A broad equity rally isn’t spilling over into the technology sector, where gains are still concentrated in just a few artificial intelligence winners that have become defensive plays amid an uncertain macroeconomic backdrop.

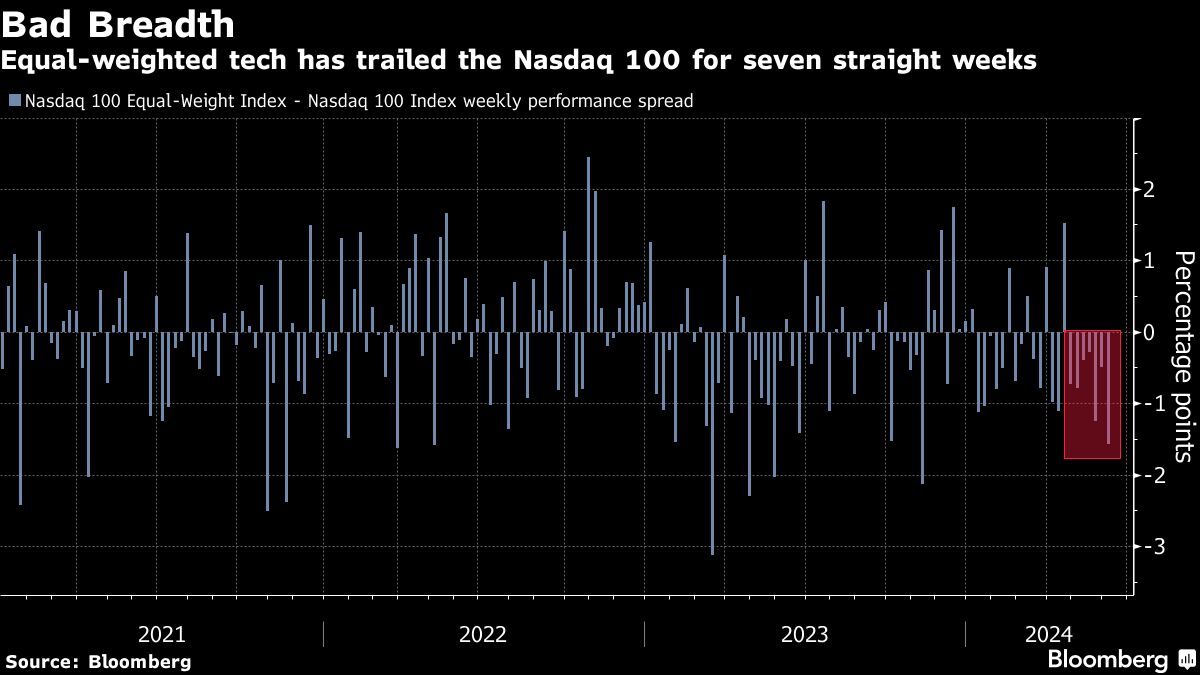

An equal-weight version of the Nasdaq 100 Index, which makes no distinction between software giant Microsoft Corp. and drugmaker Moderna Inc., has trailed its cap-weighted peer for seven consecutive weeks through Friday’s close, the longest streak of underperformance since the first week of February 2020, data compiled by Bloomberg show. Before that, a lag this consistent happened only a handful of times ever — in 2017, 2012 and 2007.

For the “equal weight, in general, to do better, we need to get a sense that the Fed is gonna cut rates,” Alec Young, chief investment strategist at Mapsignals, said.

Friday’s blowout jobs report threw cold water on hopes that the Federal Reserve will hand out multiple rate cuts this year. Following the print, Fed swaps no longer price in a cut before December. The S&P 500 Index and Nasdaq 100 initially dropped, but pared losses to end the week higher 1.3% and 2.5%, respectively.

“There’s a lot of macro uncertainty right now. So it’s all about bottom-up earnings visibility. And the reality is that the mega cap, Magnificent Six really provide that,” said Young, referring to the so-called Magnificent Seven excluding Tesla Inc.

Investors are most comfortable sticking to what’s worked — piling into the biggest technology stocks and the winners of the artificial intelligence wave for their relative safety. Chip stocks, and especially Nvidia Corp., are seeing the most momentum as investors including hedge funds eschew other tech stocks, including software companies, that could be left behind in the AI frenzy.

“It’s very difficult to get broad market participation, value participation, equal weight participation when you have cyclical concerns,” said Young.

To be sure, the weighted Nasdaq 100 usually outperforms its equal-weight counterpart because of the larger impact of the biggest winners. Still, the concentration in a few names means that if there’s a selloff in the top, it could drag down the entire index and market — something there’s less risk of in the equal-weight index.

“I think in the three to six-month time horizon we may see something of a bubble left that pops,” said George Ball, chairman of Sanders Morris Harris, adding that sky-high valuations are at the top of the list of potential worries. “Because those few names so dominate the tech sector, weakness in them will bring down the broader averages, perhaps even quite sharply.”

Still, it’s impossible for investors to ignore the biggest tech stocks as they grind higher.

“Money’s going to flow to leadership stocks,” said Ken Mahoney, chief executive officer at Mahoney Asset Management, even if those stocks make up a disproportionate amount of weightings in indexes. “If that’s what it takes to find and deliver performance, you’ll find us there too.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Carmen Reinicke