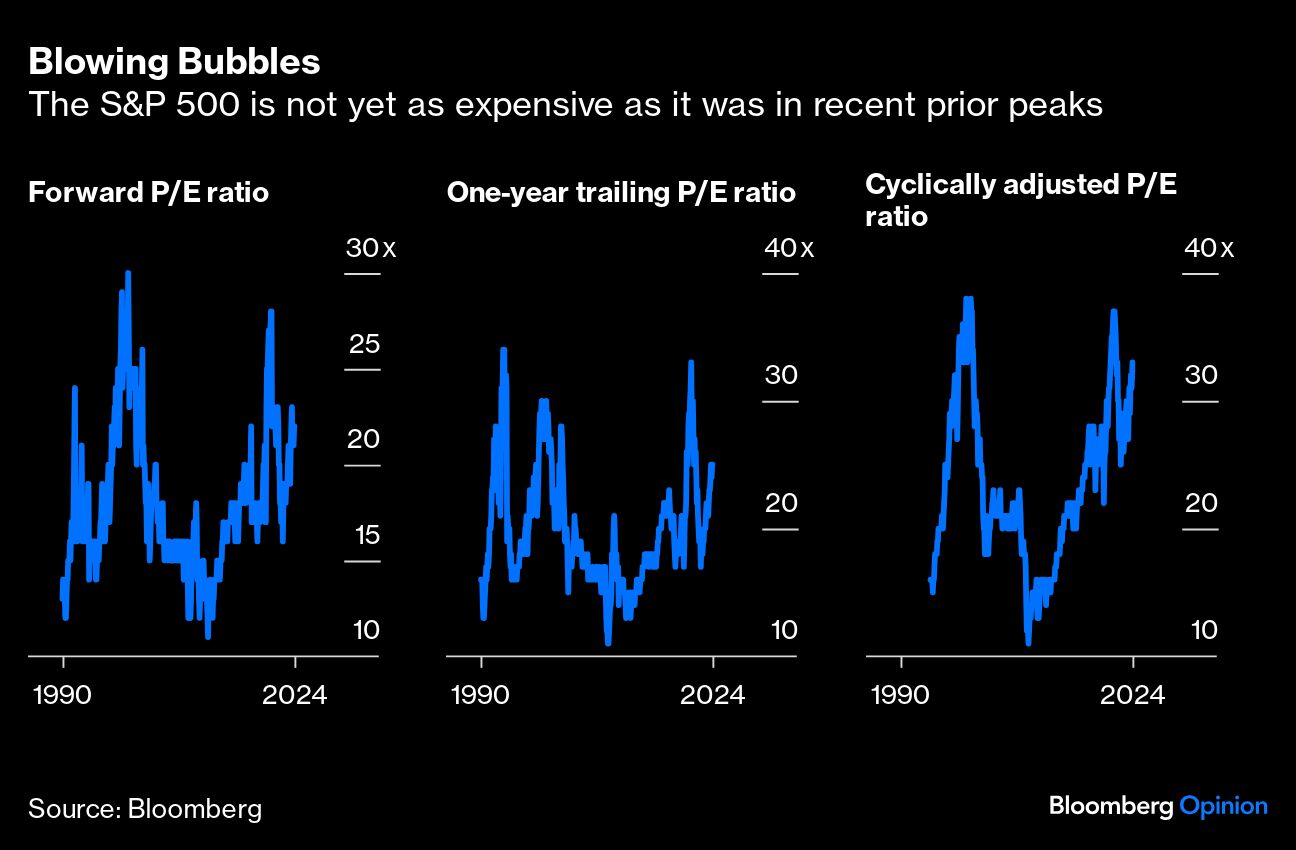

First, the good news. Whatever one’s preferred measure of earnings, this market is cheaper than it was at the dot-com peak. The S&P 500 trades at 22 times forward one-year earnings, compared with 30 times in December 1999. It trades at 25 times last year’s earnings, compared with 30 times in 1999. And based on so-called cyclically adjusted earnings, or the average inflation-adjusted earnings over the prior 10 years, it trades at 33 times, compared with 38 times near the dot-com peak.

