When the Hunt brothers cornered the silver market in 1980 by amassing a huge cache of the precious metal, jeweler Tiffany & Co. ran an advertisement in the New York Times denouncing the move: “We think it is unconscionable for anyone to hoard several billion, yes billion, dollars worth of silver and thus drive the price up.”

Might the copper market suffer a similar squeeze? Until now, I would have been confident in saying no. But speculators are about to get an easy and completely legal way to dominate the market for the red metal — a development that regulators seem far too relaxed about.

Sprott Inc., a Canadian investment firm, has launched a $100 million fund that will buy and hold physical copper on behalf of investors. Unlike most other speculative products that buy financial derivatives, such as futures contracts, the new vehicle will purchase actual metal, stored in a warehouse.

Copper doesn’t have the luster of silver or gold, but it’s crucial for the global economy, particularly as the electrification of everything makes copper more essential. A copper squeeze would be, therefore, detrimental for global economic growth and inflation. Consumers – think about wire companies that produce electrical cables, electric-car manufacturers and air-conditioner makers -- should be alarmed. A decade ago, when JPMorgan Chase & Co. and BlackRock Inc. proposed similar products, US copper users went to court to block them. Both firms ultimately abandoned their projects.

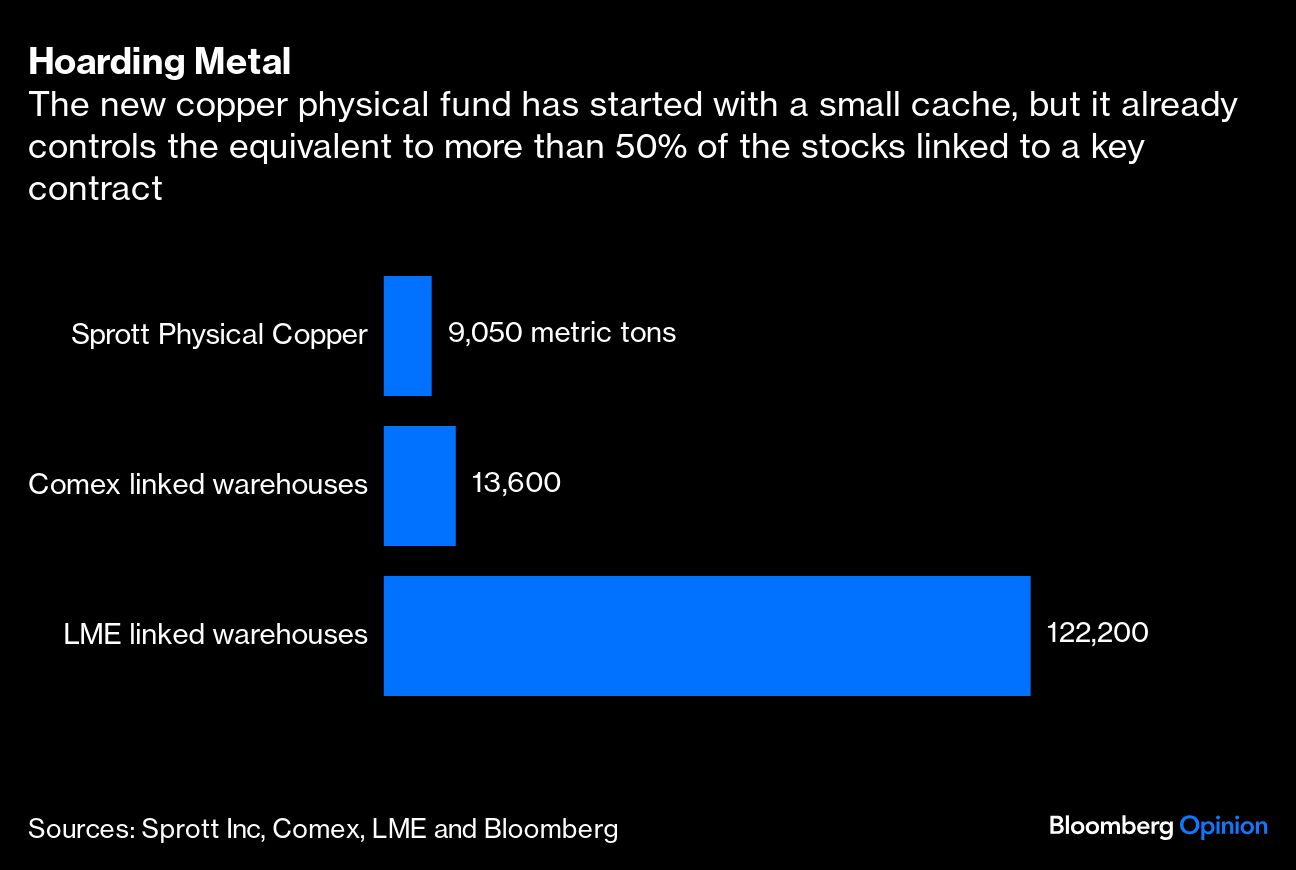

The new fund, listed on the Toronto Stock Exchange, has started with a small cache: fewer than 10,000 metric tons of copper, a fraction of the 28 million tons consumed annually. But its stockpile already equals more than 50% of the stocks in warehouses linked to the copper futures contract listed in New York, and about 10% of the stocks linked to the contract listed in London.1

The recipe for disaster is simple: As more money pours into the new fund, more copper will need to be stockpiled as backing. Others firms are likely to follow with their own physical funds, boosting demand even further. Rinse and repeat, and the copper market could suddenly face an acute — and artificial — shortage. Canadian regulators may have decided that the new copper fund wouldn’t impact today’s market prices. While that’s currently true, they’ve opened a dangerous door that will be difficult to close in the future if physical copper funds become sufficiently popular to squeeze the market.

Granted, the metal will be there, stored in warehouses and in theory accessible to whoever needs it. But if investors refuse to sell, it won’t be available to the global economy, which could lead to wild price swings. That regulators have opted to legalize this kind of squeeze doesn’t make it less dangerous. Investors looking to speculate in copper had plenty of other instruments available, including swaps, futures and options.