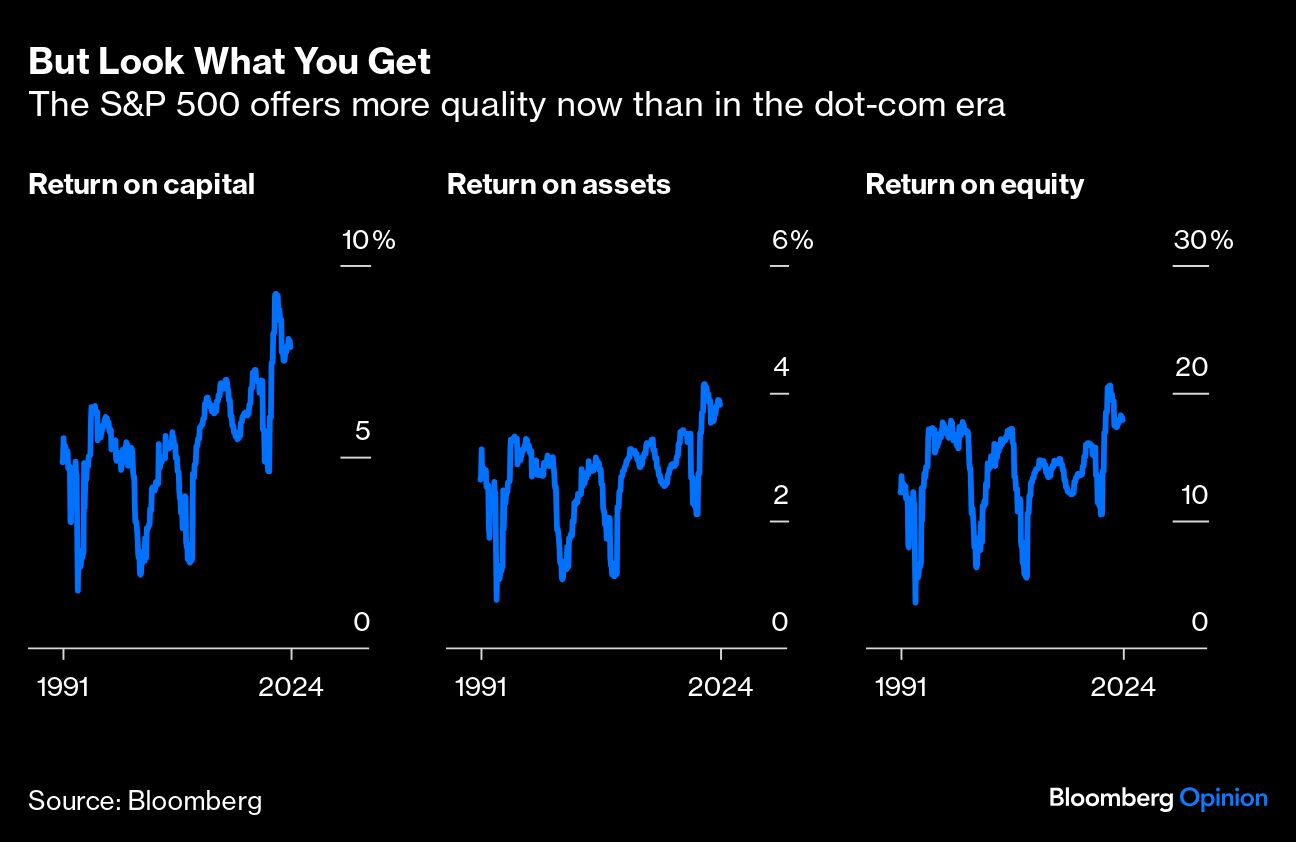

This market isn’t only cheaper; it’s also higher quality. As a group, the companies in the S&P 500 are more profitable than they were in 1999 — return on capital is 55% higher, return on assets is 34% higher and return on equity is 8% higher. Their balance sheets are also stronger because many companies lightened up on debt after the 2008 financial crisis. The S&P 500’s debt-to-equity ratio is nearly half what it was in 1999.

Investors seem less speculative, too. I ranked the companies in the S&P 500 from high to low based on price/earnings ratios using 12-month trailing operating earnings. The valuations of the bottom 450 stocks were comparable during both periods. However, every one of the 50 most expensive stocks was a lot pricier during the dot-com era. Yahoo! Inc. topped the list in 1999 with a ridiculous P/E ratio of 1,731. That honor now goes to Advanced Micro Devices Inc., which at 233 times earnings is still exorbitant but a fraction of that valuation. More broadly, the average P/E ratio for the 50 most expensive stocks in 1999 was 196; now it’s 83.

It helps that the 50 most expensive stocks today have a smaller footprint than they did in the dot-com era. They account for 17% of the S&P 500, compared with nearly a quarter of the index in 1999.

Those are all reasons to think that calling this market a bubble is probably premature. But it’s inarguably an expensive market, and it’s not too soon to think about what that means going forward. Historically, there’s a strong inverse relationship between valuations and subsequent medium-term returns — that is, high valuations tend to be followed by below-average returns, and vice versa. Notably, it took the S&P 500 more than seven years to reclaim its 1999 level, during which time the index paid investors just 1.8% a year.