I’m all for encouraging speculation in commodity markets: Hot money plays a key role in helping to guide the invisible hand, providing price discovery and liquidity. But the Sprott Physical Copper fund isn’t a speculative investment vehicle — it’s a hoarding one. The fund manager is in the buy-and-hold commodity business, and makes no secret that its model relies on stockpiling. Its strategy is to never sell the copper it accumulates, baring very unusual circumstances, although it would be open to loaning the metal.

If Sprott succeeds to the point where it attracts, say, a couple of billion dollars in assets, the fund would need, at current prices, about 200,000 tons — surpassing the amount of copper available in the warehouses linked to the copper contracts in London and New York.

The argument in favor of physical funds in precious metals is that investors want to own the actual asset because they are worried, among other things, about confiscation and debasement. Thus, physical gold funds are a hedge against, in many ways, Armageddon. But no one buys copper to defend against the end of days.

The Sprott fund isn’t just a bad way to bet on copper; it’s also very expensive. Hopefully, that’s the best insulation against its potential impact: Its fees are so high, more akin to a hedge fund than a mutual fund, that it probably won’t prove too popular. For starters, subscribers paid the equivalent of 6% of the net asset value of the fund in fees to the underwriters of the initial public offering. Then, the annual running fee equals 0.5% of NAV, plus another 0.9% in warehouse and insurance costs and a further 1% in one-off fees to a trading house for buying the copper.

So, even putting aside the cost of the IPO, investors are paying nearly 2.5% of their capital in fees in the first year. Moreover, the trading house buying and storing the copper gets an “incentive fee” of 50% of all the profits it makes “on all other transactions involving copper, which are not outright purchases or sales of copper, such as lending and exchange transactions.” So the incentive to pledge the warehoused metal in various side bets is extremely high.

With such generous fees and the risk of a market squeeze, the only winner is the company behind the fund. For investors and the global economy, it’s a worrying development that should have been nixed — like it was a decade ago.

1. Commodity traders and others control copper stocks outside the exchanges, so the total amount of copper inventories is higher than the Comex and LME linked warehouses suggest.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Javier Blas