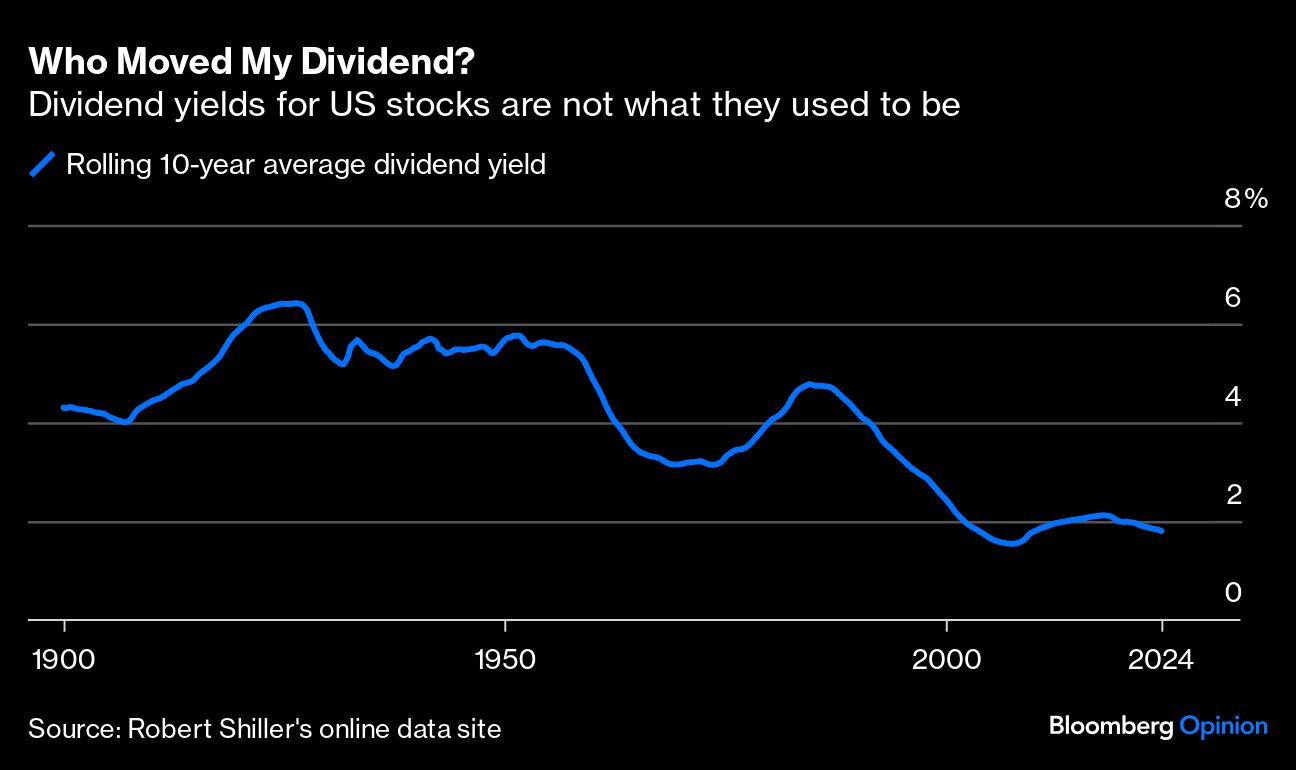

It’s hard to know exactly what lies ahead, but it’s possible to make an educated guess. From the mid-1800s to the mid-1990s, the two big drivers of stock returns were dividends and earnings growth. Since then, dividend yields have fallen off — the S&P 500’s dividend yield is barely more than 1%. So, investors must rely on earnings growth to power returns.

And what drives earnings higher are sales growth and expanding profit margins. Sales have grown by 4% a year over the past three decades; let’s assume that continues. The bigger question is about margins. Since the early 1990s, profit margins have swelled to 12% from closer to 4%, an enormous achievement that amounts to margin expansion of about 4% a year.

But there’s a limit to how much profit companies can squeeze from sales. It’s harder to imagine profit margins expanding meaningfully from here than it is to envision them contracting closer to their long-term average. Let’s be generous, though, and assume companies can maintain their current level of profitability for the next decade. With margins stable and sales growing at 4% a year, earnings will also grow at 4% a year. Add to that the current dividend yield of 1.4%, and the expected return for the S&P 500 is 5.4% a year over the next 10 years.

That also assumes valuations stay where they are, which may be too generous. The S&P 500’s P/E ratio has averaged 18 times forward earnings since 1990. If it returns to that average over the next 10 years, it would be a drag of 2.2% a year, bringing the S&P 500’s expected return closer to 3.2% a year. There’s no guarantee valuations won’t go lower, particularly if investors decide they prefer the 10-year Treasury yield at 4.3%.

One can quibble with those assumptions, but no matter how you slice it, it’s hard to recreate the mid-double digit returns the S&P 500 has produced since 2010. I’m confident the two biggest money managers on the planet, BlackRock Inc. and Vanguard Group Inc., tried their best, and here’s what they came up with: BlackRock estimates that US stocks will return 5.4% a year over the next decade, and Vanguard anticipates that number will be in the range of 3% to 5%. Sounds about right.

Don’t get me wrong, I like bubble banter as well as anyone, but it’s no substitute for a cleareyed assessment of what lies ahead.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Nir Kaissar